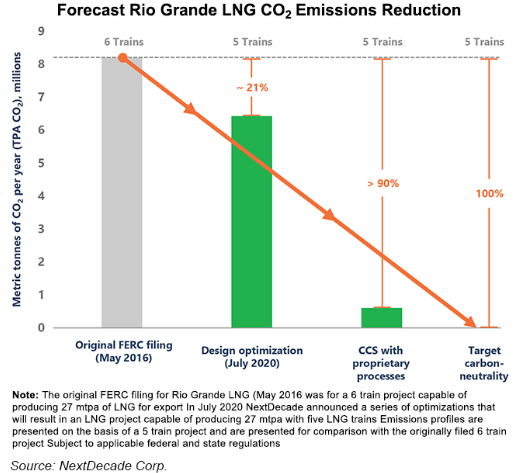

In our ESG and Climate piece yesterday we briefly discussed the mid-west carbon capture projects, questioning their economic viability. Two of the most expensive components of any CCS project are pipelines and compression costs and we cannot see how a long network of pipe in the mid-west to pick up what are essentially small volumes can work economically. These projects are reliant on very high LCFS-like credits, and as we showed in last week’s report, LCFS credits have fallen this year and could fall further. The pipeline right of way issue is another major hurdle and we have seen growing resistance to pipelines of any sort over the last few years. Those who oppose CCS in principle could cripple these mid-west plans simply by co-opting enough land-owners on the path of the proposed pipelines and refusing access. We are supporters of CCS, but have done substantial work on economics and show that the process only begins to make economic sense if the sequestration is close to the emissions. Relying on possible artificially high carbon prices to justify the projects will only lead to pain, assuming the pipeline right of ways can be obtained.

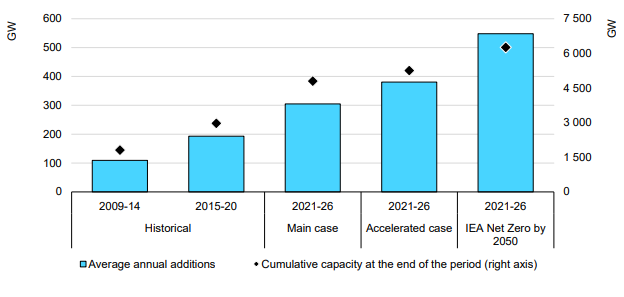

The core message of the IEA analysis published today is around how renewable power rates of investment remain far too low and need to more than double immediately to meet net-zero goals – see below. This analysis is very supportive of our renewable power inflation thesis, as none of the renewable power component manufacturers can double production either cheaply or quickly, and none of their suppliers has that much spare materials capacity. On the solar front, we may have the additional problem of regional production concentration. China has the largest share of capacity for solar module capacity and now has much more aggressive plans for solar power domestically. We could see China-based components stay in China, exaggerating shortages outside China. The IEA has an accompanying report today on the possible impact of commodity pricing on solar and wind pricing and it is also linked here – these reports were published this morning and we will cover them in more detail in next week's ESG and Climate report. More on this in today’s ESG and Climate report.

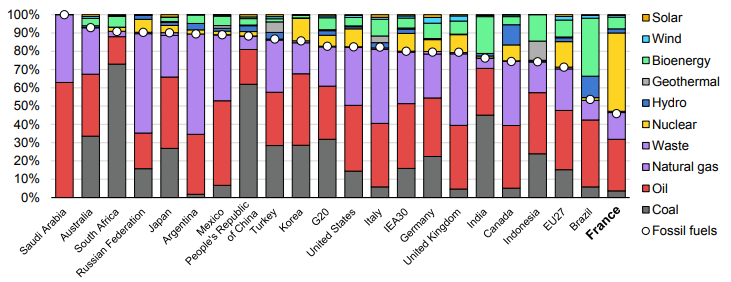

The fuel use data in the Exhibit below is very much a function of geology and the good and bad luck associated with it. The large hydrocarbon users' consumption patterns are a function of what they have – if you have a lot of coal, you use a lot of coal. The significant build-out of nuclear in France is partly because of Frances’ exceptional track record with the technology but also because the country does not have anything else to fall back on. Japan’s nuclear component was much higher before Fukashima. It is, however, worth noting the almost insignificant share of wind and solar anywhere, and then to put this into context with the collective ambitions, not just for 2050, but for the much shorter 2030 targets.

