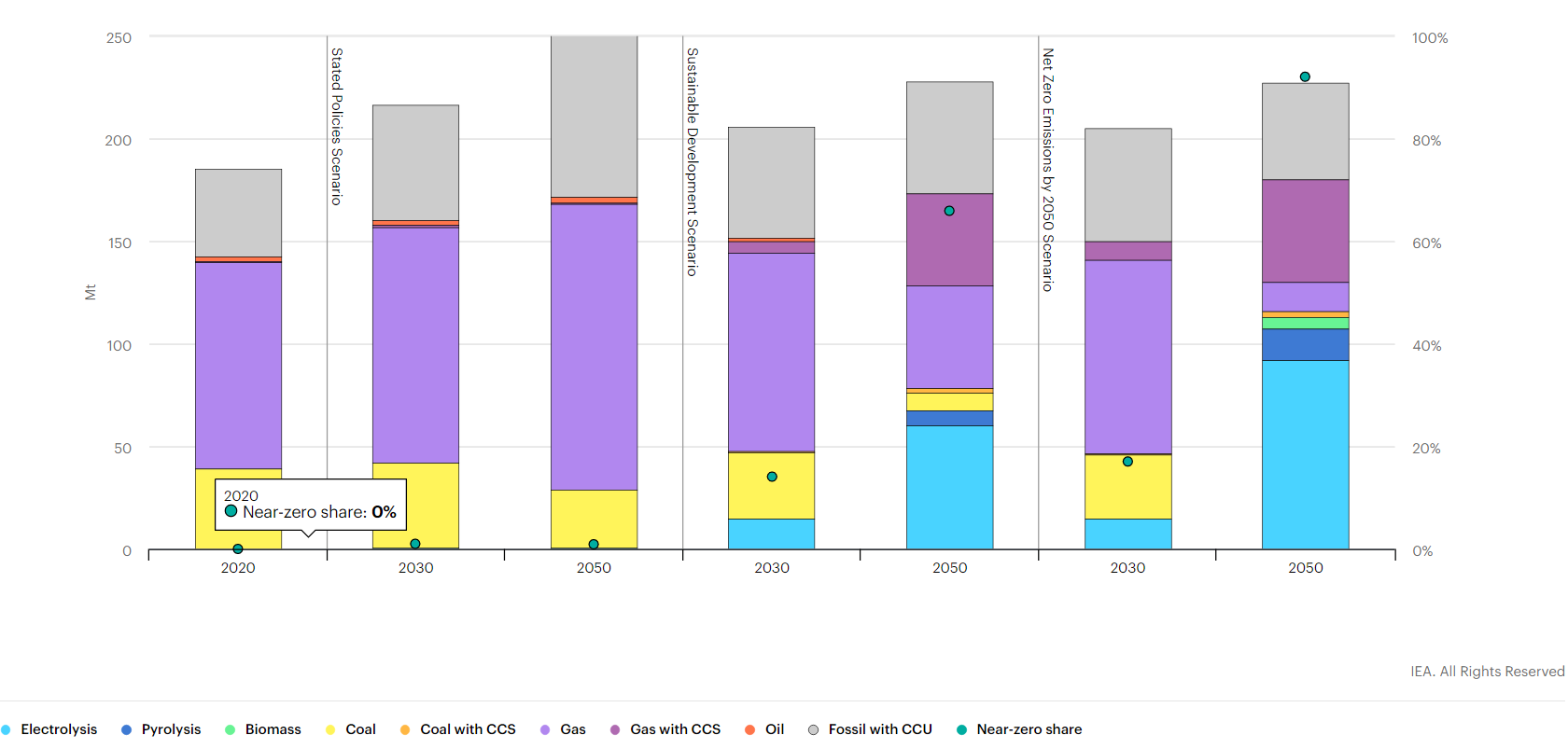

One question we would have concerning the IEA ammonia projections in the charts below is whether the absolute demand assumption for 2050 is too low. If Japan has success co-firing its coal-based facilities with ammonia over the next 6-7 years, we could see a step-change in ammonia demand. The chart likely reflects expectations in Japan, but we would expect other coal-heavy economies to follow Japan's lead. If this were the case, we would expect the share of hydrocarbon-based ammonia to rise with accompanying CCS.

