We have talked at length in today's daily and recent Sunday recaps about our expectation for a mega-cycle in chemicals because of an unwillingness to deploy capital as uncertainty rises. The exception is likely to be large oil producers looking at long-term downstream integration plans, with the primary objective of consuming captive crude oil. The Aramco ambitions in China bear some similarities to the ExxonMobil investment announced for China last year. While the crude oil market may be tight and prices may be high today, few oil producers believe that demand will not ultimately be hurt by renewable penetration and EV and hydrogen growth as transport fuels. Looking for captive crude oil demand is a logical step for the major and it is likely that the Aramco ambitions include refining as well as chemicals in China.

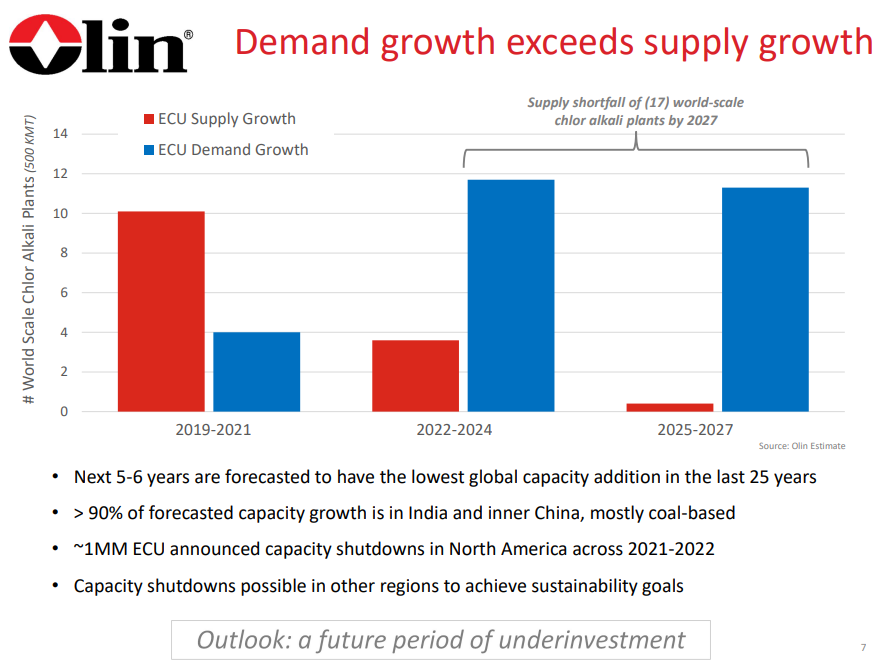

We are already seeing the impact of ESG-pressure related underinvestment in many commodities, and the picture that Olin paints around chlor-alkali is not dissimilar to some of the analyses that could be done around some metals today – especially those that are critically important to the EV, Solar, and Wind industries – this is a topic that we have covered at length. While chlor-alkali may be a pressing very near-term example of how underinvestment could impact chemicals, we suspect that the issue may be much broader, just not yet apparent in other sectors because of the wave of new investment from 2017 through 2022. The polyethylene equivalent chart to the one below would show more balanced supply/demand in the 22 – 24 period than for chlor-alkali but the same deficit thereafter. Many of the other base chemicals would look the same. This supports our expectation of an industry mega-cycle, possibly starting as early as 2023. Of course, there is time to add new capacity by 2025/26, but most companies are more focused today on how they comply with tighter environmental standards today than they are on their next expansion. Further hindering new expansion-driven capital investment decisions is the uncertainty around polymer demand (how much will be recycled, will there be more bans, will there be a substitution from other materials). Our view is that base polymer demand will continue to grow and that we will run short as a consequence of underinvestment. See our report titled - Waiting For The Big One – Is A Chemical Mega-Cycle Ahead?

The Air Liquide announcement linked is consistent with the widely held view that semiconductor markets desperately need new capacity and shows that existing China-based manufacturers are stepping up. Air Liquide will supply new capacity in Wuhan, where it has been an active producer of high purity gases for the semiconductor industry for decades. While this is likely a sound investment for Air Liquide, backed by strong “take or pay” agreements from customers, the risk to the expansion is that while the world is in dire need of new semiconductor capacity, it is unclear how much of that need is for more China-based production. There is significant semiconductor demand in China and that demand will continue to grow, but consumers in the West are not only looking for more semiconductor supply but also more semiconductor supply security, and with the concentration of production in China and Taiwan, supply from outside the region is more desirable. We see new semiconductor capacity announced for the US and the auto industry, in particular, is calling for more diversity of supply, not just for semi’s but also for other EV components, especially batteries. There is already anecdotal evidence of a preference for non-China-based materials – all the way back to lithium - but how much more US and European producers are willing to pay for this “preference” will dictate the ultimate level of spending. Despite these concerns and absent broader geopolitical risk, this is likely a relatively safe project for Air Liquide and the capital commitment is not going to break the bank.