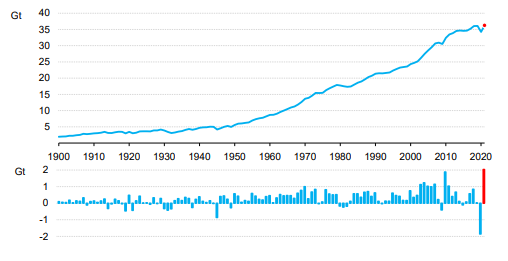

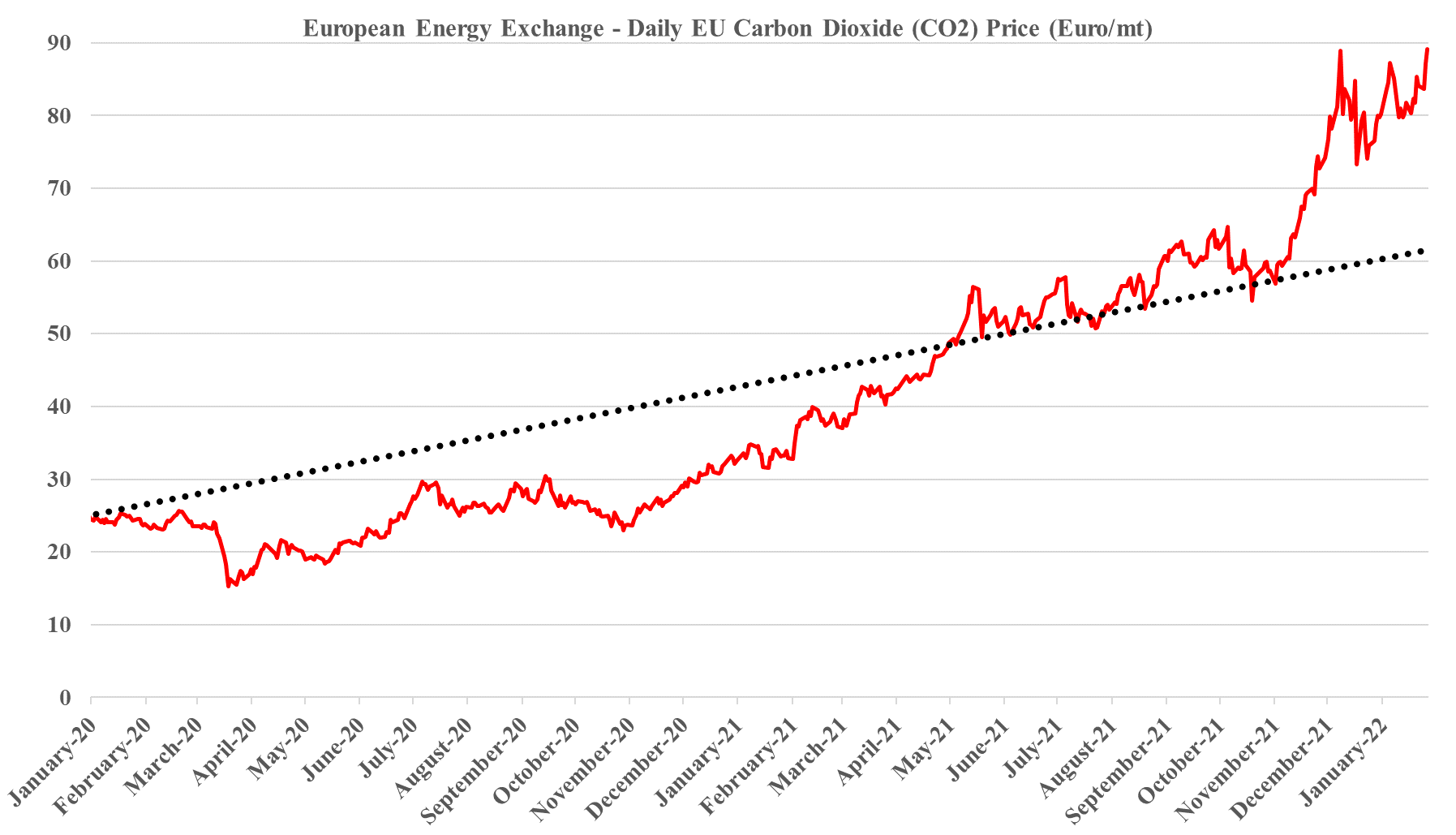

The IEA CO2 emissions data is not a surprise as it has been telegraphed for a while by several commentators that the world went backward in 2021. There were several causes, not least of which was an economy which, with the benefit of hindsight, was overstimulated, pushing up demand for resources in general, including energy. There has also been an overestimation of the rate of investment in renewable power, something which is finally gaining attention more generally, triggered by the energy supply fears that have emerged from the Russia/Ukraine conflict. It will take time to make the very large investments needed to abate the CO2 associated with industrial and consumer activity and there is no overnight fix. Accommodative policies are needed today for investments that will start a decline in emissions several years from now.