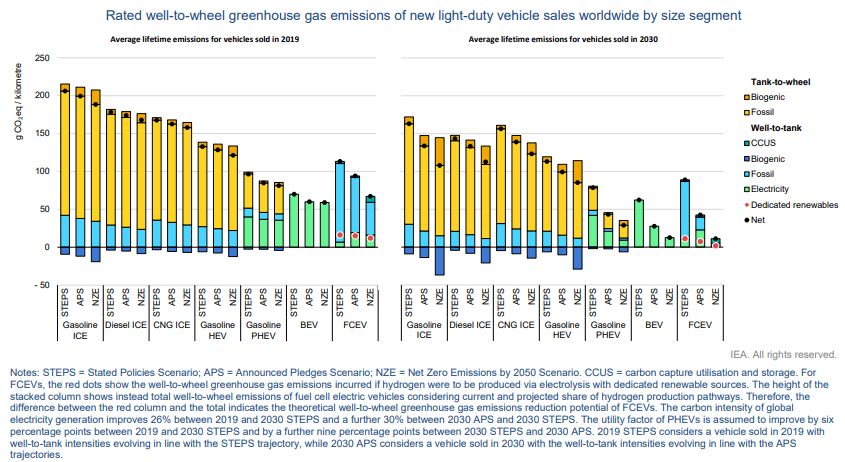

We highlight more from the IEA on the importance of EVs versus other vehicles to bring down “well to wheel” carbon footprints and the second (not unexpected) “kick in the pants” chart that shows the World woefully short in terms of its projected EV adoption rate. There are – probably expensive – hurdles to reaching the IEA net-zero goals with respect to EVs. The first is going to be the need to pay or tax consumers enough for them to give up a perfectly good ICE vehicle long before the end of its natural life.

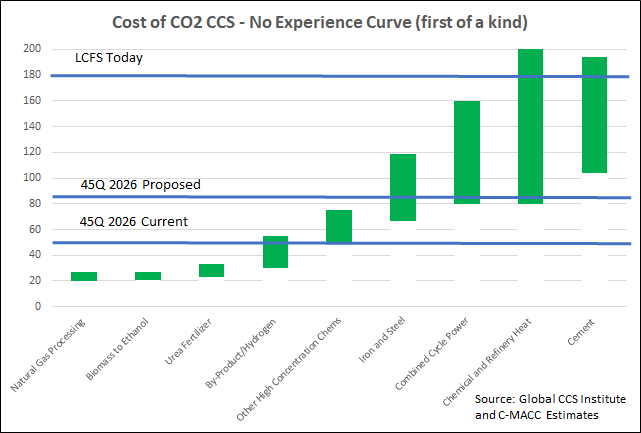

We want to focus today on the headlines around the possible increase in the 45Q CCS credit in the US and discuss the false logic of those that are objecting to it. There is no scenario where the US can move to a lower emissions power and transport profile while avoiding runaway inflation and social disorder without the continued use of fossil fuel-based power and transportation fuels for decades. The reliance on these fuels should and will decline over the years, but it is unreasonable to expect a transition that causes it to stop overnight. In the meantime, CCS is a mechanism that would allow fossil fuels to play a part with a much lower emissions footprint, and given that the CO2 impact on global warming is cumulative, if we can capture and store several billion tons of CO2 underground over that transition period it should be a good thing. Members of the Sierra Club and others would do well to look at the energy inflation problems in Europe and the move this week to put natural gas and nuclear back in the energy transition mix (too late in our view) because the move to renewables cannot keep pace with demand, which will grow faster as more EVs hit the road. The proposed 45Q credit is shown in the chart below vs. the current credit, the LCFS credit, and estimates of CCS costs.

