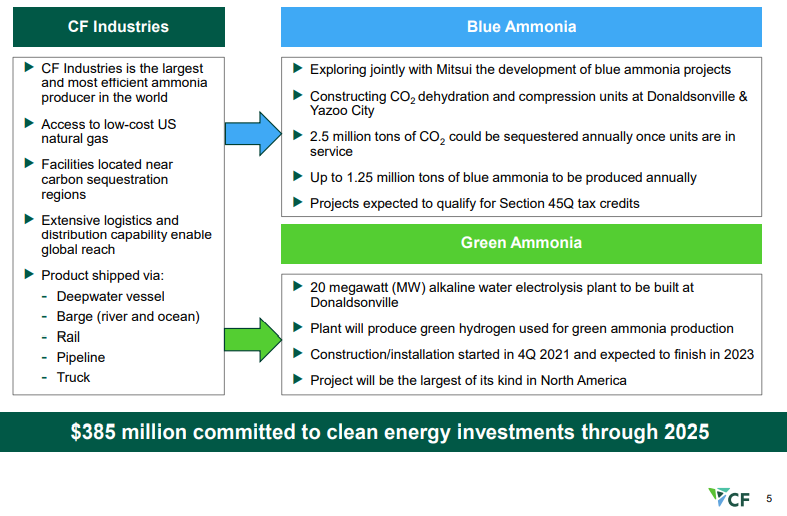

We continue to believe that the US has a cost advantage in CCS versus many of the other regions of the world and that when coupled with low natural gas prices the US should be able to take a lead in developing low carbon chemicals. CF is pushing the idea of both blue ammonia in the US as well as green ammonia, and while the company has yet to announce sequestration plans for the CO2 it is working to purify – see Exhibit - once dehydrated and compressed the incremental cost of storage should be low.

