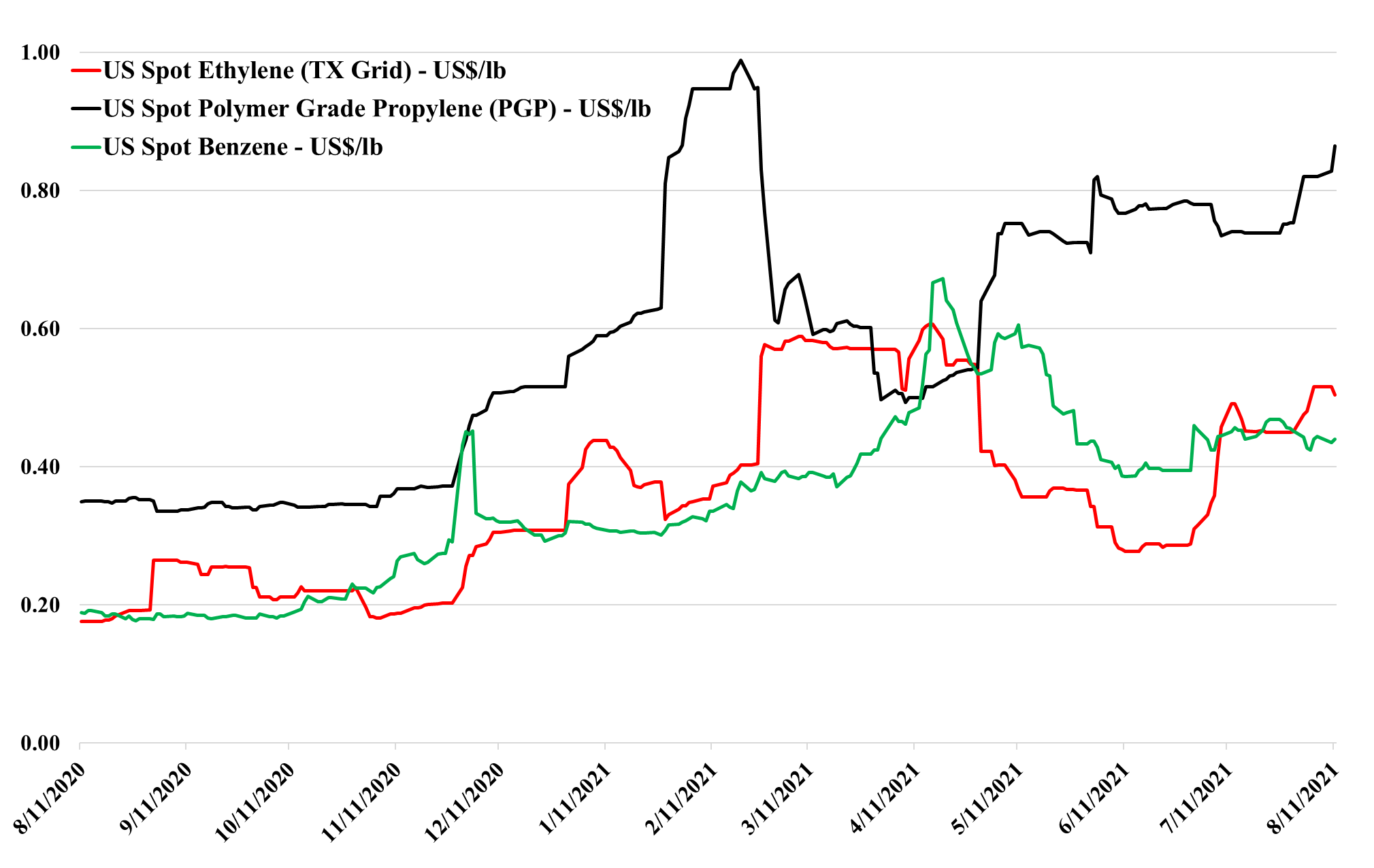

US benzene prices reflect both the net short market in the US but also the alternative value of reformate as a gasoline feed. While benzene is very limited in terms of how much can be left in fuel streams, its refinery-based feedstock, reformate, is a key component in gasoline – albeit low octane – prior to reforming and even during reforming the benzene conversion can be limited if the gasoline value is higher and volumes are constrained. In the US, as well as in many other parts of the world, we are facing gasoline shortages and today more than 13 US states have gasoline prices above $5 per gallon. While that may be shocking to Americans, the car ride from Heathrow yesterday was in a very popular make in the US that currently costs more than $200 to fill up in the UK! So benzene is getting squeezed – its feedstocks are more expensive and some of the alternatives to making benzene currently offer better netbacks. While we see all polymer costs rising in the US and elsewhere, this US benzene surge is not good for US polystyrene producers at a time when the industry is trying to justify polystyrene’s existence in a “circular” world, and it is also inflationary for the epoxy businesses, and other consumers of both styrene and phenol.

In our Sunday Thematic to be published this weekend we are focused on business lines that will still look good in an economic turndown versus those that are more vulnerable, and ASIX may find itself spread across both buckets. The momentum in agriculture is very strong and even with a quick resolution in Ukraine, we could see high