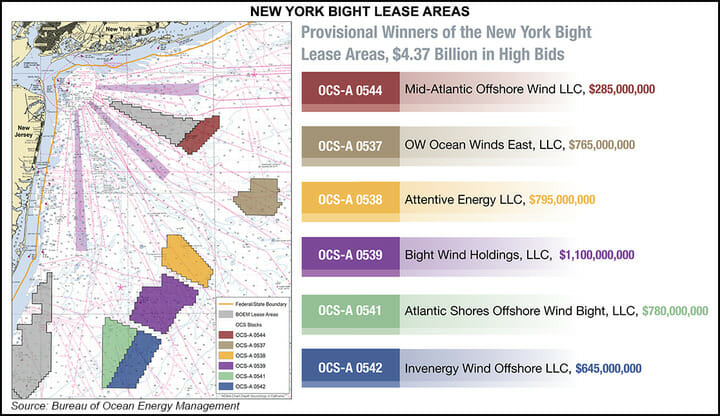

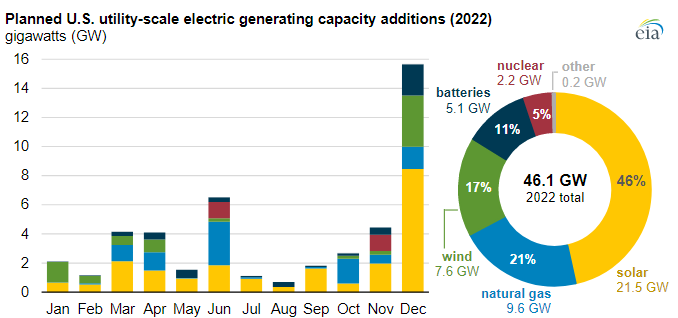

We include a couple of headlines and charts in today's daily report that step into the central theme of this week’s ESG and climate report, which will be published tomorrow (see here). The offshore wind ambitions and the EIA solar and battery projections both assume that the materials are available to build the capacity. In the case of the offshore wind leases, the winning bidders do not need to be in the market for all of the projects today and while the opportunities will lead to a step-change in demand for turbines in the US, the timing is less clear today that it will be in a few months and that timing may be adjusted to reflects equipment timing and costs, etc.