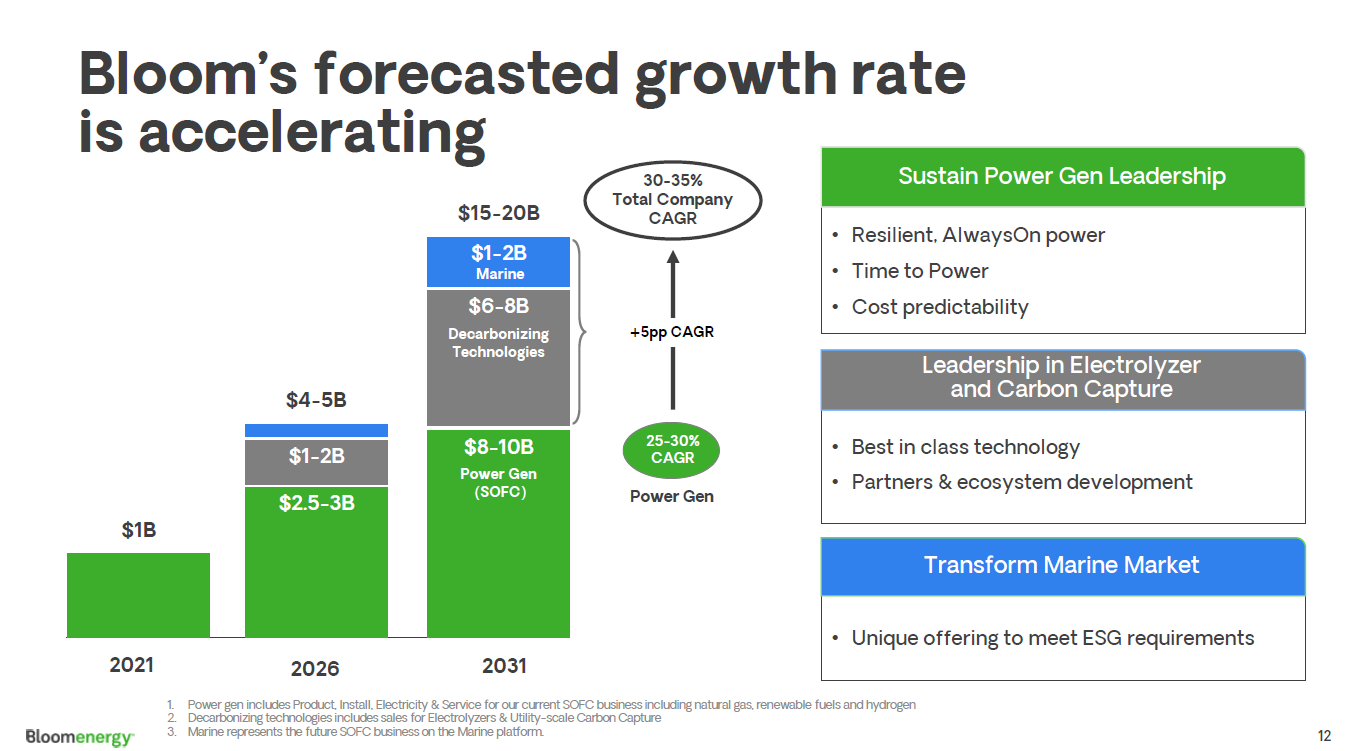

There is a lot in the ESG section of today's daily report and we will elaborate more in our ESG and Climate report next week (to be found here). The Bloom Energy results were strong and the modular nature of what Bloom is offering, in our view, should only increase the level of interest going forward. SMR and ATR base blue hydrogen projects are very large, requiring billions of dollars of capital and taking years to construct. The projects are further complicated by the likely need to build dedicated CCS with each unit. The methane fuel cells that Bloom offers are modular and can be much smaller and more incremental from an investment perspective. For blue hydrogen, they will still need CCS, but they offer a lower capital-based route to hydrogen and power today. We can see an opportunity to deploy these units, or something similar, everywhere there is CCS, as either an incremental source of hydrogen and power or a large source. Bloom still has work to do on lowering costs, but much less work than green hydrogen appears to have today, in our view.

The linked Covestro headline from today's ESG & Climate report is a reminder that the chemicals and polymer makers are dealing with more than just recycling and product lifecycle management. Customers are equally focused on the carbon footprint of the products they buy and the green hydrogen move by Covestro (assuming that affordable green hydrogen is possible) would replace hydrogen made from fossil fuels and replace other fuels for heat in some cases. Germany has some considerable issues with decarbonizing, as the blue hydrogen route will be challenging in a country that will likely not allow onshore CCS. Covestro and others may have little choice but to buy green hydrogen and/or green power, even if supplies come up short of plan and costs are higher as a result. This is a good illustration of why we believe that the right policies in the US could drive some additional competitive edge while meeting climate objectives. Cheap hydrocarbons coupled with cheap CCS may only be matched in some parts of the Middle East.

The linked Siemens Gamesa news could not have been a more clear example of one of our key research themes of the last year – backlog up, suggesting strong demand for new wind power capacity – deliveries and profits down because of material shortages – price inflation and logistic issues. While the company is getting squeezed because of higher costs on contracts that have limited opportunity to pass through the cost, at the same time slide 8 of the earnings release deck shows that selling prices rose in fiscal 1Q 2022. This breaks a declining trend in pricing and one of the core assumptions behind many energy transition plans – that renewable power prices can keep falling. Onshore wind orders are falling, but offshore orders are rising – and these come with higher costs and the need for more materials as we showed in a chart in yesterday’s daily. The added costs burden of more offshore wind projects may only serve to tighten markets for materials further, leading to further increases in installed costs.

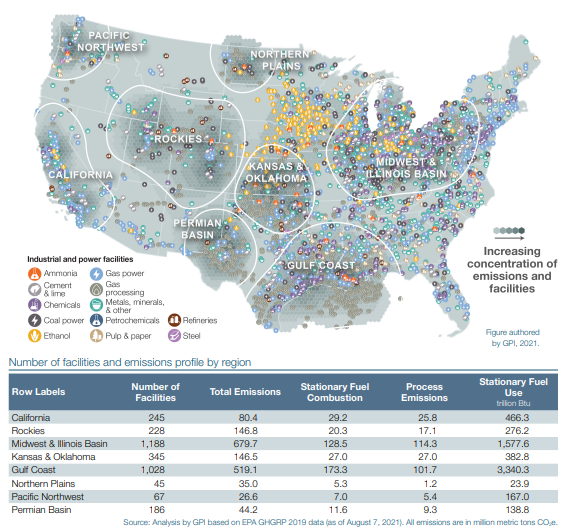

The Green Plains Institute analysis below draws heavily on the EPA emissions data by facility, but correctly, in our view, identifies where CCS makes the most sense in the US. We still struggle with the pipeline distances associated with some of these ideas as CO2 disposal is still a cost for emitters and in any attempt to reduce costs, pipeline distances will be key. We have discussed the opportunity recently for massive blue hydrogen investment (including CCS) to replace industrial heating fuel and this would apply in all of the regions below. Note our conclusions in today’s ESG and Climate report that we expect renewable power installation goals to fall short – requiring more use of natural gas (for power generation or hydrogen production) with accompanying CCS.

