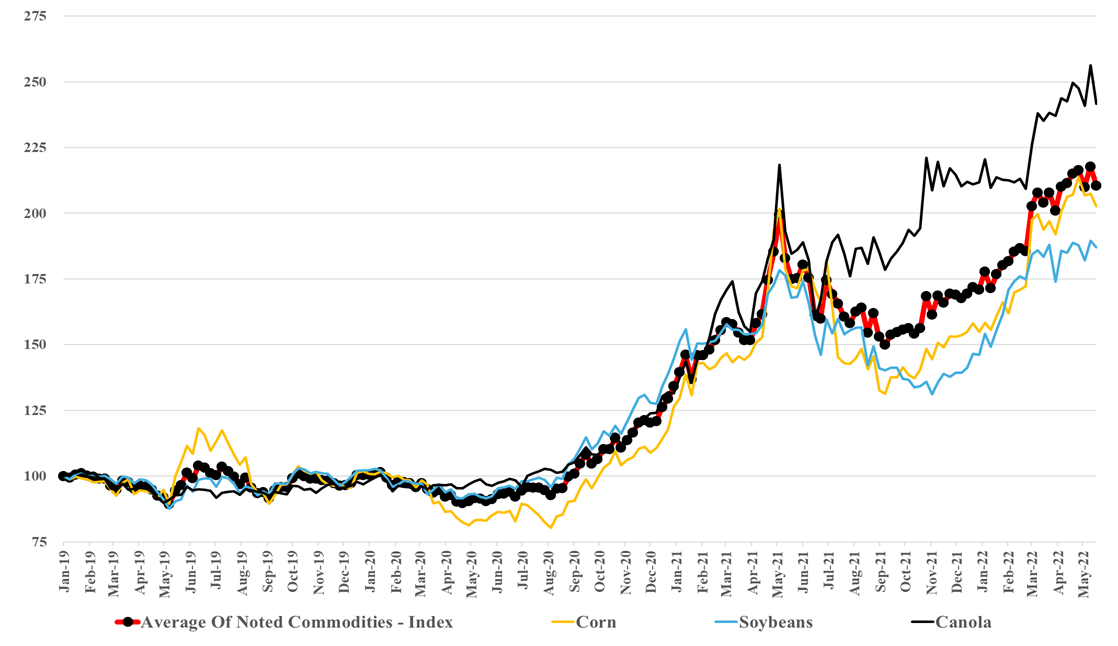

We have focused on agriculture this week with the ongoing announcements of new ammonia projects and the commodity crop prices and the overall index shown below are some of the key drivers of the activity in fertilizers but also are helping Ag equipment demand and we discuss the Deere results in today's daily report. We do not see how the trends in the chart below correct quickly and the profit through the farming, fertilizer, ag chemicals, and equipment chain should remain high in the US, at the expense of the consumer-facing high food prices (second chart below). We would need some coordinated medium-term policy to encourage moving more land in the US into agriculture, and this is especially necessary if we also intend to pursue bio-based fuels and materials. There has been much discussion around energy security over the last couple of months, but we think it is a much broader security discussion than just energy. Governments need to become much more accommodative around many aspects of production, food, energy, materials, etc. This accommodation can come with tighter emissions standards and emissions costs, but the primary objective should be to encourage more local production of many different things.