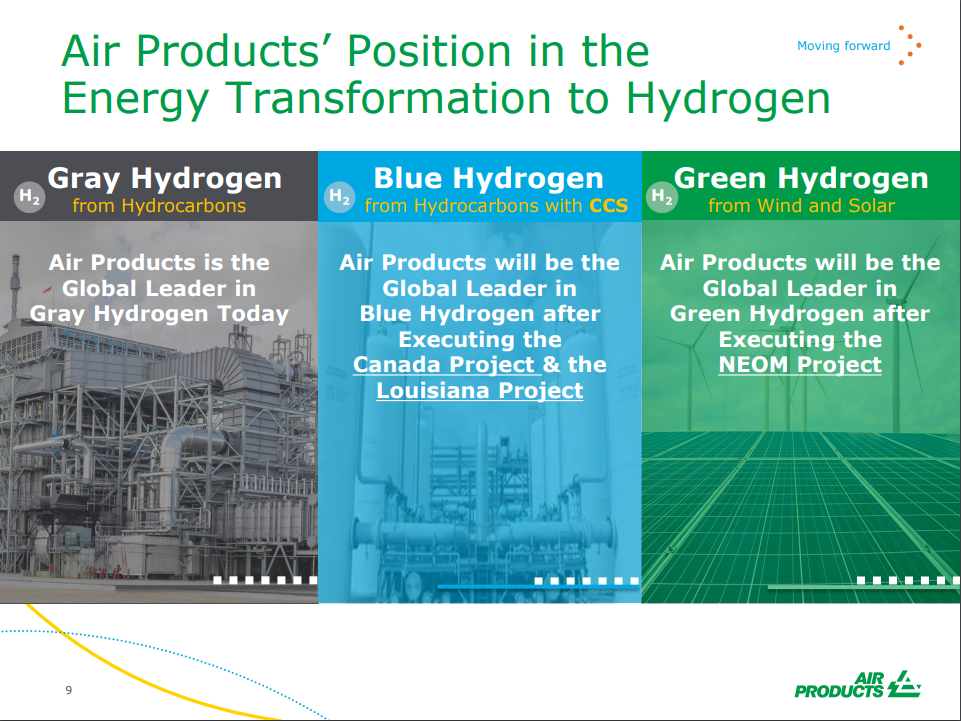

It is interesting to contrast Linde and LyondellBasell with Air Products and Dow. Air Products and Dow have transitioned away from the more generic messaging around broad objectives, and while they still have them, have started talking about concrete plans and spending aimed at lowering carbon emissions. Dow has a project on the books that will lower the emissions of existing capacity while Air Products is talking about greenfield low carbon investments at this point. Many of the commentators and climate activists are calling for concrete plans as opposed to broad objectives and we suspect that most of the narrative will move that way across energy and materials.

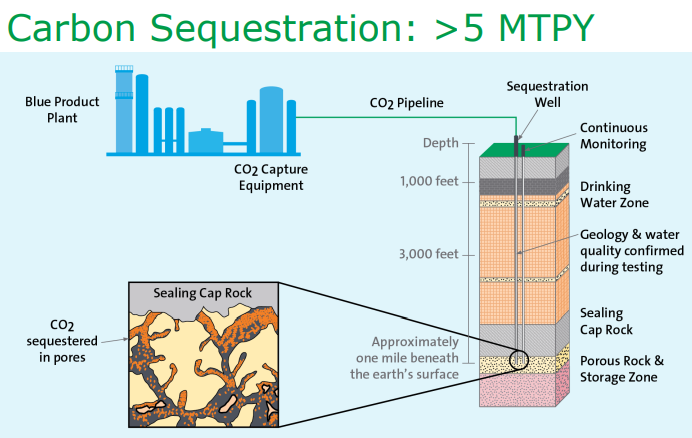

We want to focus on carbon use today, in part because we have written extensively on sequestration recently, in part because of the headline highlighted below, and in part, because we need something fresh for our ESG and Climate report tomorrow! Carbon use does not get much press beyond EOR, but there are emerging technologies and there is a lot of R&D spending – on how to collect CO2 more efficiently and on what it might then be used for. We suspect that almost everything being looked at will have some application, but that there will be limits to those applications and they will likely be niches in nature, but not necessarily unprofitable.

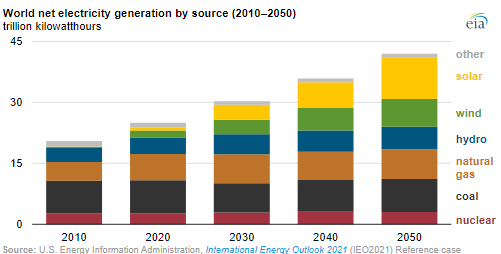

If you look back at our ESG and Climate piece this week (EIA View Suggests Natural Gas & CCS Critical To Net-Zero Goals), you will note that we focused on the recent EIA global energy outlook, and another chart from this outlook is shown below. In the ESG report, we talked about the global need to support increased “clean” natural gas use to offset as much of the coal predictions in the chart as possible and to drive additional hydrogen production to offset some of the petroleum product demand that the EIA still expects to be sued as a transport fuel in 2050. We also called for the broad and warm embrace of CCS so that some of the fossil fuel that the EIA is predicting – especially all of the fuel used for power in the exhibit below. Yesterday Air Products announced not only a large blue hydrogen complex for Louisiana but also the CCS to support it and made a very compelling argument in its presentation for the need for substantial volumes of blue hydrogen – something we fully agree with. We covered the subject in detail in yesterday’s daily. “Blue Is The Color, Hydrogen Is The Game…”

In our ESG piece yesterday we talked about the competitive edge that Canada now has with respect to both natural gas (because of lower prices versus the US) and CCS, both because of relatively low costs but also because of the clear value on carbon. Yet today we see an announcement in the US!