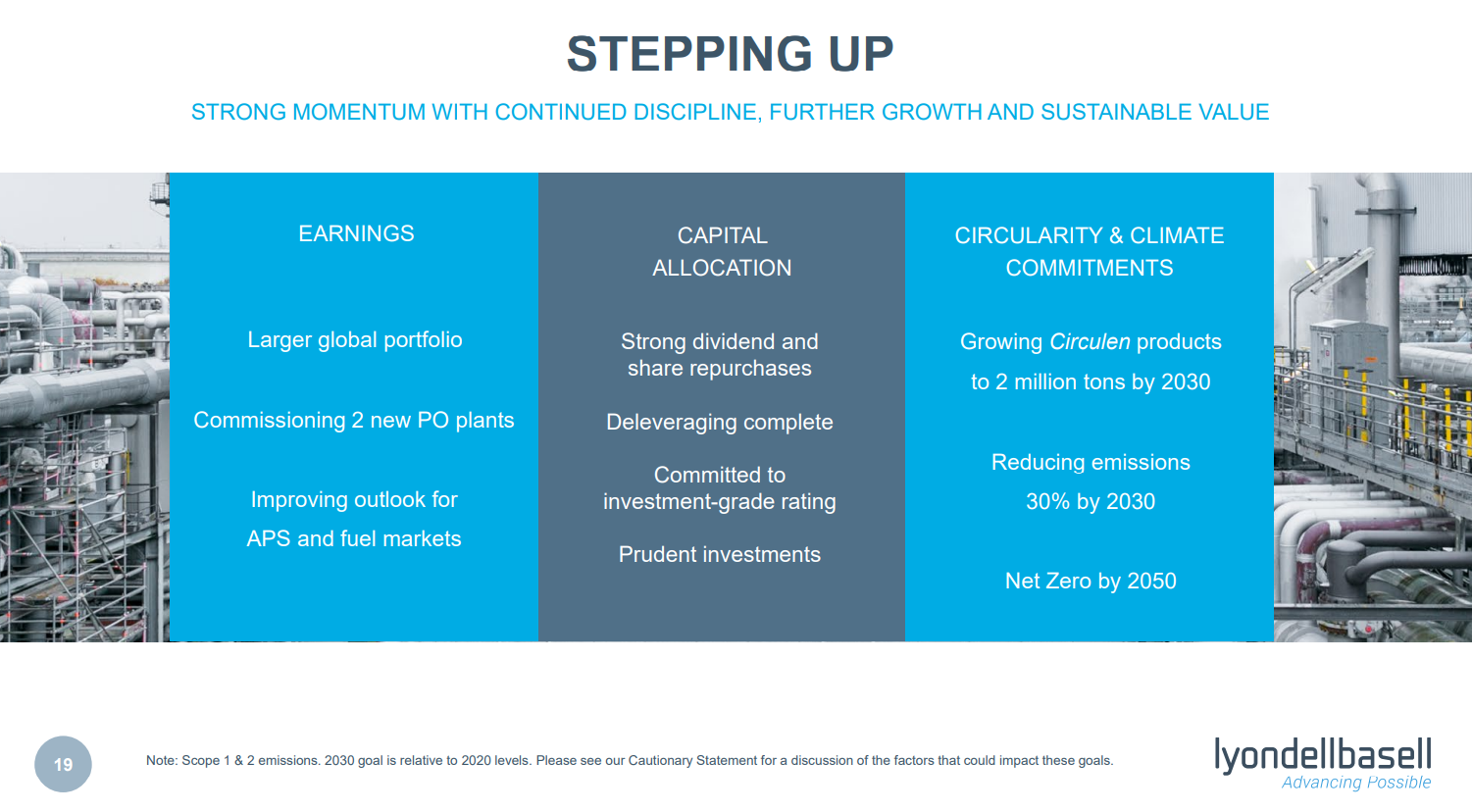

2022 is the year in which the rubber will need to meet the road for many of the chemical and other material and industrial companies who have made 2030 emission pledges. In the Dow release yesterday, the company used the call as an opportunity to remind investors about the Canada investment and tie that into the 2030 emission goals. We note LyondellBasell’s 30% emission reduction goal by 2030 and like others, LyondellBasell will not be able to get there without substantial investment. LyondellBasell and others do not necessarily have to spend in 2022 (neither does Dow), but unless there are some concrete plans by the end of the year stakeholders will likely start to question whether the emission goals are real. We suspect that most companies are trying to work out whether investments in hydrogen (likely blue hydrogen because of the volumes needed) are a better solution than trying to capture CO2 from a natural gas furnace. Any large hydrogen investment with associated CCS will take 5-6 years from concept to production. Like Dow, we would expect others to focus emission-reduction investments in countries/states that have a clear value on CO2. See today's daily report for more.