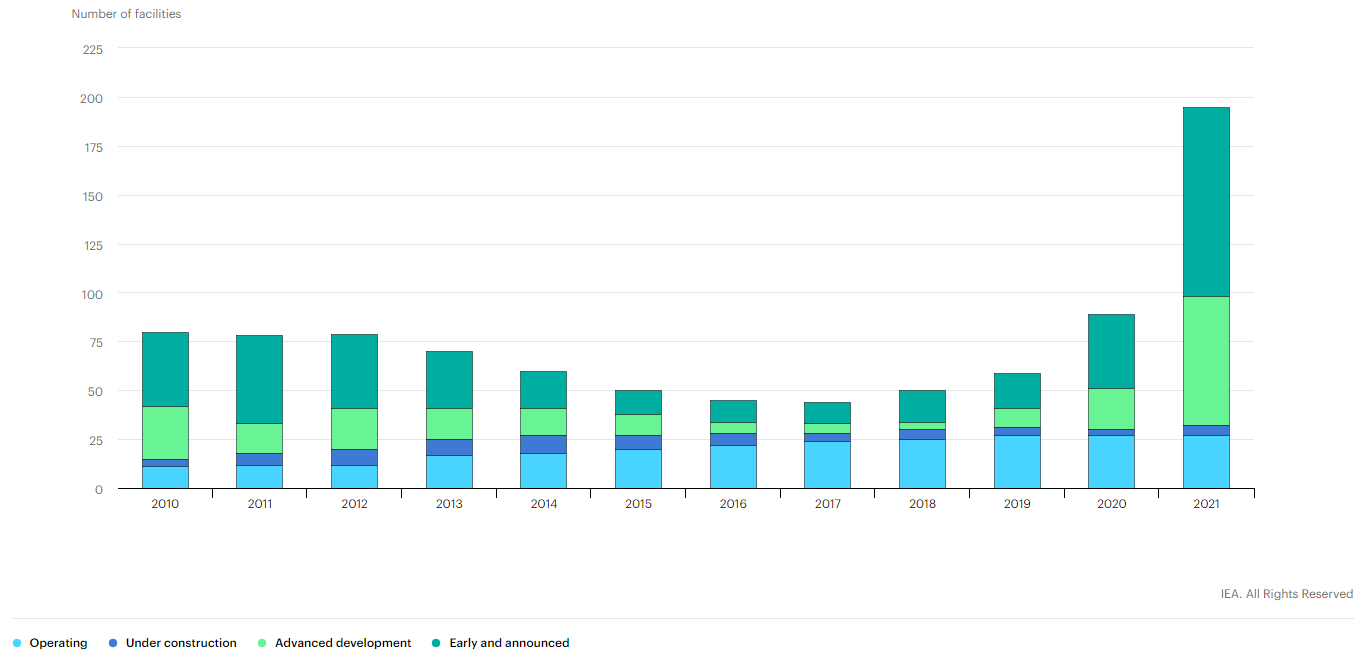

We note the IEA work on CCUS in several charts below and this is good timing relative to our ESG and climate report this week – which focused on carbon pricing, something we believe is necessary to promote more real activity in CCUS. In the Exhibit below, it is important to note how many projects are in “development” rather than operational or under construction. It is also worth noting that the number of projects under construction has not grown since 2019. One of the reasons for this is that increased activity at the planning stage is then followed by a delay associated with permitting, which depending on the region can take 2 plus years. The other constraint is uncertainty, with many of the projects under consideration waiting for something to change, either local values of CO2 or mandates or direct government support. For example, the large project planned for Houston and championed by several oil, power, and chemical companies is unlikely to move forward without a higher tax credit for CO2 sequestration or without some other incentive. The mid-West projects targeting the ethanol industry will also need permits, not just for the wells but also for the many hundreds of miles of proposed pipelines.