prices for crops and farm inputs for years as it will take a long time to correct recent imbalances and the Ag markets were already tightening before Russia invaded Ukraine. This and natural gas shortages (see today's daily report) should keep upward pressure on ammonia and ammonia derivatives pricing. On the other hand, any slowdown in consumer durable/discretionary spending will likely negatively impact nylon. A faster resolution in Ukraine would likely be negative for the Ag names as even if it takes a while to correct crop and fuel imbalances, the stock market will likely look through that and start focusing on eventual more normalized markets.

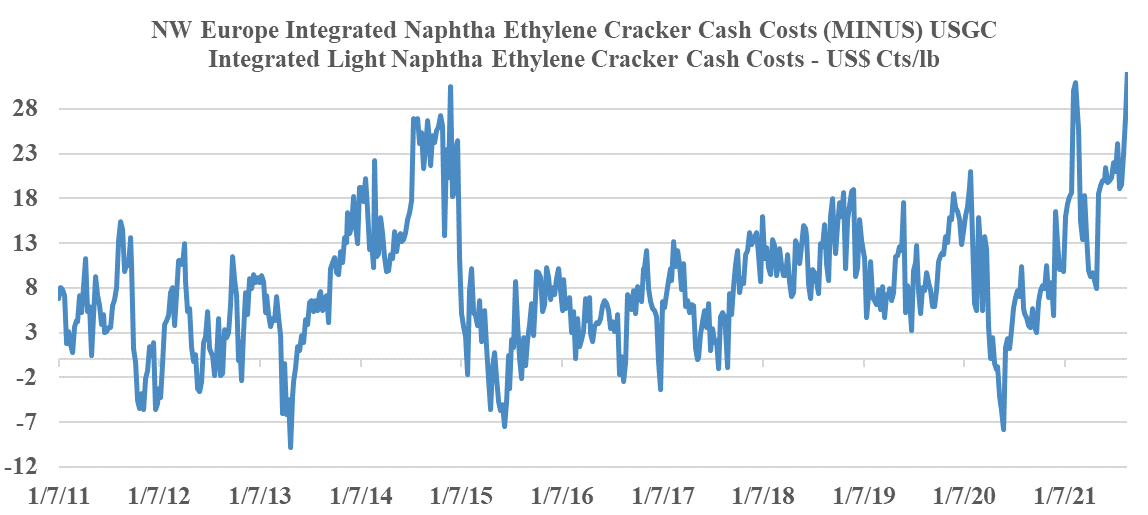

With the rapid jump in international natural gas and oil prices, we would see very concerted efforts to raise basic chemicals and polymer prices in Europe and Asia and will have a positive knock-on effect for the US. In our weekly catalyst report on Monday, we showed that ethylene producers outside the US were all losing money, especially in Europe and Asia. Some European demand will already be lower, because of curtailed product exports to Russia and Ukraine, but producers will want to cover costs at a very minimum and consequently, will be trying to match price increases with cost increases and if possible do a bit better than that. All of this will create a greater margin umbrella for the US, and US exporters selling directly into international markets will see export margins step up and may see incremental opportunities to export more, assuming that the freight rates are not too onerous for incremental containers.