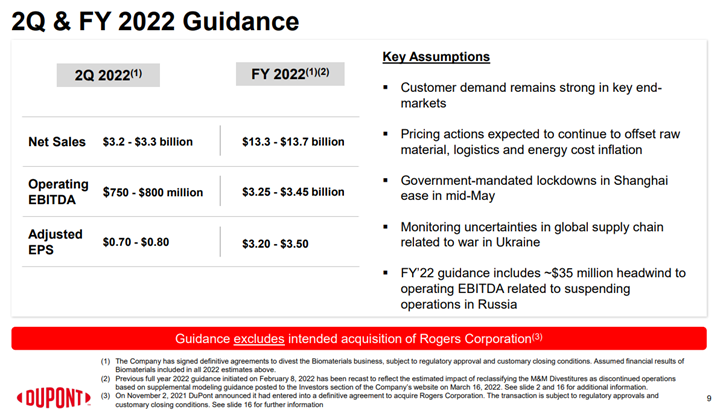

Like many of the European producers, DuPont has taken a risk in our view by holding guidance flat in the face of inflation, weakness in China, and a potential further economic slowdown in Europe and the US. We struggle with what an alternative approach should be for DuPont and others, given that it would be challenging to map out a credible downside scenario today. What we would note, however, is that when things turn negative for the materials industries they tend to fall quickly and sharply. For all of the base chemical and specialty chemical companies what might upset things for 2022 are largely outside of their control, and it is hard to second guess cutbacks in customer demand until they happen, especially in an environment where all are looking at volatile costs from energy and consumer spending uncertainty because of inflation. For more see today's daily report.

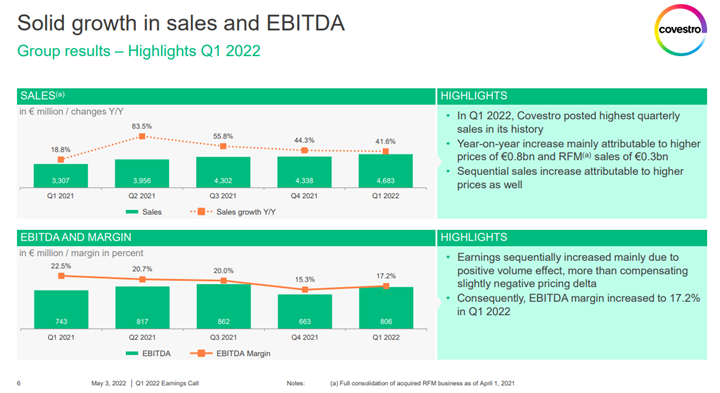

We reflect back on our BASF comments of last week and see Covestro falling into the same trap, by underestimating the potential slowdown in discretionary spending in Europe (and the US) and consequently putting too much hope into revised guidance. At the same time, we are not sure what would be gained by painting a picture of doom and gloom, but we would hedge much more overtly if we were offering guidance around the business outlook today.

