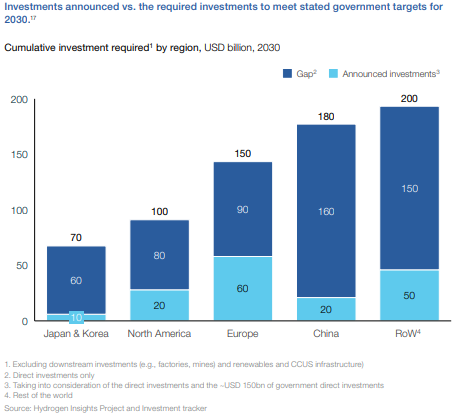

The hydrogen council chart below drags us away from 2050 and back to the more concerning near-term goals of 2030. The chart shows a significant gap in the current planned spend for hydrogen by region and the spending required to move far enough towards 2050 targets. This chart makes assumptions about the share of energy transition that will be met by hydrogen and given that it is the industry producing the chart, it is probably on the high side, but it is inclusive of both blue and green hydrogen. We have serious concerns about these totals being reached in general, but we see the target as completely unreachable without significant blue hydrogen (because of renewable power and electrolyzer capacity limits and we cannot rely on Canada to do all of the “heavy lifting” for blue hydrogen - see company section in today's daily report. The Biden administration may make more progress on emissions if the next order of business was just on CCUS rather than an omnibus bill that included CCUS but which could get held up in negotiations for months if it even gets passed.

The Dow chart below was included in the presentation around the Canada project and repeated today in the earnings call. We have talked about the Canada project at length as well as the more recently announced Air Products blue hydrogen project in the US. The more interesting debate from here is what will happen next. Are Dow’s and Air Product’s phones ringing off the hooks with potential customers saying “we want some of that”, or is it quieter? We suspect that the phones are ringing and ringing a lot. Perhaps because people genuinely want the low carbon polyethylene or hydrogen, but also perhaps because users of polyethylene and hydrogen are likely obligated to find out more so that they can explore both the opportunities of buying from Dow or Air Products, or evaluating what their alternatives might be. We suspect that a surge in genuine customer interest is likely, good for both Dow and Air Products, but also good for others either considering decarbonizing projects or offering a carbon-free alternative already. See our ESG and Climate piece from yesterday for more on this.

We want to focus on carbon use today, in part because we have written extensively on sequestration recently, in part because of the headline highlighted below, and in part, because we need something fresh for our ESG and Climate report tomorrow! Carbon use does not get much press beyond EOR, but there are emerging technologies and there is a lot of R&D spending – on how to collect CO2 more efficiently and on what it might then be used for. We suspect that almost everything being looked at will have some application, but that there will be limits to those applications and they will likely be niches in nature, but not necessarily unprofitable.

