First, it is going to be an uphill struggle to get some common sense around the continued use of fossil fuels during any period of energy transition if the activists take away all resources from the energy industry – banking, PR, etc. While there is plenty of work to be done to minimize greenwashing, there is also plenty of work that needs to be done to explain why fossil fuels are still needed and how we can use them as cleanly as possible. If it becomes a business risk to bank or advise any company in the fossil fuel industry, while there will inevitably be workarounds, the net effect will be continued underinvestment, in production and in cleaning up the fuels and the concerns that we raised for natural gas in our Sunday Thematic will happen.

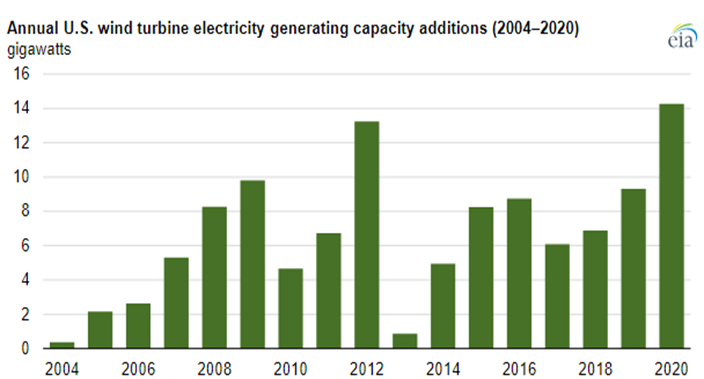

It should not be surprising that 2021 has seen a rebound in emissions as nothing has changed fast enough over the last 24 months in terms of renewable power additions and carbon abatement to offset more than the underlying growth in power demand, and based on what we are seeing in European and Asia LNG markets, we have fallen short of demand growth. The wind capacity chart below has one main conclusion – not enough. One of our main inflationary fears for 2022 is that both wind and solar installation rates need to step up meaningfully from current levels to make a difference – the IEA suggests that installation rates need to double (at a minimum). It has already proven difficult to meet installation targets in 2021, in part because of supply chain issues but also in part because of material shortages, all of which have led to rising installation costs, against the longer-term run of falling costs because of learning curve gains. We believe that costs will rise again in 2022 and 2023 as installers/projects compete for limited solar module and wind turbine components

While we would generally avoid quoting work from a company that we might consider a peripheral competitor, we are happy to do so when it backs up one of our central themes – in this case, inflation in renewable power costs. The quote is taken from the Wood Mackenzie report flagged article linked here and discusses a view on how challenges that renewable power installers have faced in 2021 will extend into 2022. The quote talks about shortages of renewable power equipment, and the obvious consequence will be higher prices for that equipment, especially as raw material prices for components remain high and possibly move higher. In our ESG and Climate report today, we talk about the need for some commonsense oversight such that impractical ESG investing targets do not limit the ability of producers of critical fuels and materials to operate.

International natural gas prices are hitting new highs this week, both on an absolute basis and relative to the US - see both charts below. At the same time, we see new contracts being signed for US LNG to move to China and Europe, but mainly China. This is happening despite significant renewable power investments globally in 2021 and it would appear that many have underestimated energy demand growth in projections and policy. The other net effect of the supply/demand imbalance this winter and possibly through 2022 will be increased coal use in Europe and the US, with local governments unable to meet near-term climate goals, especially in Europe, but also in parts of Asia and, at the same time keep the people warm and the lights on. In our ESG and Climate piece tomorrow we will focus on one highly unpopular but likely very practical opportunity for coal as part of a planned energy transition program, and it is likely that, while climate goals may not need to change, some socially unpopular decisions around the use of fossil fuels will be needed to prevent even more socially unpopular inflation or absolute shortages.

When China announced its 2060 net-zero goals we dedicated one of our ESG and Climate pieces to the topic - China: A Challenge With 2060 Goal But Also A Possible Edge - concluding that this would likely drive considerable competitive advantage for China assuming that others would bear the costs of new technology learning curves and China would get the solutions more cheaply. In interim China would have lower costs of manufacturing because of the delayed net-zero implementation. With the Biden administration now pushing for a coordinated 2050 commitment for the US, some of the burdens of early costs that China could benefit from also fall on the US. In one of the headlines (from today's report), there is criticism of the European CBAM and questions around whether it could work. The reality is that it, or something like it, has to work, otherwise asymmetric climate policies will create pockets of competitive advantage - potentially very damaging to those spending more.

