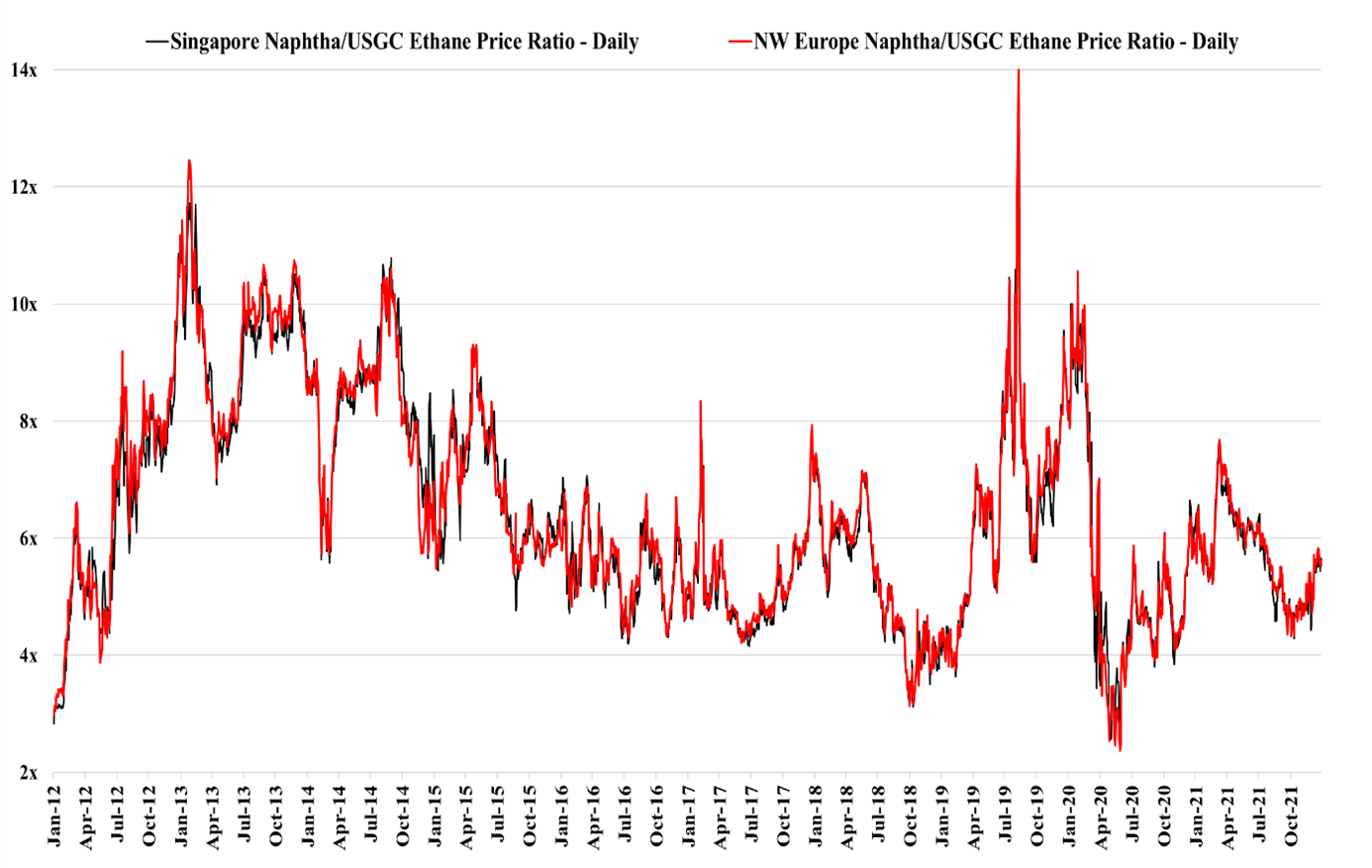

Looking at the exhibit below, it is clear that planning for consumers of hydrocarbon feedstocks is a challenge, and this is especially true for anyone looking at new projects, adding to our view that new project announcements will slow in basic chemicals, setting up for a major upcycle after 2023. The volatility in relative feedstock prices over the last ten years likely means that you would need to be able to demonstrate profitability under a wide range of possible feedstock price scenarios, while at the same time assuming that prices are set by marginal costs. Today global prices are set by marginal costs as parts of Asia are operating at break-even economics, with the much more profitable US and Europe impacted by feedstock advantages in the US and higher freight costs for polymers trying to enter the US and European markets. The US trade balance discussed in today's Daily is partly influenced by rising prices on some imported goods because of higher freight costs. While we continue to see some basic chemical expansion announcements, there have been periods of relative feedstock costs over the last 10 years where