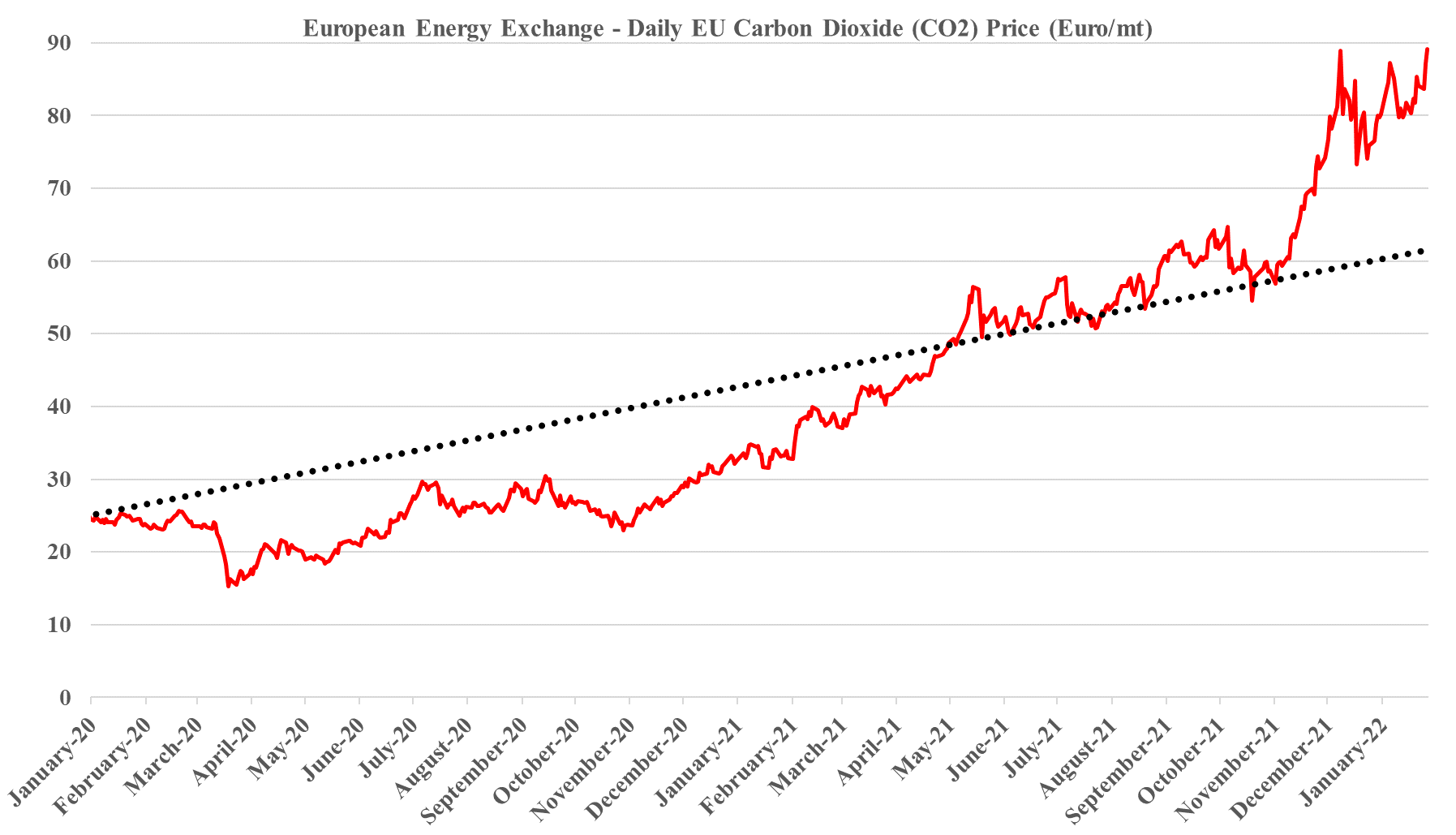

The linked Canada headline supports one of the themes that we have been highlighting for a while, which is that certainty around carbon pricing is likely to drive investment rather than discourage it. Canada, and specifically Alberta, has seen several new investments announced over the last few months because manufacturers can now add some certainty around carbon values to other advantages offered by the province, including cheap natural gas and what appears to be low-cost CCS opportunities. We are also seeing investments shape up in Europe – also to produce low carbon materials and fuels – and this is also driven by greater certainty around carbon value. The lack of a carbon price in the US is becoming a competitive disadvantage for the country and those opposing it in government are, in our view, very misguided. If China can develop a credible and broad carbon pricing mechanism, it will also likely gain investment dollars, possibly at the expense of the US. Not having a sound climate change and carbon value framework in the US is a major threat to many of the reshoring initiatives that US retailers and manufacturers would like to see.

