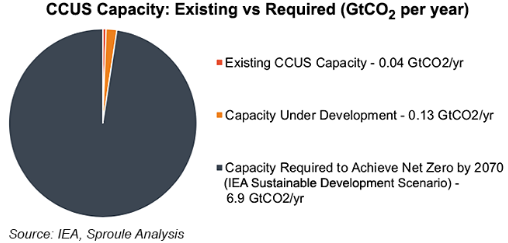

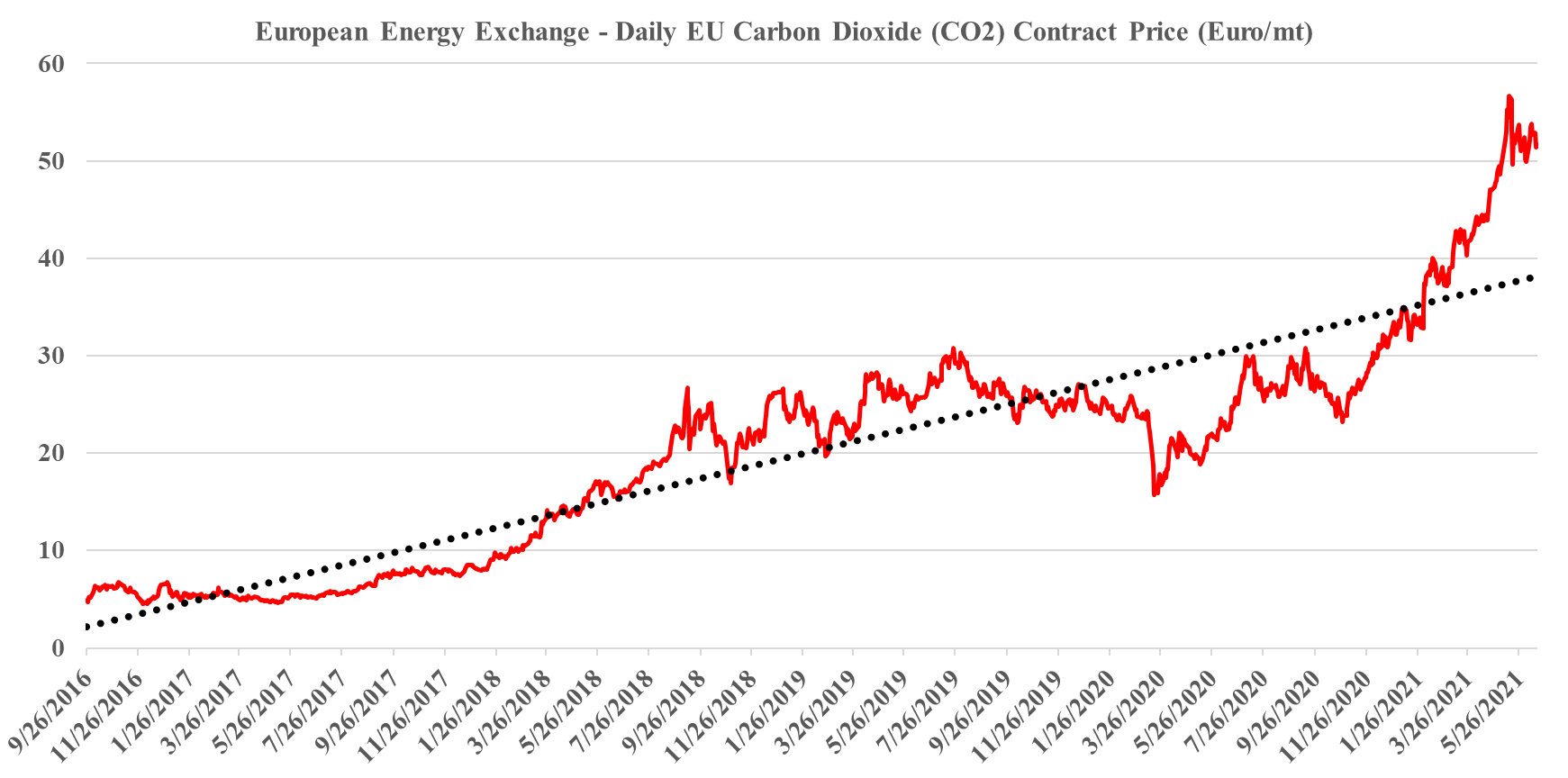

Most of the focus today is on carbon, in part because the CCS momentum is picking up, with more initiatives being announced daily all around the world, and partly because of the surge in European carbon prices as shown in Exhibit 1 from today's daily report. The IEA CCS projections in the Exhibit below, are likely low in our view, despite the significant investment needed to reach the target shown. In our ESG and climate report today we focus on many of the materials supply limitations that will likely emerge as the world tries to add wind and solar capacity at higher and higher rates. Our analysis of the IEA net-zero projections published earlier this year suggested that the IEA might be too ambitious on renewable power and that the balancing effect would likely be increased natural gas use versus its base case and more than forecast CCS. We have a long way to go to get there given the shortfall in the exhibit below, but at the same time, carbon prices are moving to make it happen. The European price has spiked again this week and is now slightly higher than $100 per ton of CO2, a level reached by the UK price late last week. At this level, we should see investments in Europe to abate carbon without additional local subsidies, or with minimal subsidies. The constraint in Europe will be finding inexpensive CCS locations. A $100 carbon price in the US would, in our opinion, drive a very significant investment in the US, not only in CCS capacity but also in new blue and green hydrogen capacity.

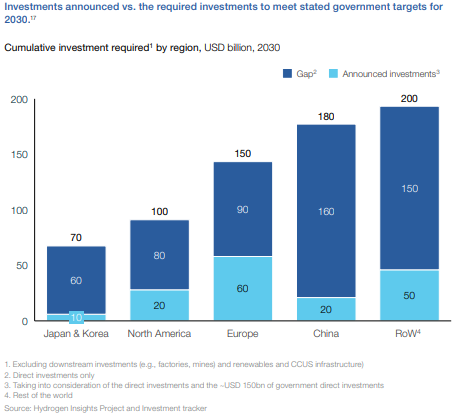