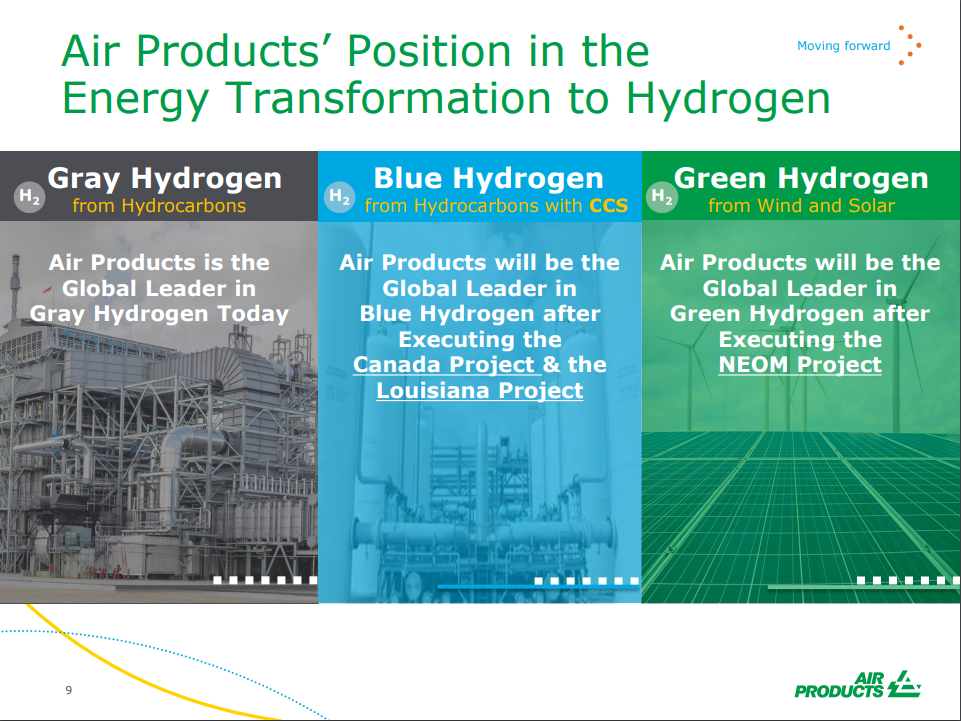

We expect to see a step up in chemical companies parading their green credentials – or plans for more green credentials, not just because COP26 is ahead but because it has now become a competitive issue. Dow’s view that it may be able to sell low carbon polyethylene in the US at a premium to regular polyethylene reflects a fairly rapidly changing narrative with customers, many of whom are also trying to accelerate their green credentials. For a couple of years, we saw packaging companies, for example, talk in broad terms about ambitions around recycled/renewable content, carbon footprints, etc. Now we are seeing the results of them trying to put their ambitions into practice and they are looking for tangible solutions from their suppliers to help them meet the pledges that they have made to consumers. For many of the packagers, the cost of the packaging is a very small component of the product cost and we would expect the packagers to look at more expensive packaging solutions if it gives them a better label. In the Air Products chart below, the company is using the La Porte start-up to remind us that it is already a huge player in hydrogen and hydrogen infrastructure. See our recent ESG and Climate Report.

The gaps in the exhibit below are not surprising as 2050 is a long way away and we would not expect all of the needed capacity to be announced or pledged yet, especially as many companies are still weighing alternatives. For example, as an ethylene producer, you have 5 paths – hydrogen as a furnace fuel – electric power as a heating medium – stick with what you have and use CCS – find an alternative route to make the polymers – make alternative polymers.

