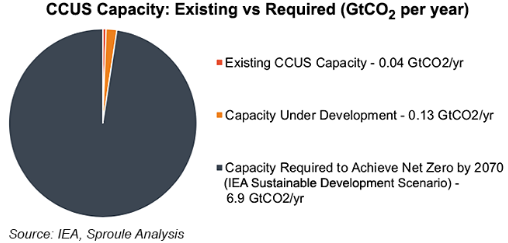

Most of the focus today is on carbon, in part because the CCS momentum is picking up, with more initiatives being announced daily all around the world, and partly because of the surge in European carbon prices as shown in Exhibit 1 from today's daily report. The IEA CCS projections in the Exhibit below, are likely low in our view, despite the significant investment needed to reach the target shown. In our ESG and climate report today we focus on many of the materials supply limitations that will likely emerge as the world tries to add wind and solar capacity at higher and higher rates. Our analysis of the IEA net-zero projections published earlier this year suggested that the IEA might be too ambitious on renewable power and that the balancing effect would likely be increased natural gas use versus its base case and more than forecast CCS. We have a long way to go to get there given the shortfall in the exhibit below, but at the same time, carbon prices are moving to make it happen. The European price has spiked again this week and is now slightly higher than $100 per ton of CO2, a level reached by the UK price late last week. At this level, we should see investments in Europe to abate carbon without additional local subsidies, or with minimal subsidies. The constraint in Europe will be finding inexpensive CCS locations. A $100 carbon price in the US would, in our opinion, drive a very significant investment in the US, not only in CCS capacity but also in new blue and green hydrogen capacity.