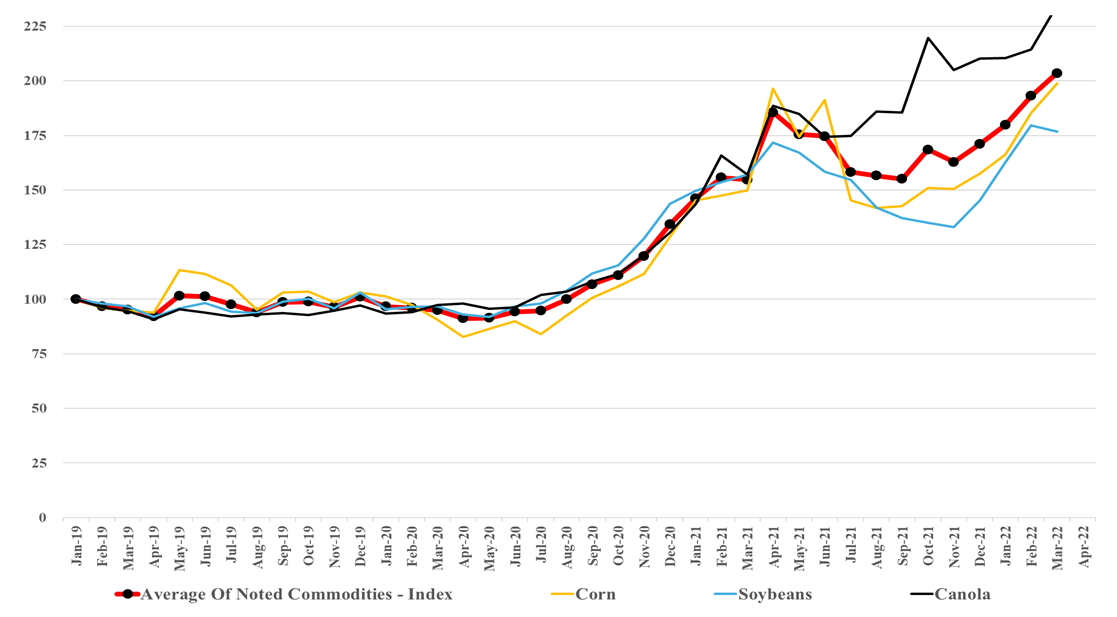

In our ESG and Climate report tomorrow, we are focusing on renewable materials and fuels, emphasizing counting carbon and the importance of verification and auditing. However, one of the side issues concerning renewables is their impact on food prices if they bid crops away from the food chain. The chart of the day from our daily chemical reactions report shows that corn prices are above their historical correlation with crude oil, but it also indicates a correlation and fuel markets can pay more for corn and other crop-based fuels when oil prices are high. The issue with exhibit below is that we already have inflated crop prices with minimal incremental demand for the fuel markets today. Prices are rising on strong global demand growth for food – supply chain issues that existed before the Ukraine crisis and – the supply challenges that are a direct consequence of the Ukraine crisis. This is before any significant investment in renewable fuels or materials. As governments implement policies to encourage renewable fuels – especially SAF – they need to consider what policies and incentives might be required in addition to price, encourage meaningful changes to the acres planted around the world, and help productivity where it is low.

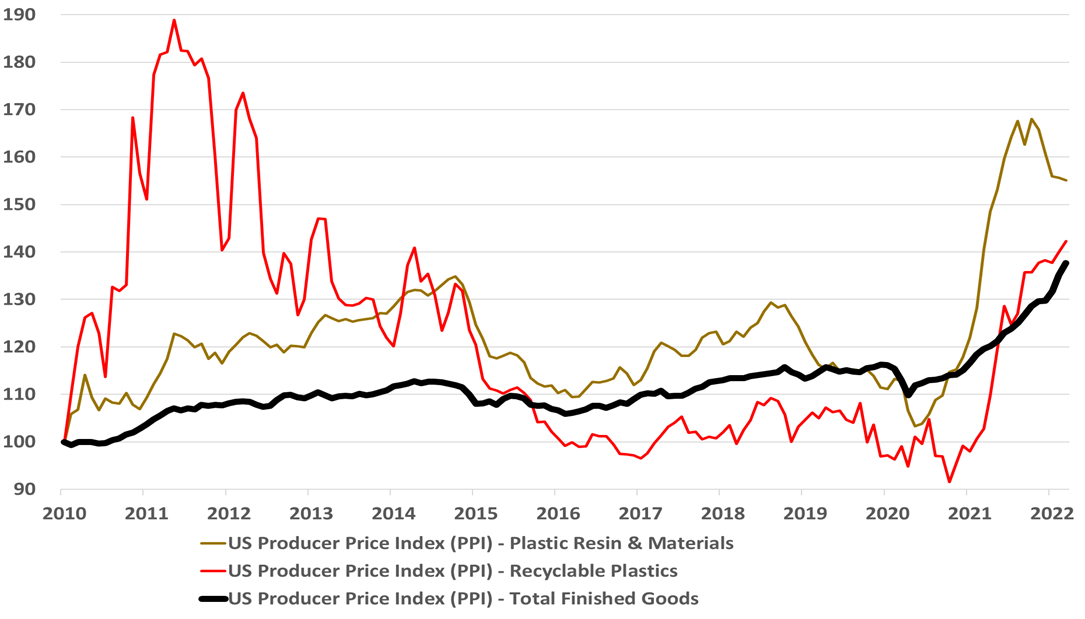

It is important to note from the chart below that the US plastic resin price index is out of phase with the overall industrial products markets as we saw a shortage driven peak in 2021 – largely weather and supply chain-related. The US on average continues to command resin price premiums relative to Asia. The China polymer surpluses are largely land-locked for now because of very high shipping costs and very high oil-based production costs, and the US surplus is also challenged because of logistic issues with exports. In the US, exporters are building inventory in anticipation of better logistics and on the basis that the surpluses for the most part have customers. If we do see a global slowdown in demand, triggered by inflation – see our most recent Sunday Recap – the inventories in the US and China could become a problem.