The hydrogen council chart below drags us away from 2050 and back to the more concerning near-term goals of 2030. The chart shows a significant gap in the current planned spend for hydrogen by region and the spending required to move far enough towards 2050 targets. This chart makes assumptions about the share of energy transition that will be met by hydrogen and given that it is the industry producing the chart, it is probably on the high side, but it is inclusive of both blue and green hydrogen. We have serious concerns about these totals being reached in general, but we see the target as completely unreachable without significant blue hydrogen (because of renewable power and electrolyzer capacity limits and we cannot rely on Canada to do all of the “heavy lifting” for blue hydrogen - see company section in today's daily report. The Biden administration may make more progress on emissions if the next order of business was just on CCUS rather than an omnibus bill that included CCUS but which could get held up in negotiations for months if it even gets passed.

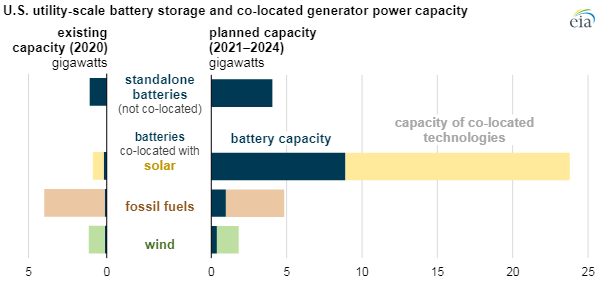

The battery storage investment chart below is interesting in that it shows significant pairing with Solar facilities and less with wind. If we are to meet the green hydrogen goals that many are optimistically predicting over the next 10 years, then the new wind and solar investments need to be paired with hydrogen and hydrogen-based swing power generation capacity. This is the only way that countries will develop effective hydrogen grids. Simply having one or two large hydrogen facilities and/or import facilities will result in very inefficient distribution models either for fuel cell vehicles or for heating and swing power generation. A distributed network for hydrogen makes much more sense and modular electrolyzers coupled with modular hydrogen power generators is a more holistic model, with much more flexibility than adding batteries. Granted, the battery technology is tested and available today, but the broader ambitions for hydrogen will not be met if we do not get out of the blocks soon.