In our ESG and Climate report tomorrow we are focusing on the very wide range of carbon prices and the structures of the various emission reduction incentive schemes, with a focus on what it does to the competitive landscape within the impacted markets. For example, with the government subsidy being offered to BASF and Air Liquide for the CCS project in Antwerp, some level of competitive edge will be granted to the companies, because similar subsidies might not be available to others. Last week we discussed the very wide range of potential carbon abatement costs for companies in the same business, driven by technology and geography. If we add to that the potential for some projects to attract subsidies, while others do not, we change the landscape of the competitive playing field. Could we, for example, see BASF shutter production in Germany, where abatement costs are high, and move more manufacturing to Antwerp – something likely to be very unpopular with the German government and trade unions. This is more problematic in Europe because of the open trade policy. For Germany to give the same benefit that BASF has at Antwerp to chemical manufacturers in Germany could be prohibitively expensive given the much higher inland costs of CCS in Europe, assuming any permits would be issued. Alternatives to CCS, such as the electrification of industrial heating processes or the use of hydrogen as fuel might be equally expensive. We see some of the select European subsidies possibly causing discord between the member states.

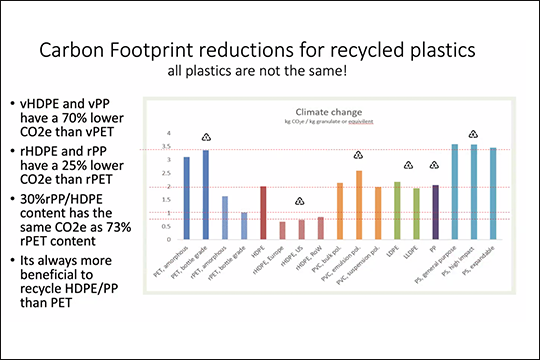

It is interesting to watch the pivot between recycled versus virgin polymer to the carbon footprint of the various options as outlined in the chart below. We are assuming that the numbers in the chart are averages as there is a sizeable range for everything. As we note in today's daily report, ethylene feedstock will impact the carbon footprint of ethylene and consequently, the footprint of polyethylene – HDPE made from ethane based ethylene in the US where the ethylene producer is recycling hydrogen back into the furnaces, will have a much lower carbon footprint than HDPE made from naphtha based ethylene in Europe, for example. On the recycling side, there will also be a range based on transportation costs for collection and sorting and then distribution to a customer.

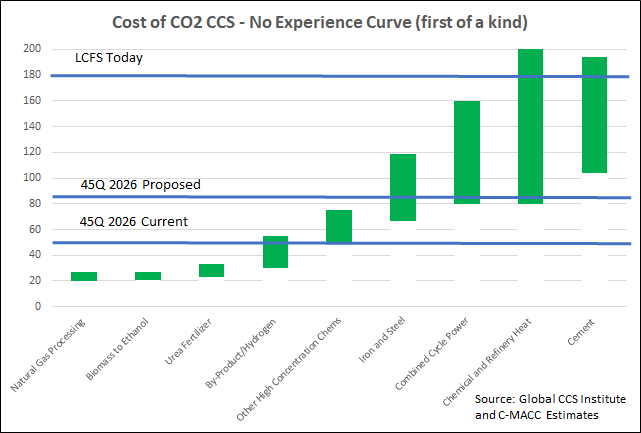

We want to focus today on the headlines around the possible increase in the 45Q CCS credit in the US and discuss the false logic of those that are objecting to it. There is no scenario where the US can move to a lower emissions power and transport profile while avoiding runaway inflation and social disorder without the continued use of fossil fuel-based power and transportation fuels for decades. The reliance on these fuels should and will decline over the years, but it is unreasonable to expect a transition that causes it to stop overnight. In the meantime, CCS is a mechanism that would allow fossil fuels to play a part with a much lower emissions footprint, and given that the CO2 impact on global warming is cumulative, if we can capture and store several billion tons of CO2 underground over that transition period it should be a good thing. Members of the Sierra Club and others would do well to look at the energy inflation problems in Europe and the move this week to put natural gas and nuclear back in the energy transition mix (too late in our view) because the move to renewables cannot keep pace with demand, which will grow faster as more EVs hit the road. The proposed 45Q credit is shown in the chart below vs. the current credit, the LCFS credit, and estimates of CCS costs.