While we remain advocates of “stronger for longer” with respect to chemical demand and pricing in the US, the auto data does suggest that the US consumer may be cooling off a bit in reaction to higher prices and higher borrowing rates. Historically, the chemical industry has a habit of running headlong into a downturn while waving an “everything is great” flag, and the RPM results and outlook have a vague “deja vu” feel to them. We also note some surprise at the robustness of the MDI market in the chart below, and it would be wrong not to admit that our cautionary antennas are rising. The auto exposed products should still see some upside from higher auto production in the second half of the year, but otherwise, a possible consumer pullback to take the wind out of the sector sales, especially if the US is constrained moving out products because of container and shipping issues. The significant cost advantage remains in the US but the ethylene market over the last week is a reminder of what can happen when you struggle to find someone who can take the last pound. Given infrastructure, energy, and clean energy investment, as well as reshoring, many materials could see significant offsets to consumer spending pullbacks and our focus would remain on PVC and building products, as most of the hit would be in consumer durables. Metals demand should remain strong regardless. For more see today's daily report.

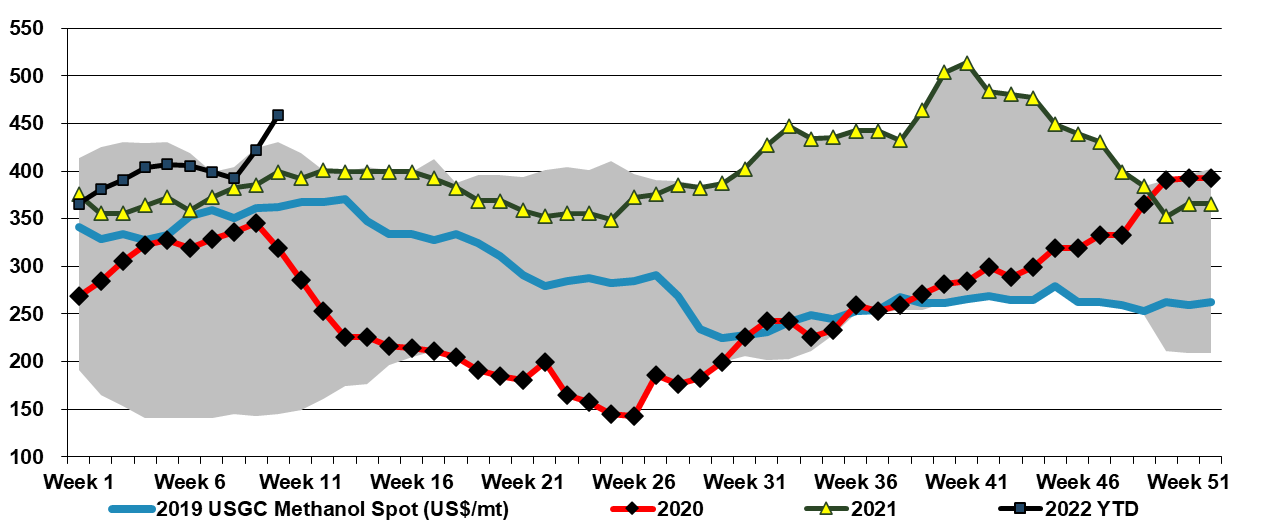

A couple of weeks ago we raised the idea that US methanol could be a significant beneficiary of the conflict in Central Europe, not just because it is very economically unattractive to make methanol in Europe, but because it might be possible for Europe to import methanol for its energy value - $40 per MMBTU natural gas can make all sort of alternates look attractive. The impetus behind the methanol spot price increase in the US may be in part rising local natural gas – or the fear of further increases – but export demand is likely the larger driving factor and this could continue or even increase further if potential European importers work out how to convert to use methanol as a fuel.