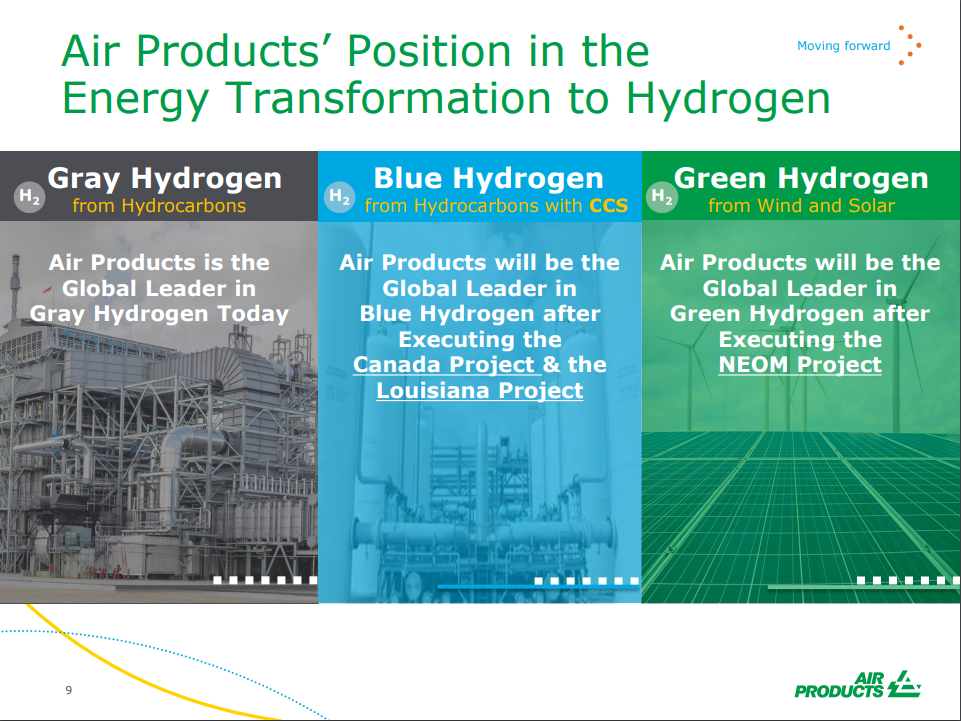

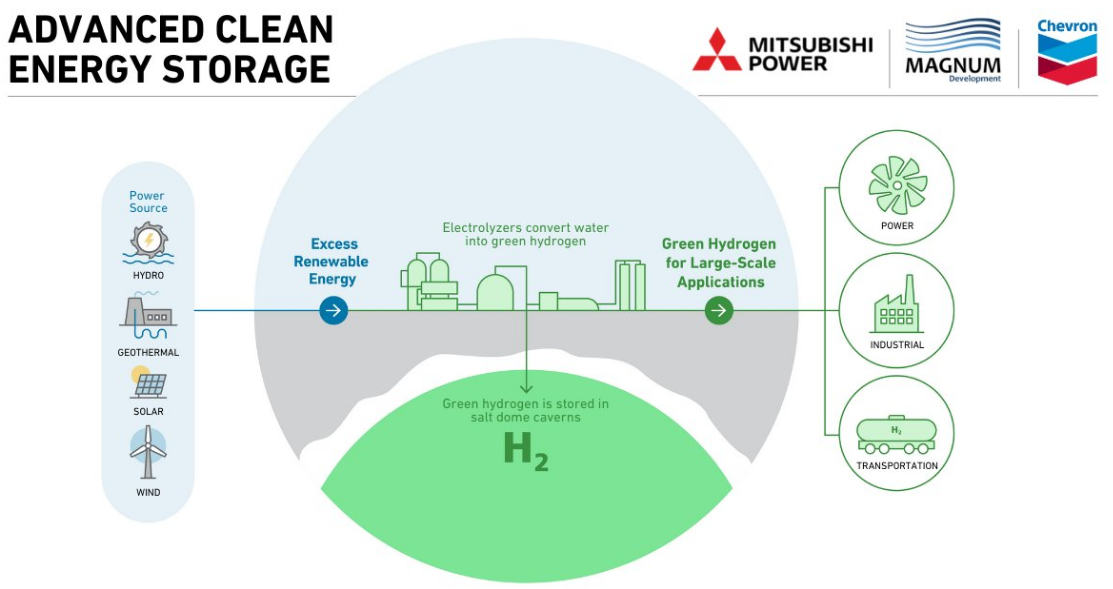

The Engine No1 headline and the Chevron headline are not necessarily the right way to think about the challenges for Chevron and whether or not the challenges are just really beginning for ExxonMobil. The Engine No 1 approach to ExxonMobil was not ESG focused and hit on a larger issue of very poor shareholder returns, with ESG/Climate only one-line item on a list. What Engine No 1 is doing now, is focusing more specifically on climate, and ExxonMobil is likely as large a target as Chevron on this basis. Last week in our Sunday report, we commented on how good the Chevron Gevo deal was for Gevo, but that it did not move the needle for Chevron. Chevron, ExxonMobil, and others are aggressively pursuing renewable fuels, mostly from waste and vegetable oils until the Gevo agreement, and there is another headline today about Chevron pursuing CCS opportunities with Enterprise and the chart below discusses a green hydrogen plan for Chevron. All of these initiatives do not sum to something that investors will take note of for any of these companies yet, and while they might be important building blocks towards a net-zero future, larger tangible investments are probably needed to get any investor buy-in. In the meantime, the activists have a lot of room to work.

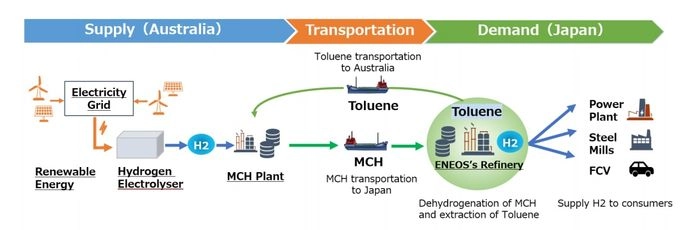

The exhibit below highlights one of the more significant constraints for green hydrogen, which is that the abundant low-cost power opportunities (strong wind and lots of sunshine) are often not where demand for hydrogen exists and the challenge is how to transport it. The problem with reacting it to make something else and then recovering it at the point of use or a distribution hub is that hydrogen is very light and you end up moving a lot of something else to get a little hydrogen. Air Products is looking at making ammonia in Saudi Arabia and shipping the liquid ammonia and the project below is looking at using toluene as a carrier in what appears to be a closed-loop with toluene moving one way and methylcyclohexane moving the other way. The liquid shipping would be cheap, but with the MCH route, only 5% of what you would be moving to Japan would be the green