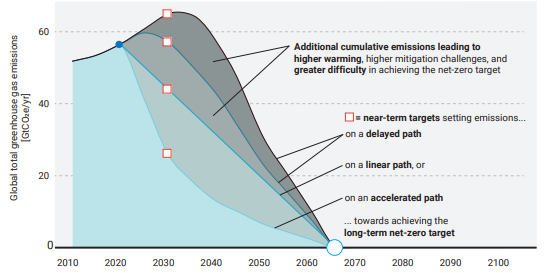

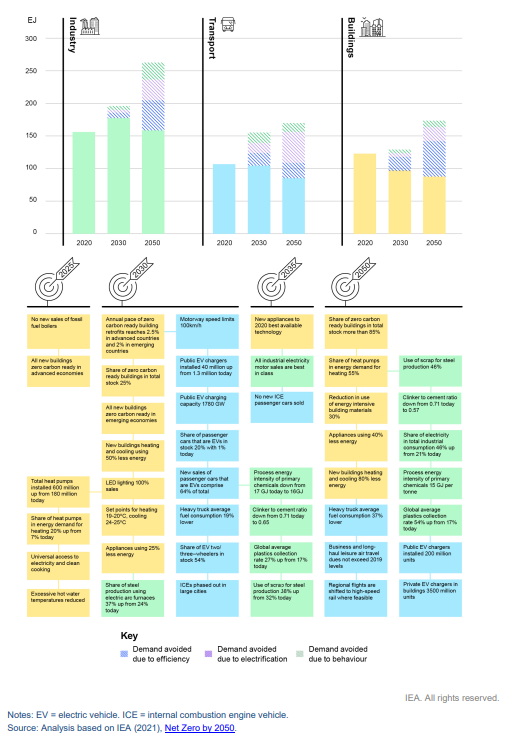

In a media interview earlier this week (more details to follow) we were involved in a discussion about inflation and specifically energy. The discussion covered much more than this, but the chart below is perhaps one of the easier ways of showing where our concern lies, and it ties directly to the behavioral patterns that are emerging concerning climate change and ESG focused investing. As noted in the title of the chart, the likelihood that the linear path from here to net-zero will work is very low, given that we would need global government coordination now, and we are far from it. The other scenarios are much more likely, at least in the early years, and they call for an increase in emissions, which implies growing demand for fossil fuels and other materials that have a high emissions footprint. If you are an oil or gas producer and you look at the chart you could quickly conclude that while your products are in demand today and likely to be in growing demand for several years, the longer-term outlook is very unclear. This might slow down your investment plans, or at least make you think twice about the shorter lead-time projects – such as on-shore and shale-based. However, it could kill any longer-term offshore/deepwater projects that take many years to bring on stream. Today we see energy investment hesitancy everywhere (see our Chemical Blog), but at the same time, we do not see the global coordination to drive a faster energy transition, assuming we had the materials and the investment dollars to move any faster. The risk that we run out of produced fossil fuels from time to time over the next 3-5 years is very high.

In our ESG and Climate report tomorrow we are focusing on the very wide range of carbon prices and the structures of the various emission reduction incentive schemes, with a focus on what it does to the competitive landscape within the impacted markets. For example, with the government subsidy being offered to BASF and Air Liquide for the CCS project in Antwerp, some level of competitive edge will be granted to the companies, because similar subsidies might not be available to others. Last week we discussed the very wide range of potential carbon abatement costs for companies in the same business, driven by technology and geography. If we add to that the potential for some projects to attract subsidies, while others do not, we change the landscape of the competitive playing field. Could we, for example, see BASF shutter production in Germany, where abatement costs are high, and move more manufacturing to Antwerp – something likely to be very unpopular with the German government and trade unions. This is more problematic in Europe because of the open trade policy. For Germany to give the same benefit that BASF has at Antwerp to chemical manufacturers in Germany could be prohibitively expensive given the much higher inland costs of CCS in Europe, assuming any permits would be issued. Alternatives to CCS, such as the electrification of industrial heating processes or the use of hydrogen as fuel might be equally expensive. We see some of the select European subsidies possibly causing discord between the member states.