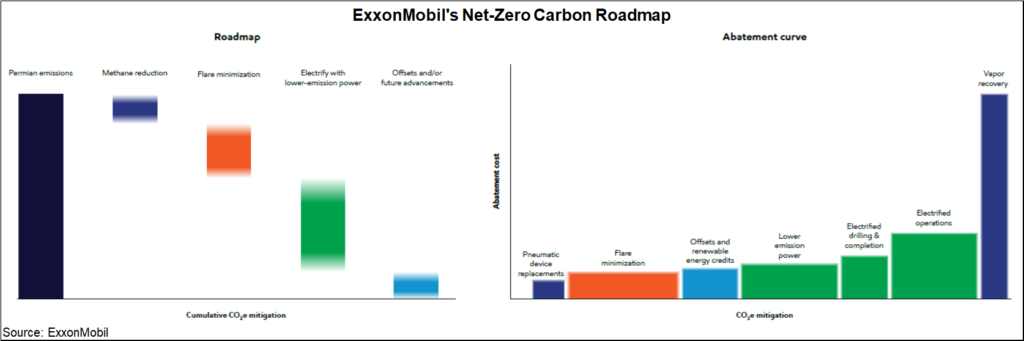

One piece of big news early this week was ExxonMobil’s announcement that it is developing plans that will drive net-zero emissions by 2050 and the company shared a detailed overview. We have picked some charts from the report, some of which can help us draw conclusions for ExxonMobil, but others are more general. The company is banking on a lot of emission reduction and CCS to get to the 2030 target and a large part of the goal is likely to come from the plans for the Permian and the previously stated net-zero target that the company has for 2030 – detail on how this will be achieved is shown in the Exhibit below, see more in today's ESG report.

In yesterday's ESG and Climate report, we looked at an extreme example of how the right support for clean fossil fuel use through a long period of energy transition, could create economic growth, support job growth, and not require subsidies – coal gasification to produce low-cost hydrogen. With the opposition to the “Build Back Better” bill, there is a clear opportunity for the fossil fuel industry to step up and suggest compromises, and we are seeing increasing interest in large scale CCS, despite its cost, in part because it is a path that will allow natural gas and other fossil fuels to meet increasing demand in a way that has a much lower carbon footprint, and in part, because it will still be cheaper than some of the heavily subsidized ideas to try and accelerate investments in renewable power that will inevitably fall foul of equipment and material shortages – something we have written about at length in past research – linked here. The EIA has already noted that coal use in 2021 has risen globally and it is likely that it will rise again, given the increasing demand for electric power and the lack of supply elasticity in the renewable power and natural gas-based systems – coal is a large part of the swing capacity these days. Many of the CCS projects proposed for the US are not much more than proposals today, but we are seeing some initial investment to prove that subsurface storage opportunities are feasible.

As we have mentioned before, we see a couple of major challenges with the CO2 pipelines proposed for the mid-West, one of which is summarized in the Exhibit below. The first issue is pipeline right-of-ways, as there are already activists determined to oppose the pipelines, and opposition to pipelines has been a core them of the last 10 years. The second issue is cost. Carbon abatement is a cost for all looking for solutions and even where incentives exist, such as the 45Q program or the LCFS fuels program, the challenge will still be creating a path with the lowest. Compression and pumping costs are high for CO2, especially if the pipeline wants a pressure that will allow for direct injection into a series of wells. Lower pressure transportation by pipe is inefficient and raises the capital cost of the pipeline – so it becomes a trade-off – CAPEX vs OPEX. $4.5 billion of investment – as suggested by Summit – is $375 per annual ton of carbon dioxide sequestered - $37per ton assuming 10-year straight-line payback – twice that if you want a 10% return. This is before a dollar of OPEX and pipeline costs could easily exceed another $30+ per ton, with separation and purification of the CO2 stream also not free. Unless the ethanol producers are paying Summit and Navigator to take the CO2, the math becomes very challenging. See today's daily report and our weekly ESG and Climate report for more.