hydrogen. Using ammonia the green hydrogen content is slightly less than 18%, but you have to make the nitrogen on-site. The cost of making the nitrogen would be a function of the local cost of power and these remote locations should have very low-cost renewable power. In the example below, the opportunity is likely unique to the refinery structure and shipping opportunity and we doubt that it is easily replicated in a way that would be more economic than shipping ammonia or shipping compressed hydrogen itself.

Source: H2 Bulletin, August 2021

It is hard to ignore the number of headlines on hydrogen initiatives, today, highlighted in our ESG and climate report, as well as the acceleration in project announcements over the last several months. In the 80s in the UK, it was trendy to drive a VW Golf GTI – everyone had to have one – hydrogen has the same feel today – everyone has to have a project. The projects vary and fall into a handful of categories:

The primary reason for the flurry of carbon capture related headlines in the US over the last few weeks – and our analysis shows a significant step up – is because it looks like this will be the one technology/route to lower carbon emissions that will get a real boost from the infrastructure bill. There is bipartisan support for CCS because the fossil fuel industry sees it as a way to stay in the game and the unions believe that it will create jobs. This combination should garner enough votes to push it into the bill and get it passed, although the details around how CCS would be supported remain unclear. The infrastructure bill has very few real sources of income in it to offset the very high costs – something we will discuss on Sunday – and consequently giving a bigger tax break, through the 45Q program would create an even larger funding gap than we have today. The value/cost dynamic has to rise to get the activity that everyone is looking for and maybe that could be achieved by overlaying a carbon credit onto the program. Anyone exporting to Europe and concerned about the CBAM extending to natural gas, NGLs, chemicals, and polymers would likely consider CCS if they were eligible for 45Q and could also claim an offset on their exported products to neutralize the CBAM tax/fee.