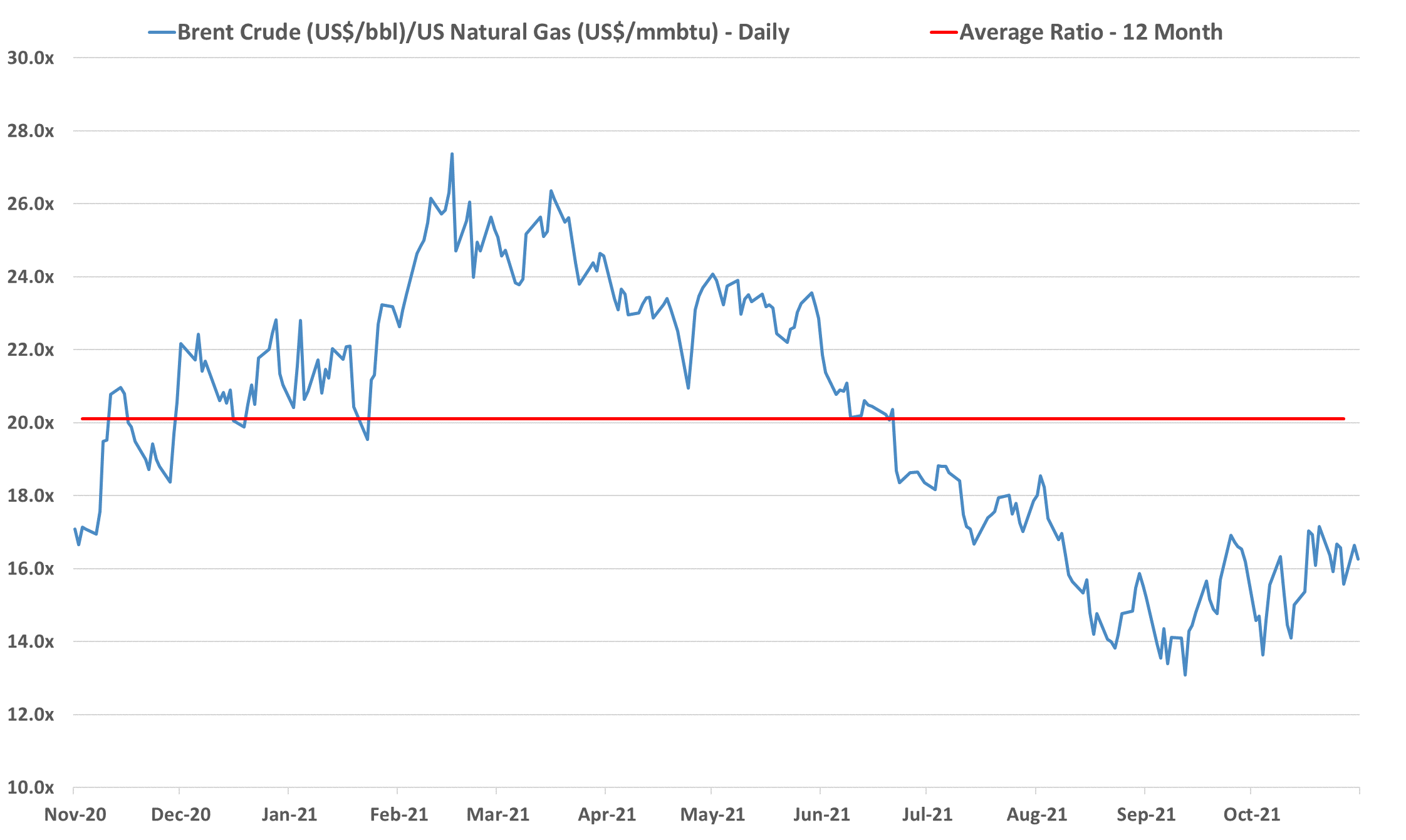

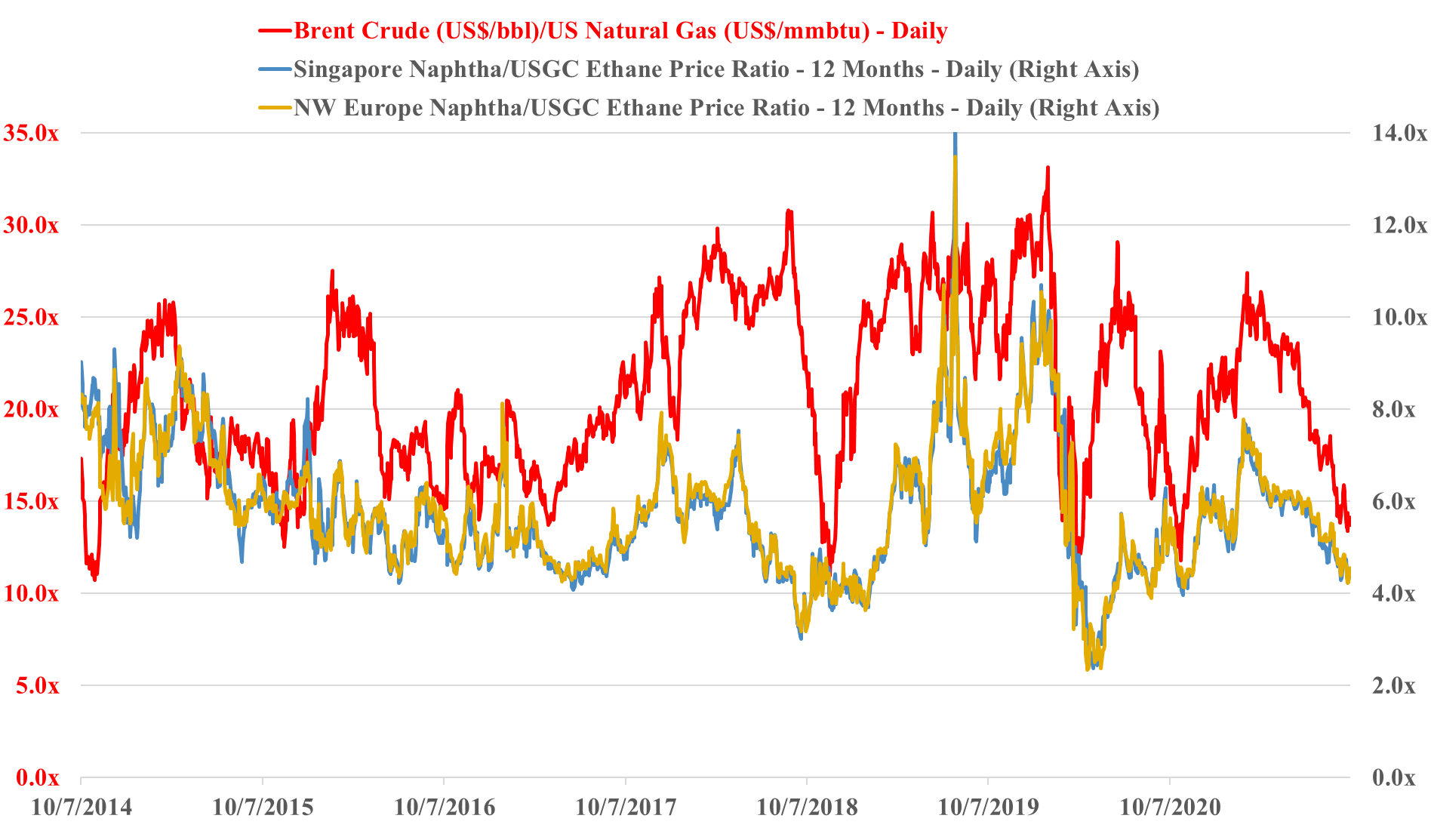

We remain concerned that natural gas E&P investment in the US remains too low to meet expected demand increases, especially for natural gas-fired power stations and LNG, but also possibly for NGLs, especially ethane, given new ethylene capacity and a fresh export market in Mexico. Near-term, natural gas prices are showing some easing relative to crude, albeit a very volatile trend – Exhibit below – but we see medium and longer-term shortages unless E&P spending increases. The new power facilities shown in the bottom Exhibit will all need incremental natural gas, and the international LNG market is so tight that as new capacity comes online in the US we would expect it to run as hard as is possible. This sets up for a market where the clearing price of natural gas in the US is at risk of being set by the marginal exporter. The price jump for domestic consumers would be dramatic and it would cause all sorts of headaches in Washington and probably intervention. We showed the incremental natural gas price in the Netherlands in our Daily Report on November 18th, and if the US price were to reflect the netback from this level, they would rise close to $30 per MMBTU. The natural gas industry needs some sort of global blessing to continue to operate as what will likely be the core transition fuel. It will be necessary to clean up the emissions footprint of natural gas, but the industry should be encouraged to invest on this basis. For those who doubt whether the US natural gas price can rise to $30/MMBTU – note that the Europeans did not think $30 was possible either.