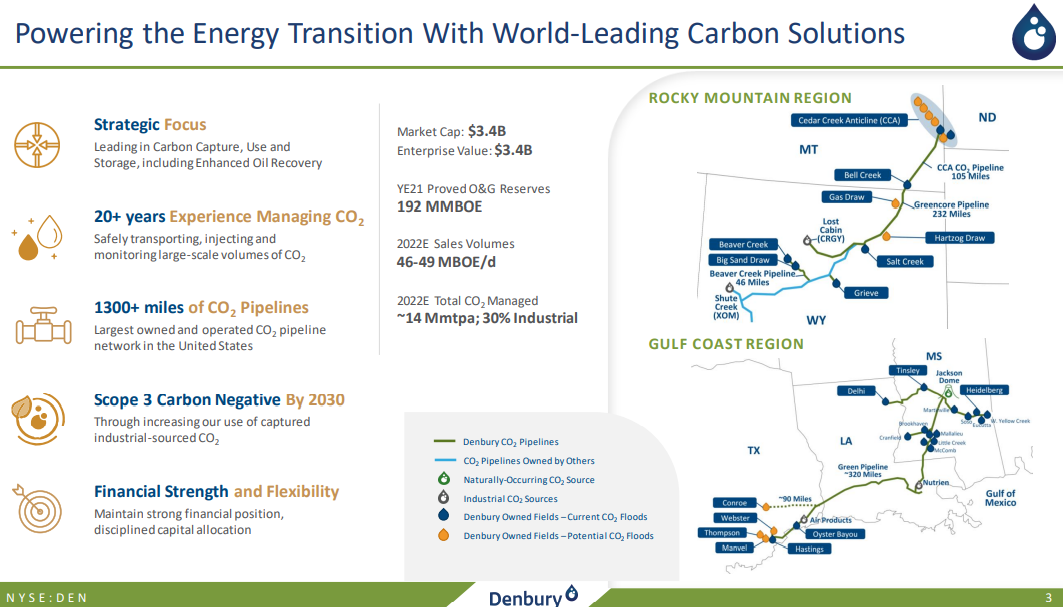

The Denbury release is a great example of something that we discussed in our ESG and Climate piece yesterday. The company is putting stakes in the ground concerning carbon capture and storage but is only really spending on its EOR opportunities, which of course look really interesting today. While the 45Q credit for EOR helps, the main driver is the incremental crude oil volumes that you can pull out of the ground because of the CO2 injection – the higher the price of crude oil the greater the value of EOR. Regardless of the tax credit, the economics of EOR should look very good today and it is not surprising to see several initiatives from Denbury given that it has a lot of existing infrastructure for CO2. The CCS plans are no different than some of the projects we discussed yesterday – they are stakes in the ground – marking territory – but unlikely to move forward without higher incentives. One of the core topics of our report yesterday is whether the conflict in central Europe will turn attention away from energy transition and energy security for tomorrow, because of the acute distraction of both energy and national security today.