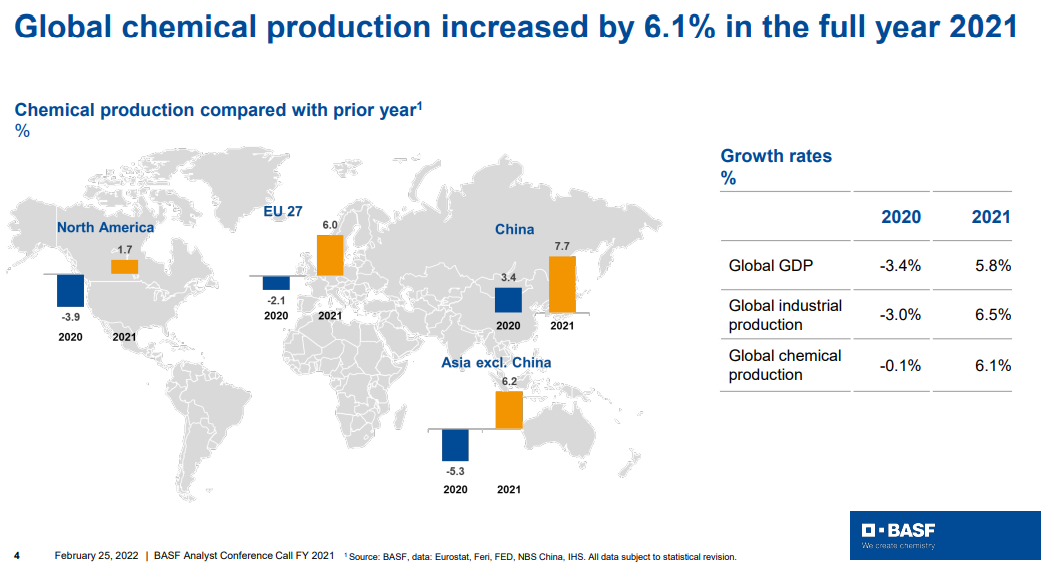

Fear of shortages is the one factor that is most supportive in terms of helping to push through pricing and the events in Europe and their associated impact on energy prices should be all the support that the chemical and polymer industry needs to push pricing through that will cover cost inflation. Buyers of raw materials and intermediate products will naturally look to buy a little more than they need in the near term, both to ensure that they get something ad to try to build a bigger inventory cushion. This will have the effect of pushing apparent demand higher, making the pricing initiatives easier. Few will push back on pricing if their primary concern is availability. Looking at the BASF results summarized in the chart below, demand is already very robust and this will lead to higher utilization rates and higher volumes for chemical producers as well as high pricing. The commodity producers are likely more interesting here as they can move prices much more quickly than the specialty companies who might see margins squeezed over the next couple of months. None of this is good for inflation. See more in today's daily report.

It is likely a difficult day for the European chemical industry as all of the fuel prices that they depend on are rising quickly, which will force many difficult decisions over the coming days. There are a couple of factors to consider – what happens to costs and margins if energy prices remain inflated, and what happens if energy availability becomes an issue and plant closures are necessary. In a world that is already reeling from inflationary pressure that we have not seen in four decades, there is at least an acceptance that prices can move higher, but the energy-dependent European industrial and materials companies will need to move prices quickly and meaningfully to absorb their higher costs. If natural gas supplies from Russia are halted, Europe is likely going to need to allocate supplies, as there is no easy fix given an LNG system that is already at capacity. Industry will likely take the hit to ensure power for heating and cooling. This will drive product shortages in Europe, especially for chemicals, which will likely make it easier to get the pricing necessary to cover costs.

While it has been a long time coming, and it is unclear whether COVID hindered or helped, the DuPont materials exit is not a surprise and we noted after the IFF deal that we believed that Ed Breen was not done. During his time at Tyco, Mr. Breen showed a very clear ability to identify better owners for businesses that were lost in a conglomerate structure. We had always anticipated the same with DuPont and the business that is moving to Celanese is one we had expected to move and we had discussed previously. This should be a win for both companies as DuPont begins to look much more like a stable margin specialty chemical company with a portfolio that is becoming more ESG centric – see today's daily – while Celanese now has a large and comprehensive portfolio of polymers that are critical to the transport sector and should be able to drive both revenue and cost synergies if the company manages the integration well.