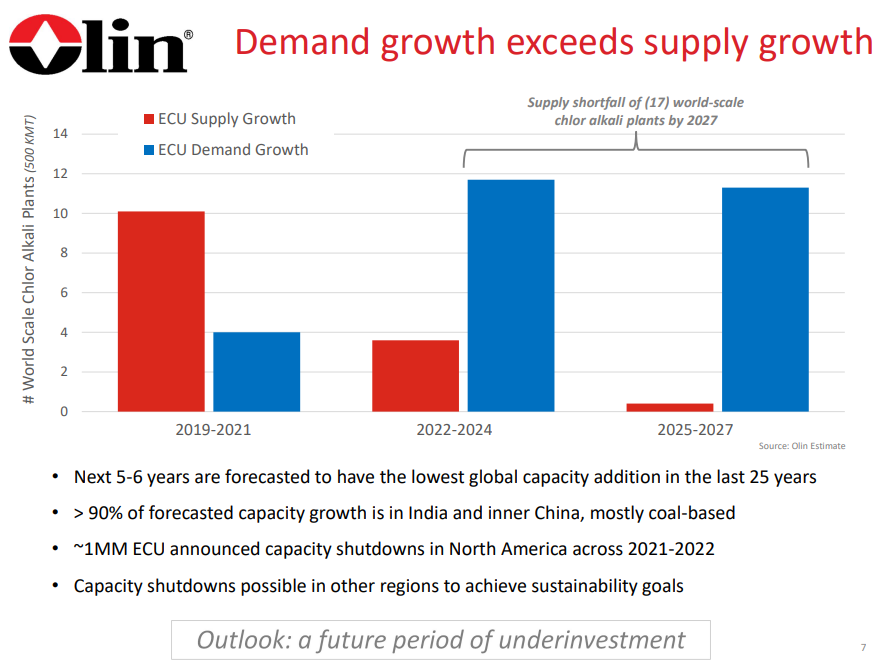

We are already seeing the impact of ESG-pressure related underinvestment in many commodities, and the picture that Olin paints around chlor-alkali is not dissimilar to some of the analyses that could be done around some metals today – especially those that are critically important to the EV, Solar, and Wind industries – this is a topic that we have covered at length. While chlor-alkali may be a pressing very near-term example of how underinvestment could impact chemicals, we suspect that the issue may be much broader, just not yet apparent in other sectors because of the wave of new investment from 2017 through 2022. The polyethylene equivalent chart to the one below would show more balanced supply/demand in the 22 – 24 period than for chlor-alkali but the same deficit thereafter. Many of the other base chemicals would look the same. This supports our expectation of an industry mega-cycle, possibly starting as early as 2023. Of course, there is time to add new capacity by 2025/26, but most companies are more focused today on how they comply with tighter environmental standards today than they are on their next expansion. Further hindering new expansion-driven capital investment decisions is the uncertainty around polymer demand (how much will be recycled, will there be more bans, will there be a substitution from other materials). Our view is that base polymer demand will continue to grow and that we will run short as a consequence of underinvestment. See our report titled - Waiting For The Big One – Is A Chemical Mega-Cycle Ahead?