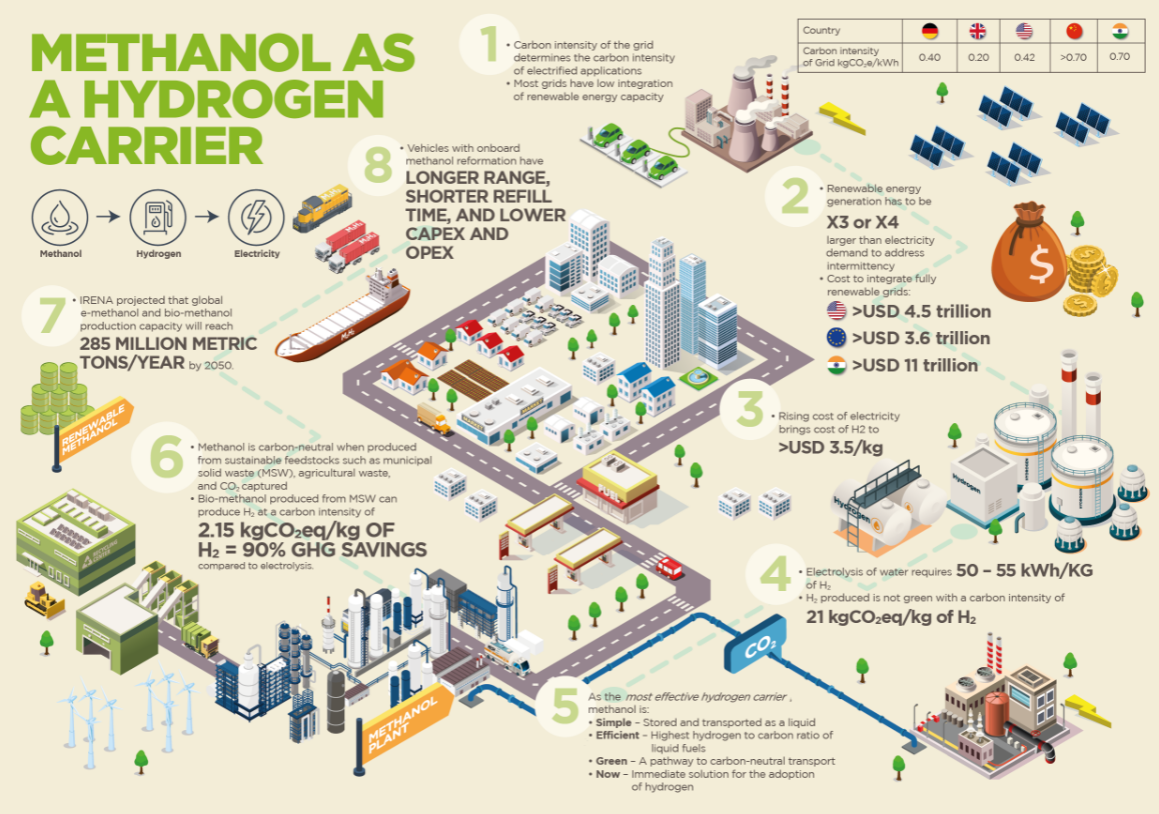

We are going to focus our Sunday Thematic this week (will be found here) on a couple of related topics: alternative technologies that only make sense when prices are high, and whether this has changed with ESG and climate pressure, and ESG solution fixation – “methanol is the only solution” – see infographic below – or it’s hydrogen or ammonia or batteries. Sticking with the theme that seems to have hit a chord with COP26 attendees and something that we discussed in a report around carbon capture several months ago – we cannot let a foolhardy quest for “perfect” get in the way of more economic “good enough” solutions. The emission issues are generally site and process specific and different solutions will be more practical and affordable for different processes and in different geographies – there is no “one size fits all” solution.