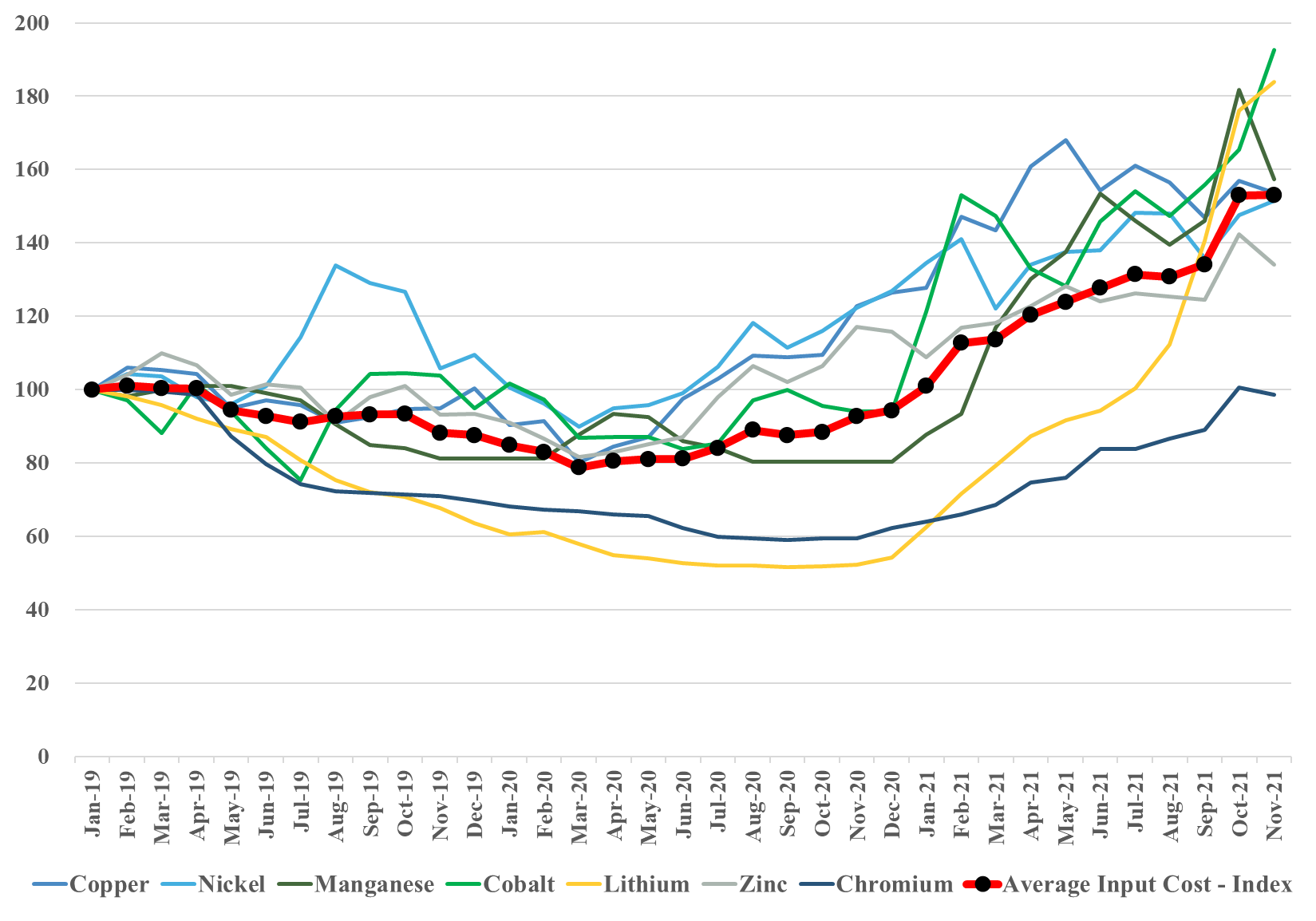

We focus today on raw material inflation and use the IEA analysis of materials demand (excluding steel and aluminum) in EVs and renewable power, creating a price index for the materials in question. This index is a straight average, but we will develop indices for specific sub-industries and include these in our next ESG and climate report. What is important is that the index below is up over 50% since the beginning of 2019 and this is before many of the EV plans and power plans move from planning to construction. We have highlighted inflation risk for more than a year now and remain very concerned that when many of the new auto plants start and many of the incremental renewable power facilities move from planning to equipment purchasing, we will see bottlenecks and faster price increases. See more in today's daily report.

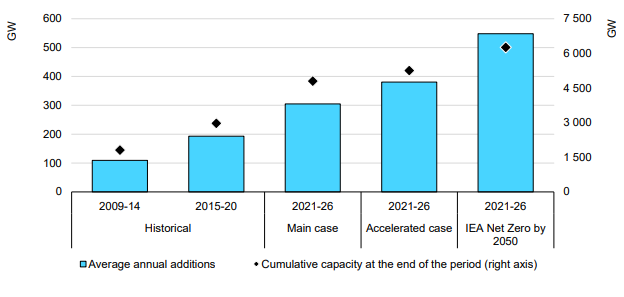

The core message of the IEA analysis published today is around how renewable power rates of investment remain far too low and need to more than double immediately to meet net-zero goals – see below. This analysis is very supportive of our renewable power inflation thesis, as none of the renewable power component manufacturers can double production either cheaply or quickly, and none of their suppliers has that much spare materials capacity. On the solar front, we may have the additional problem of regional production concentration. China has the largest share of capacity for solar module capacity and now has much more aggressive plans for solar power domestically. We could see China-based components stay in China, exaggerating shortages outside China. The IEA has an accompanying report today on the possible impact of commodity pricing on solar and wind pricing and it is also linked here – these reports were published this morning and we will cover them in more detail in next week's ESG and Climate report. More on this in today’s ESG and Climate report.

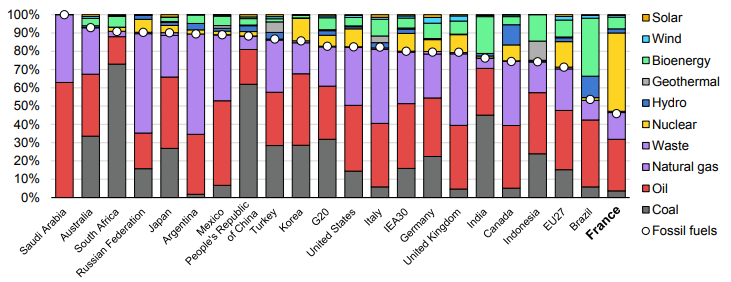

The fuel use data in the Exhibit below is very much a function of geology and the good and bad luck associated with it. The large hydrocarbon users' consumption patterns are a function of what they have – if you have a lot of coal, you use a lot of coal. The significant build-out of nuclear in France is partly because of Frances’ exceptional track record with the technology but also because the country does not have anything else to fall back on. Japan’s nuclear component was much higher before Fukashima. It is, however, worth noting the almost insignificant share of wind and solar anywhere, and then to put this into context with the collective ambitions, not just for 2050, but for the much shorter 2030 targets.