any project would have looked unprofitable. The volatility in the chart confirms that any producer will have better and worse times throughout a facility’s operating life, and consequently, start-up timing can be everything. Losing money for the first few years of any project’s life can destroy any ROI goals.

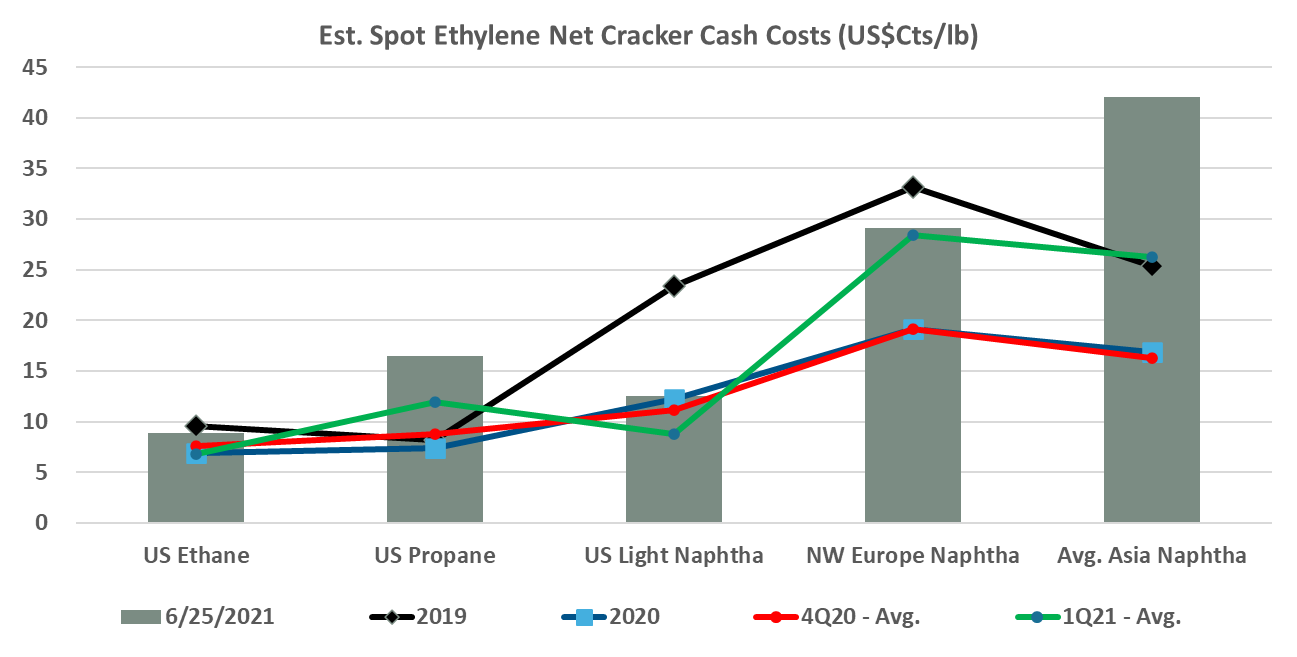

The chart below focus on the ethylene cost curve and show that the US currently retains a distinct cost advantage despite escalating domestic feedstock costs. The current cost advantage in the US is sufficient to move ethylene derivatives into most markets profitably and while US spot prices for ethylene may not quite reflect the levels needed to stimulate exports today – US ethylene costs certainly do. The restart of the Nova unit in Louisiana may put some further downward on US ethylene prices but as we discussed yesterday, given the weather risks in 3Q it is an interesting dilemma today over whether you sell surplus ethylene or store it on the basis that spot prices will rise because of production outages – this time last year the “store it” decision would have been the right one as spot prices rose through 3Q.