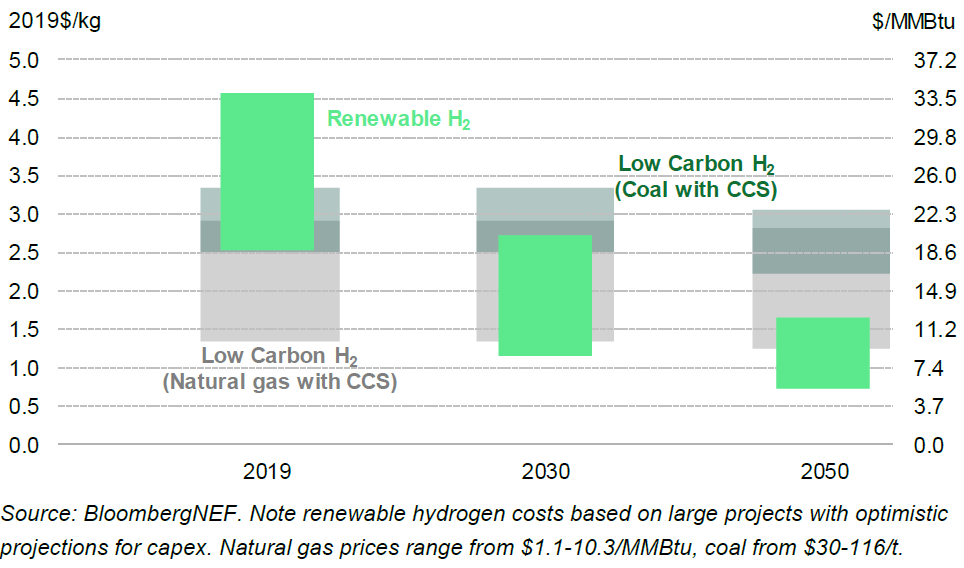

In our ESG and Climate report published today we focus on hydrogen and what we believe are some unrealistic cost/timing estimates for green hydrogen. One of our concerns is that the hope of cheap green hydrogen, and absent any other strong incentives, will put the brakes on other carbon abatement initiatives and if the cost of hydrogen does not fall we could reach 2030 having made little progress on any front.

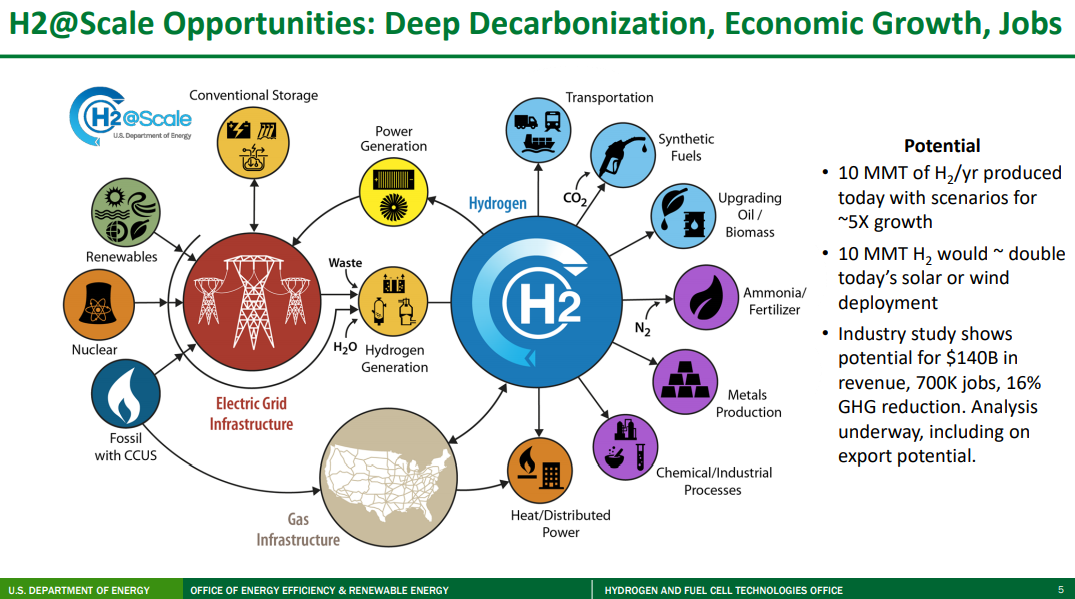

We will cover the very comprehensive DoE hydrogen work in more detail in the ESG report next week, but a couple of the charts from that work are worth mentioning today. The first picture below accurately depicts all of the potential uses of hydrogen and shows that over time it could solve a lot of “hard to solve” CO2 emission problems, especially where electricity cannot do the job efficiently. The reason why so many countries and companies are so interested in hydrogen is because of its potential versatility and because of its minimal carbon footprint (there is some carbon leakage in the full lifecycle of the production coming from construction around the plants themselves and infrastructure to use the hydrogen).