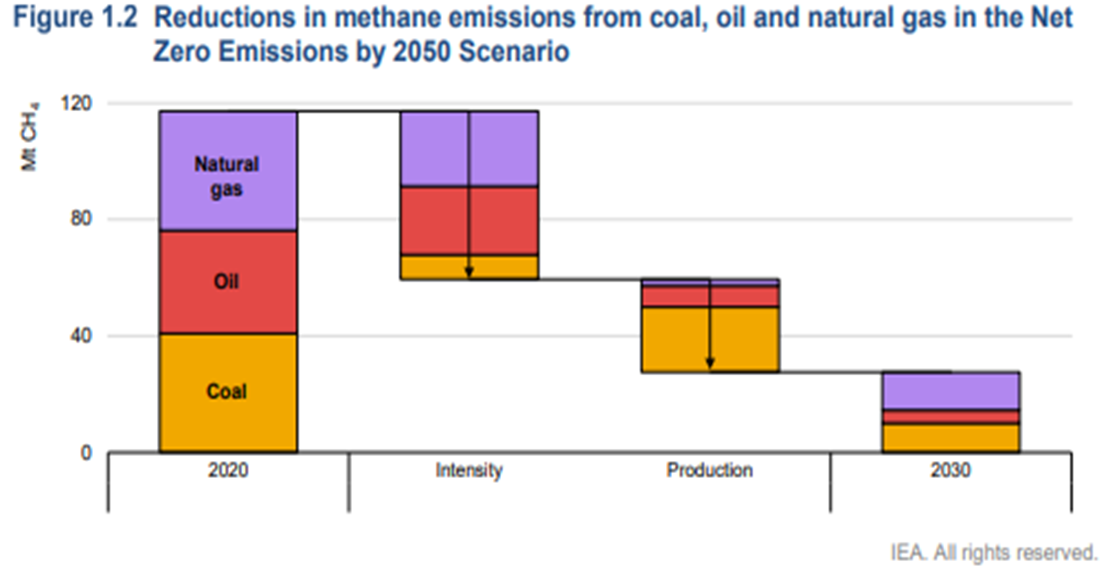

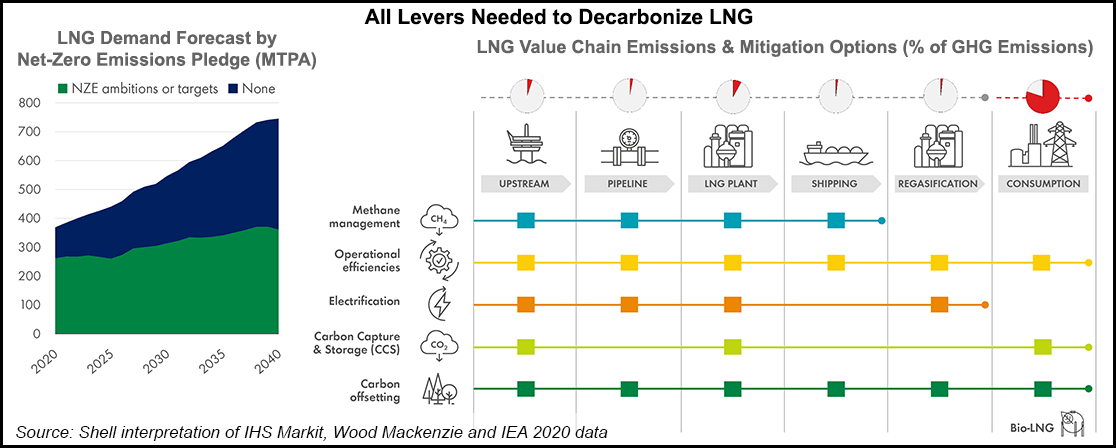

A couple of things worth highlighting in today's daily report – the first being Chevron’s move to join the net-zero club – focusing all eyes now on ExxonMobil in particular but also the rest of the US E&P crowd. Chevron will have some major challenges getting to net-zero and will likely face much of the same skepticism that bp, Shell, and TotalEnergies attracted in Europe initially and still face today. The Europeans have placed a lot of their bets on moving into renewable power – for the moment, Chevron is focused on moving to net zero in its own operations, which we read as biofuels and a lot of CCS. Given the acute shortage of international natural gas, it would make the most sense for the independent natural gas E&P companies and the LNG sellers to jump on the same boat. By promising low carbon natural gas and LNG, the industry is much more likely to gain support for the expansion that the world needs to counter some of the EIA assumptions around coal and petroleum product use from 2030 to 2050. Of course, it would be a whole lot easier for the US industry to do this if they had a value on carbon to work with! The chart below looks at one of the core clean-up issues, which is methane leakage. This is a subject we cover extensively in our ESG and Climate service linked here.

The carbon capture plans lacking a place to put the CO2, suggested in the two connected stories linked here (link 1, link 2), echo something that we have been highlighting for a while. There have been several press releases with respect to CCS – partnerships – plans to accompany new investments – gathering schemes for the ethanol industry, etc. but none have any specificity around where they will put the CO2. The Houston team, discussed in a recent report is talking about offshore Texas, and given both ExxonMobil and Chevron in the partnership, we do not doubt that there is a plan, but in general, the permit activity at the EPA is, we understand, quite limited today. To apply for a class 6 permit, applicants need to have a detailed analysis of the sub-surface that they plan to target, and once you have identified a location, there are likely at least 18 months of work to get into shape to submit the permit. Some of the oil majors may be able to move faster on acreage that they already have seismic models for, but it is a long process – we wrote about the need for 45Q to change in both value and duration in our recent ESG and Climate Piece.