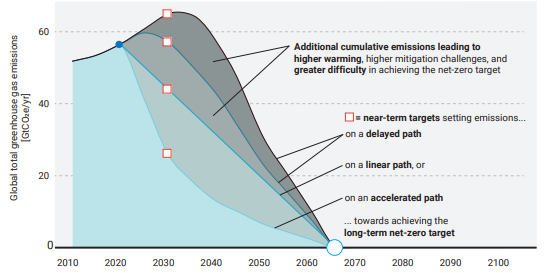

In a media interview earlier this week (more details to follow) we were involved in a discussion about inflation and specifically energy. The discussion covered much more than this, but the chart below is perhaps one of the easier ways of showing where our concern lies, and it ties directly to the behavioral patterns that are emerging concerning climate change and ESG focused investing. As noted in the title of the chart, the likelihood that the linear path from here to net-zero will work is very low, given that we would need global government coordination now, and we are far from it. The other scenarios are much more likely, at least in the early years, and they call for an increase in emissions, which implies growing demand for fossil fuels and other materials that have a high emissions footprint. If you are an oil or gas producer and you look at the chart you could quickly conclude that while your products are in demand today and likely to be in growing demand for several years, the longer-term outlook is very unclear. This might slow down your investment plans, or at least make you think twice about the shorter lead-time projects – such as on-shore and shale-based. However, it could kill any longer-term offshore/deepwater projects that take many years to bring on stream. Today we see energy investment hesitancy everywhere (see our Chemical Blog), but at the same time, we do not see the global coordination to drive a faster energy transition, assuming we had the materials and the investment dollars to move any faster. The risk that we run out of produced fossil fuels from time to time over the next 3-5 years is very high.

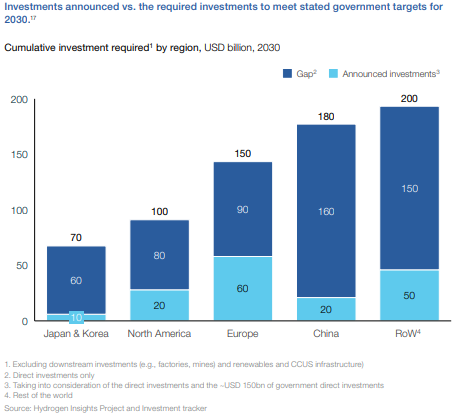

The hydrogen council chart below drags us away from 2050 and back to the more concerning near-term goals of 2030. The chart shows a significant gap in the current planned spend for hydrogen by region and the spending required to move far enough towards 2050 targets. This chart makes assumptions about the share of energy transition that will be met by hydrogen and given that it is the industry producing the chart, it is probably on the high side, but it is inclusive of both blue and green hydrogen. We have serious concerns about these totals being reached in general, but we see the target as completely unreachable without significant blue hydrogen (because of renewable power and electrolyzer capacity limits and we cannot rely on Canada to do all of the “heavy lifting” for blue hydrogen - see company section in today's daily report. The Biden administration may make more progress on emissions if the next order of business was just on CCUS rather than an omnibus bill that included CCUS but which could get held up in negotiations for months if it even gets passed.