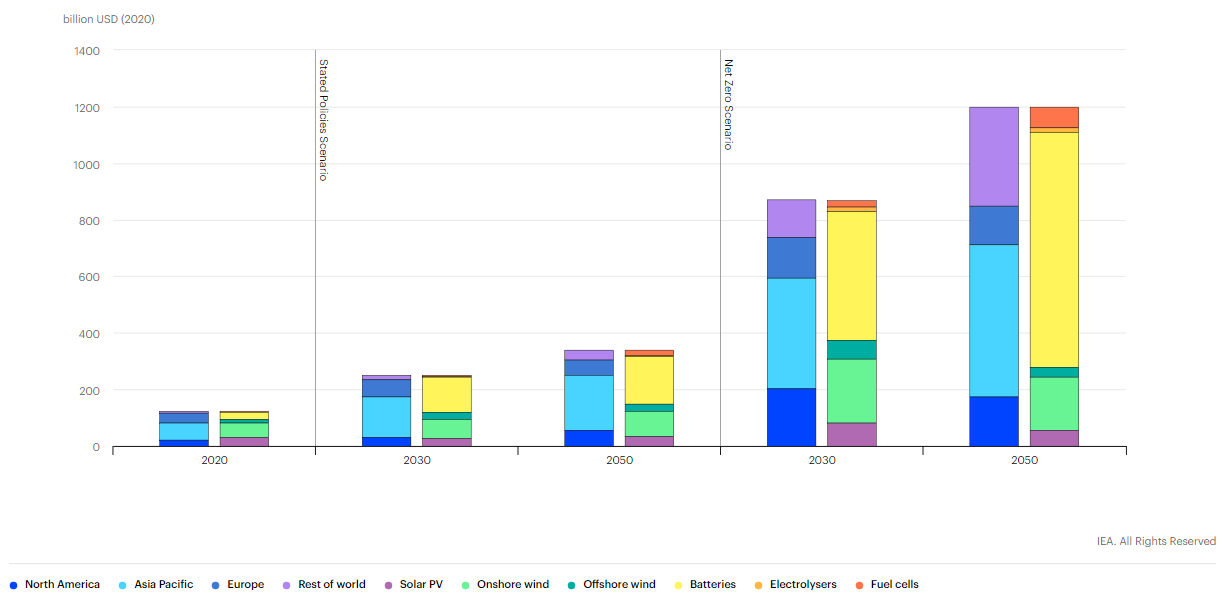

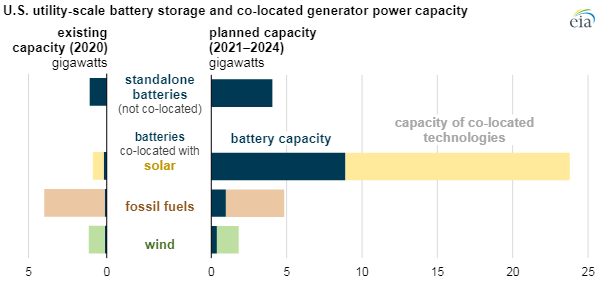

The battery storage investment chart below is interesting in that it shows significant pairing with Solar facilities and less with wind. If we are to meet the green hydrogen goals that many are optimistically predicting over the next 10 years, then the new wind and solar investments need to be paired with hydrogen and hydrogen-based swing power generation capacity. This is the only way that countries will develop effective hydrogen grids. Simply having one or two large hydrogen facilities and/or import facilities will result in very inefficient distribution models either for fuel cell vehicles or for heating and swing power generation. A distributed network for hydrogen makes much more sense and modular electrolyzers coupled with modular hydrogen power generators is a more holistic model, with much more flexibility than adding batteries. Granted, the battery technology is tested and available today, but the broader ambitions for hydrogen will not be met if we do not get out of the blocks soon.

In our ESG and Climate report yesterday we focused on sustainable aviation fuel, discussing a recent report from Shell and Deloitte, which shows some of the challenges with getting the aerospace industry to net zero. The report focused on the need for sustainable aviation fuel now, and in large volumes, as this is the only thread that the industry can pull on today – synthetic fuels (from CO2 and hydrogen will be uneconomic for decades, and neither electric powered or hydrogen-powered aircraft are going to be a solution before 2050). The bp, Delta, and Boeing linked headline is one of many that we expect to see as the need for near-term progress is urgent, given the scale of investment required. See yesterday’s report for more detail.

The charts below both support our view that we will see continued inflation in renewable energy costs, rather than the deflation that is baked into all of the forward models. It is easy to forget that some of the early solar installations are coming to the end of their useful lives and are retiring – these are gaps that new solar will need to fill. Wind power has the same issue, as many of the original wind farms need equipment replaced and the introduction of recyclable wind turbine blades has been in recent manufacturers' announcements. When we see analysis of who is going to use which tranche of new renewable power for which new hydrogen project we see major gaps in the power demand analysis, in part related to power demand growth at the domestic consumer – because the more rapid introduction of EVs – and in part because or retirement of facilities and the need to replace them.

Last week, and in our dedicated ESG and climate report this week, we talked about the challenges of shipping hydrogen, and the linked bp project for Western Australia will have the same problem to solve – choosing ammonia according to the announcement over the very inefficient toluene/cyclohexane option we discussed last week. The appeal of Western Australia is the unpopulated available land that has little alternative use and sees abundant sunshine. The bp project assumes that the facility can buy attractively priced renewable power from third parties, but the company must have a specific power project in mind for the bulk of the electricity needed. The stumbling block here will likely be when the power project(s) bid out the solar module contract, find out that the suppliers are sold out and are asking higher prices to cover reinvestment and higher material prices, and then have to go back to bp with a much higher than expected cost of power. The advantage of solar and wind projects is that inflation only impacts upfront capital costs, which can be amortized over the life of the project – feedstocks are free! That said, most of the announced projects have declining capital costs per megawatt in their planning assumptions today.