The IEA chart in the exhibit below is another stark reminder of how far away stated policies for clean energy are from what will be needed, and the 2030 gap is the most significant in our view as there is little time to correct it. The IEA has presented several studies over the last year that presents a series of “straw men” examples around how the World and, most recently China, might meet their respective net-zero targets, and the chart below is intended to show how far adrift we are, comparing what is needed to what has been stated. As we have mentioned a couple of times, it would be unusual for companies and countries to have firm plans for 2050 that sum to what the IEA is looking for as there are new technologies under development and the incentive/penalty landscape is still uncoordinated and very unclear. The latter is also a problem looking forward to 2030, but closing the gap between the STEPs scenario and the NZE scenario by 2030 looks almost insurmountable today, without a much tougher and more globally coordinated regulatory landscape, which looks unlikely given some of the low expectations for COP26 specifically. Note that how under the Net-Zero scenario discussed by the IEA, fossil fuel would peak by 2025 and compare this with the EIA analysis that we discuss in today's daily report – there is a huge disconnect.

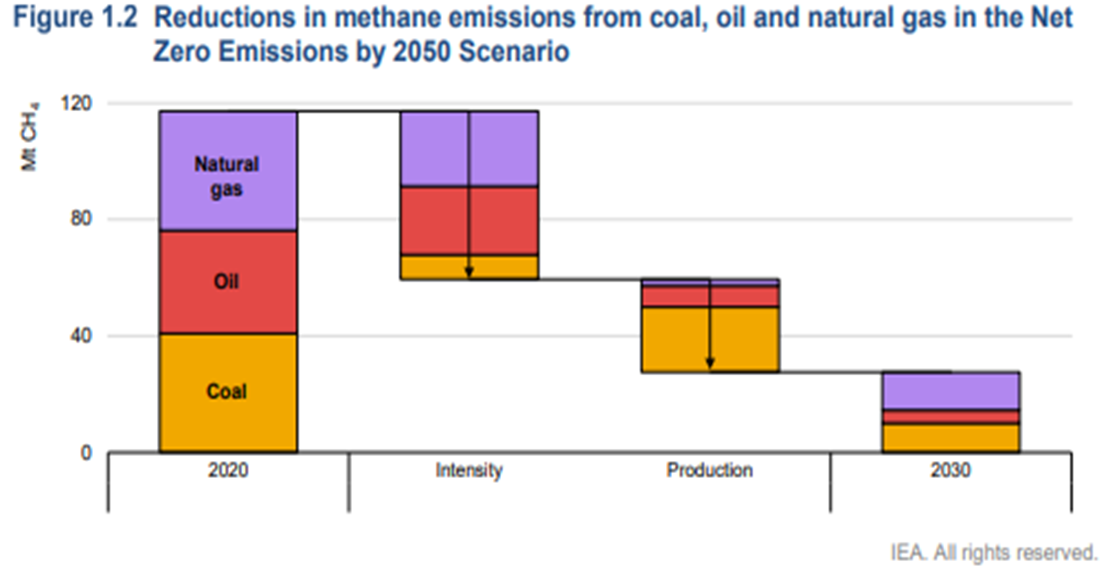

A couple of things worth highlighting in today's daily report – the first being Chevron’s move to join the net-zero club – focusing all eyes now on ExxonMobil in particular but also the rest of the US E&P crowd. Chevron will have some major challenges getting to net-zero and will likely face much of the same skepticism that bp, Shell, and TotalEnergies attracted in Europe initially and still face today. The Europeans have placed a lot of their bets on moving into renewable power – for the moment, Chevron is focused on moving to net zero in its own operations, which we read as biofuels and a lot of CCS. Given the acute shortage of international natural gas, it would make the most sense for the independent natural gas E&P companies and the LNG sellers to jump on the same boat. By promising low carbon natural gas and LNG, the industry is much more likely to gain support for the expansion that the world needs to counter some of the EIA assumptions around coal and petroleum product use from 2030 to 2050. Of course, it would be a whole lot easier for the US industry to do this if they had a value on carbon to work with! The chart below looks at one of the core clean-up issues, which is methane leakage. This is a subject we cover extensively in our ESG and Climate service linked here.