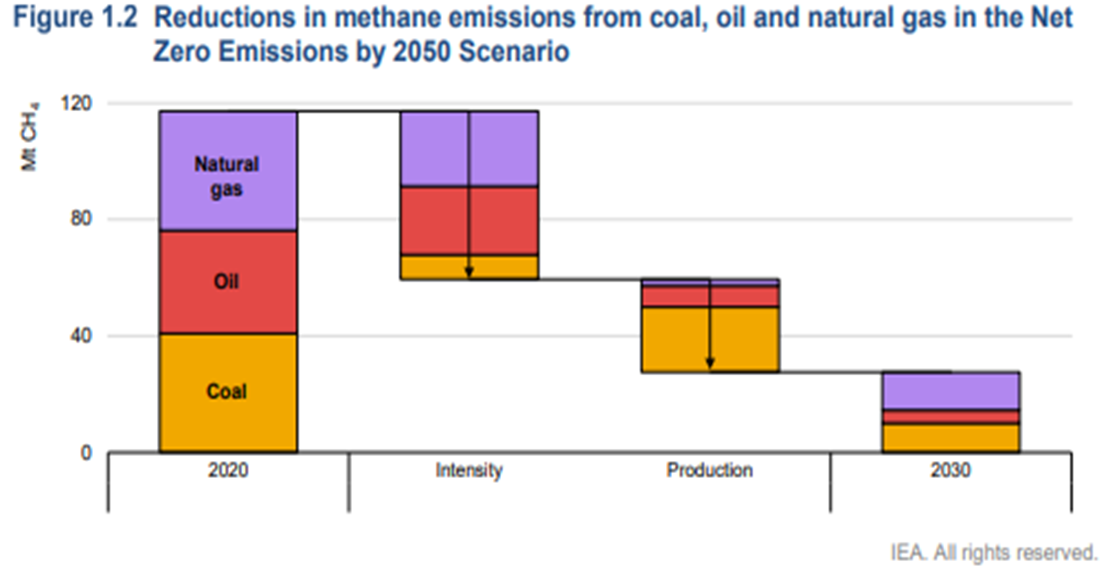

A couple of things worth highlighting in today's daily report – the first being Chevron’s move to join the net-zero club – focusing all eyes now on ExxonMobil in particular but also the rest of the US E&P crowd. Chevron will have some major challenges getting to net-zero and will likely face much of the same skepticism that bp, Shell, and TotalEnergies attracted in Europe initially and still face today. The Europeans have placed a lot of their bets on moving into renewable power – for the moment, Chevron is focused on moving to net zero in its own operations, which we read as biofuels and a lot of CCS. Given the acute shortage of international natural gas, it would make the most sense for the independent natural gas E&P companies and the LNG sellers to jump on the same boat. By promising low carbon natural gas and LNG, the industry is much more likely to gain support for the expansion that the world needs to counter some of the EIA assumptions around coal and petroleum product use from 2030 to 2050. Of course, it would be a whole lot easier for the US industry to do this if they had a value on carbon to work with! The chart below looks at one of the core clean-up issues, which is methane leakage. This is a subject we cover extensively in our ESG and Climate service linked here.

The gaps in the exhibit below are not surprising as 2050 is a long way away and we would not expect all of the needed capacity to be announced or pledged yet, especially as many companies are still weighing alternatives. For example, as an ethylene producer, you have 5 paths – hydrogen as a furnace fuel – electric power as a heating medium – stick with what you have and use CCS – find an alternative route to make the polymers – make alternative polymers.

In our ESG and Climate report yesterday we focused on sustainable aviation fuel, discussing a recent report from Shell and Deloitte, which shows some of the challenges with getting the aerospace industry to net zero. The report focused on the need for sustainable aviation fuel now, and in large volumes, as this is the only thread that the industry can pull on today – synthetic fuels (from CO2 and hydrogen will be uneconomic for decades, and neither electric powered or hydrogen-powered aircraft are going to be a solution before 2050). The bp, Delta, and Boeing linked headline is one of many that we expect to see as the need for near-term progress is urgent, given the scale of investment required. See yesterday’s report for more detail.

The charts below both support our view that we will see continued inflation in renewable energy costs, rather than the deflation that is baked into all of the forward models. It is easy to forget that some of the early solar installations are coming to the end of their useful lives and are retiring – these are gaps that new solar will need to fill. Wind power has the same issue, as many of the original wind farms need equipment replaced and the introduction of recyclable wind turbine blades has been in recent manufacturers' announcements. When we see analysis of who is going to use which tranche of new renewable power for which new hydrogen project we see major gaps in the power demand analysis, in part related to power demand growth at the domestic consumer – because the more rapid introduction of EVs – and in part because or retirement of facilities and the need to replace them.