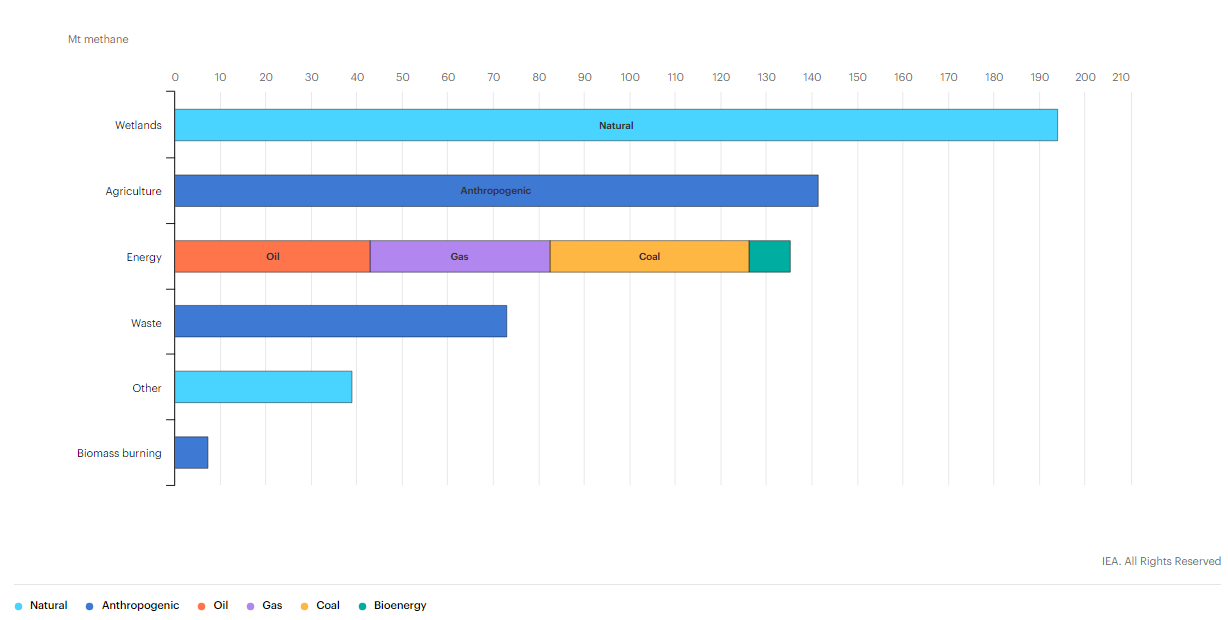

We have noted several renewable natural gas initiatives in the US and the data in the chart below shows how much methane is emitted by agriculture – the largest source after natural leakage. The agriculture-based RNG projects only make economic sense today where you have access to very large farms, where customers are willing to pay a premium, or where you qualify for incentives. That said we expect more projects, with growth stories at companies like Archaea Energy dependent on building new projects. The chart also shows how much emissions flow from the energy industry and this has been a more acute focus for remediation since COP26. See more in today's ESG and Climate report.

We view the hydrogen tax credit discussed in today's daily report as potentially very harmful, as it could give life to projects that will further increase demand on a renewable energy industry that has finite limits to its rate of growth. The credit could encourage inherently uneconomic projects – even with a longer-term “abundant power” view. If the incentives are used to back clean rather than green projects it would make more sense as blue hydrogen could be produced in very large quantities without breaking the bank and would allow constrained renewable power investments to focus on other harder to decarbonize power needs. If the hydrogen subsidy could be added to the 45Q sequestration credit we would likely see a wave of blue hydrogen investments in the US – primarily aimed at decarbonizing industrial applications and refining.

The linked Canada headline supports one of the themes that we have been highlighting for a while, which is that certainty around carbon pricing is likely to drive investment rather than discourage it. Canada, and specifically Alberta, has seen several new investments announced over the last few months because manufacturers can now add some certainty around carbon values to other advantages offered by the province, including cheap natural gas and what appears to be low-cost CCS opportunities. We are also seeing investments shape up in Europe – also to produce low carbon materials and fuels – and this is also driven by greater certainty around carbon value. The lack of a carbon price in the US is becoming a competitive disadvantage for the country and those opposing it in government are, in our view, very misguided. If China can develop a credible and broad carbon pricing mechanism, it will also likely gain investment dollars, possibly at the expense of the US. Not having a sound climate change and carbon value framework in the US is a major threat to many of the reshoring initiatives that US retailers and manufacturers would like to see.

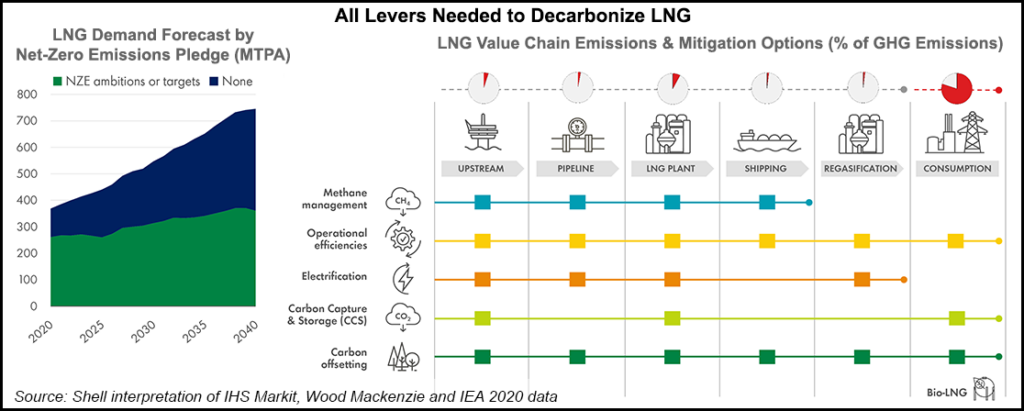

The first chart below has been included in a similar form in prior work and is a good summary of what is needed to decarbonize the LNG market to the greatest degree possible. There is a lot of resistance to the idea of endorsing natural gas as a transition fuel, but so many developed and developing countries need natural gas – often in the form of LNG – to displace or avoid (additional) coal use. If the LNG industry does not start to pursue the paths suggested in the exhibit, and reasonably quickly, it will stand very little chance of winning, or perhaps surviving, a PR battle that is very much stacked against it.