The linked article looks at the chemical inflationary cycle of the 70s, which has some relevant indicators for what we are seeing today, but there were also some stark differences. Rising raw material prices is a common theme and while it is convenient to blame OPEC+ this time, the group is not nearly as much to blame today as it was in the 70s. Consumers were facing not just higher oil prices, but also genuine shortages because of the OPEC cutbacks and the multi-year lead times that it took non-OPEC producers to ramp up E&P and ultimately production. This time the oil is there and relatively easy to get to, especially in the US, but the capital spending decisions of the US oil producers – mostly because of ESG related pressure – are holding back the production.

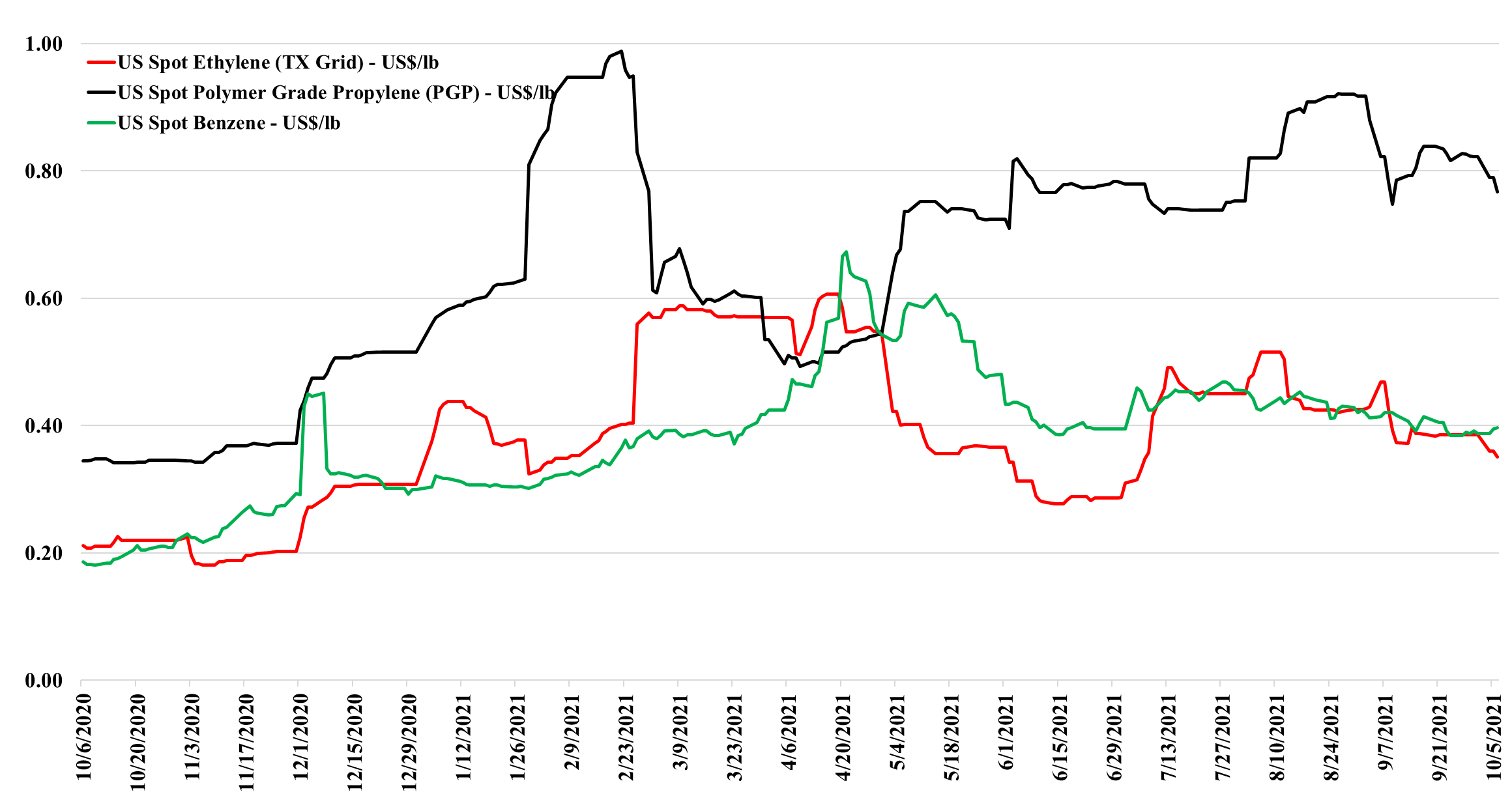

The decline in propylene and ethylene values is worth consideration today as it provides proof, along with the feedstock comments in today's daily report, that US commodity chemical producers are on average facing margin pressure WoW. We noted in yesterday's research that China prices were rising amid production cuts, but demand remains a notable concern. As production rises from current levels in 1H22, this will put downward pressure on Asia chemical prices and also translate into lower US export values.

The US petrochemical production cost competitive advantage reflects a sharp decline at the feedstock level. Natural gas and natural gas liquids prices have risen faster than crude oil and Ex-US naphtha values since mid-1H21. In yesterday's report we identified the disconnect between propane and ethane pricing in the US. While both are high, propane is so high that it is now unprofitable to make ethylene from propane instead of just less profitable. The direction of the lines in the exhibit below shows the changing landscape clearly, and the only reason why the US chemical industry is so much more profitable than the markets in Asia is that chemical product prices are so robust, in part because of the high cost of freight between the regions.

It will be interesting to see how US propane prices track this winter as we have low inventories in the US and there will likely be a step up in year-on-year export demand because of investments in Asia to consume imported propane. At some prices level, there will be demand destruction as ethylene and propylene economics are close to break-even in Asia and the region looks over-supplied enough for some producers to consider cutting back or even shutting down – if propane is the least attractive feedstock then the propane-based units will close first. Those producers in the US that have propane flexibility are unlikely to be anywhere near the market today as declining propylene prices in the US only make the feedstock less attractive. We wonder whether some of the traditional propane users in the US Gulf are experimenting with light naphtha/condensate as an alternative, but these feedstocks will also become less attractive as propylene prices fall. See more in today's daily report.