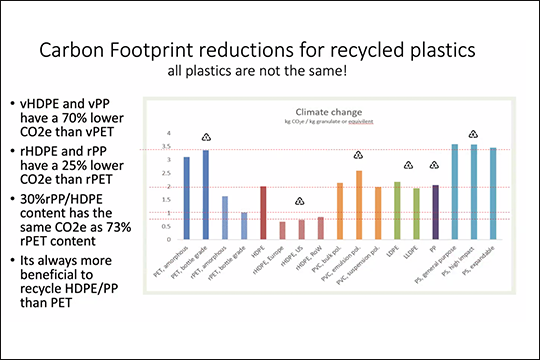

It is interesting to watch the pivot between recycled versus virgin polymer to the carbon footprint of the various options as outlined in the chart below. We are assuming that the numbers in the chart are averages as there is a sizeable range for everything. As we note in today's daily report, ethylene feedstock will impact the carbon footprint of ethylene and consequently, the footprint of polyethylene – HDPE made from ethane based ethylene in the US where the ethylene producer is recycling hydrogen back into the furnaces, will have a much lower carbon footprint than HDPE made from naphtha based ethylene in Europe, for example. On the recycling side, there will also be a range based on transportation costs for collection and sorting and then distribution to a customer.

The IEA has published another report looking at energy intensity progress – noting that the rate of improvement in energy use is likely not fast enough to do its part in achieving net-zero needs. It is a comprehensive report (linked here) and we have chosen a couple of charts as you can see in today's daily report. The more interesting conclusion within the analysis may be that the IEA expects plastic collection for recycling to rise from 17% to only 27% by 2035. While this is a global average and will differ by country and likely by material, the overall rate looks low (but probably reasonable) and too low to allow packagers to meet recycle content goals, many of which are either 2025 or 2030 targets. We discuss some of the evolving packaging challenges in our ESG and Climate report today.

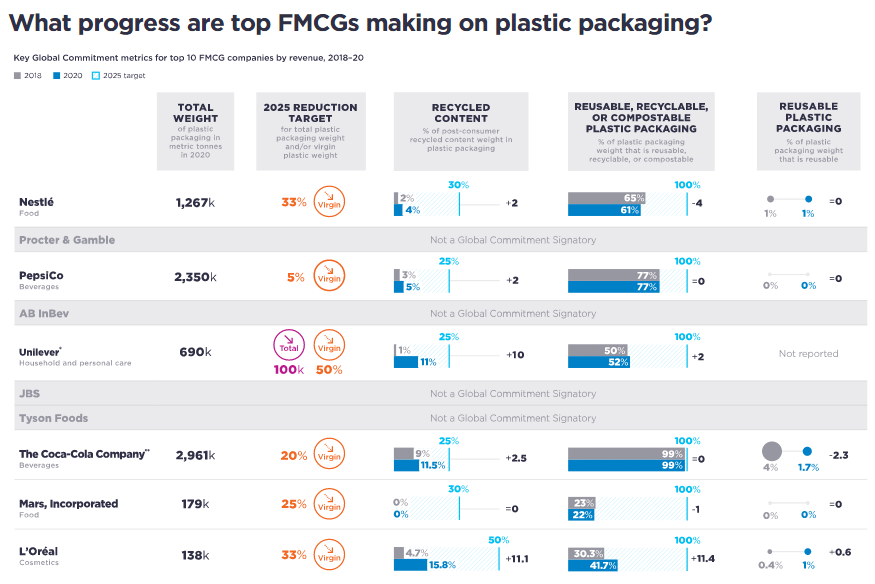

The chart below on recycling progress by the major FMCG companies is timely as it bumps into plenty of “national recycling day” headlines which include as many stories around recycling polymers into new applications as stories about like for like recycling. The more polymer that moves through collection and sorting and into roadbeds or composite particleboard replacement, etc., the less there is available for the FMCG companies to meet recycling goals. We see this as a major opportunity for the renewable polymer makers, but it is unlikely that there will be enough renewable-based polymers available to close the 2025 gap for most of the companies listed below. What is likely, in our view, is that the packagers will embrace chemical recycling as a way to increase their recycled content and will strike very specific deals with those able to show a chain of custody from collection through new polymer production.