First, it is going to be an uphill struggle to get some common sense around the continued use of fossil fuels during any period of energy transition if the activists take away all resources from the energy industry – banking, PR, etc. While there is plenty of work to be done to minimize greenwashing, there is also plenty of work that needs to be done to explain why fossil fuels are still needed and how we can use them as cleanly as possible. If it becomes a business risk to bank or advise any company in the fossil fuel industry, while there will inevitably be workarounds, the net effect will be continued underinvestment, in production and in cleaning up the fuels and the concerns that we raised for natural gas in our Sunday Thematic will happen.

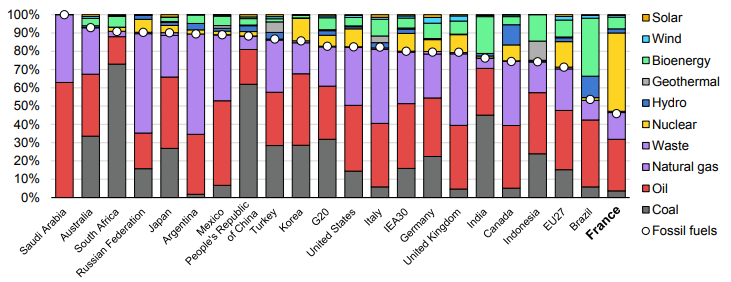

The fuel use data in the Exhibit below is very much a function of geology and the good and bad luck associated with it. The large hydrocarbon users' consumption patterns are a function of what they have – if you have a lot of coal, you use a lot of coal. The significant build-out of nuclear in France is partly because of Frances’ exceptional track record with the technology but also because the country does not have anything else to fall back on. Japan’s nuclear component was much higher before Fukashima. It is, however, worth noting the almost insignificant share of wind and solar anywhere, and then to put this into context with the collective ambitions, not just for 2050, but for the much shorter 2030 targets.

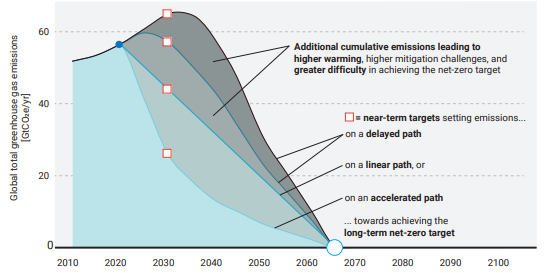

In a media interview earlier this week (more details to follow) we were involved in a discussion about inflation and specifically energy. The discussion covered much more than this, but the chart below is perhaps one of the easier ways of showing where our concern lies, and it ties directly to the behavioral patterns that are emerging concerning climate change and ESG focused investing. As noted in the title of the chart, the likelihood that the linear path from here to net-zero will work is very low, given that we would need global government coordination now, and we are far from it. The other scenarios are much more likely, at least in the early years, and they call for an increase in emissions, which implies growing demand for fossil fuels and other materials that have a high emissions footprint. If you are an oil or gas producer and you look at the chart you could quickly conclude that while your products are in demand today and likely to be in growing demand for several years, the longer-term outlook is very unclear. This might slow down your investment plans, or at least make you think twice about the shorter lead-time projects – such as on-shore and shale-based. However, it could kill any longer-term offshore/deepwater projects that take many years to bring on stream. Today we see energy investment hesitancy everywhere (see our Chemical Blog), but at the same time, we do not see the global coordination to drive a faster energy transition, assuming we had the materials and the investment dollars to move any faster. The risk that we run out of produced fossil fuels from time to time over the next 3-5 years is very high.