Before the wave on new ethylene capacity came online in the US there were several low-cost expansion projects all of which added the ability to crack ethane and some of which brought constraints around feedstock flexibility. Consequently, it is less clear than it used to be just how much US ethylene capacity can flex to exploit the very attractive light naphtha economics today. Very conservatively, we would estimate that 5-6 million tons of capacity can flex easily and about the same again with some planning and some logistic adjustments. Among the public companies, both Dow and LyondellBasell are well placed, and likely have at least 1 million tons each of flexible capacity – in both cases, there is a need for propylene and LyondellBasell has significant butadiene/C4s capacity. For context, at current prices, both companies are likely looking at an additional ethylene margin benefit in the US of $2.5-3.0 million per week for as long as this opportunity exists. This would be 0.3 cents per share per week for Dow and 0.7 cents per share per week for LyondellBasell – a rounding error in current earning but more free cash regardless. The chart below shows the unprecedented benefit in the US and see our daily report for more.

To put some perspective around the shipping container costs shown in Exhibit 1 of our daily report today, $20,000 per container equates to roughly 34 cents per pound of cargo assuming that the container is filled to maximum weight. If we also add in loading inefficiencies and assume 500 miles of road transport in the US or Europe, we can add another 5-10 cents per pound. Using ethylene costs in Asia at roughly 43 cents per pound as a basic benchmark (see our most recent weekly catalyst report), we thus estimate that it would cost around 90 cents per pound to get Asia polyethylene into the US. This does not include any working capital cost assumptions around ownership of the cargo from point of production to point of use. US spot PE prices are currently below 80 cents per pound for the more commodity grades of polyethylene, which is the market that could most easily be targeted by imports from Asia. When container rates were closer to $3000 per unit, the all-in import costs would have been roughly 30 cents per pound lower and the arbitrage would have been worth exploring. Of course, if the freight rate was only $3000 per container US polymer prices would likely be lower.