ExxonMobil Chemicals has announced that its Corpus Christi JV project with SABIC is ahead of its original schedule – ExxonMobil is now targeting a start-up in 2H21, ahead of its previously targeted 1H22 expectation. It is unusual for projects in the US to be ready ahead of schedule these days, and start-up delays tend to be the norm. We also take a positive view of this development upon comparison to the Shell Pennsylvania project, which still has a vague 2022 start-up expectation though its construction began before ExxonMobil. One could argue that the remoteness of the location – well away from petrochemical infrastructure has been a constraint for Shell, but the Corpus Christi location is also a greenfield project for ExxonMobil/SABIC. This will be the largest ethylene plant built in the US, though it is likely that the recent 1.5 million ton units (Dow, ExxonMobil, CP Chem) are expandable to 2.0 million tons. Dow is already discussing such a move with a new polyethylene facility at Freeport. It will be interesting to see what impact this ExxonMobil/SABIC facility has on both the USGC ethane market and the polyethylene market – 1.3 million tons of polyethylene is a large increment and SABIC will have half of the capacity and will be a new market entrant with on-shore production. Aramco has ethylene, through Motiva’s purchase of Flint Hills, and SABIC owns half of the Cosmar styrene plant in Louisiana.

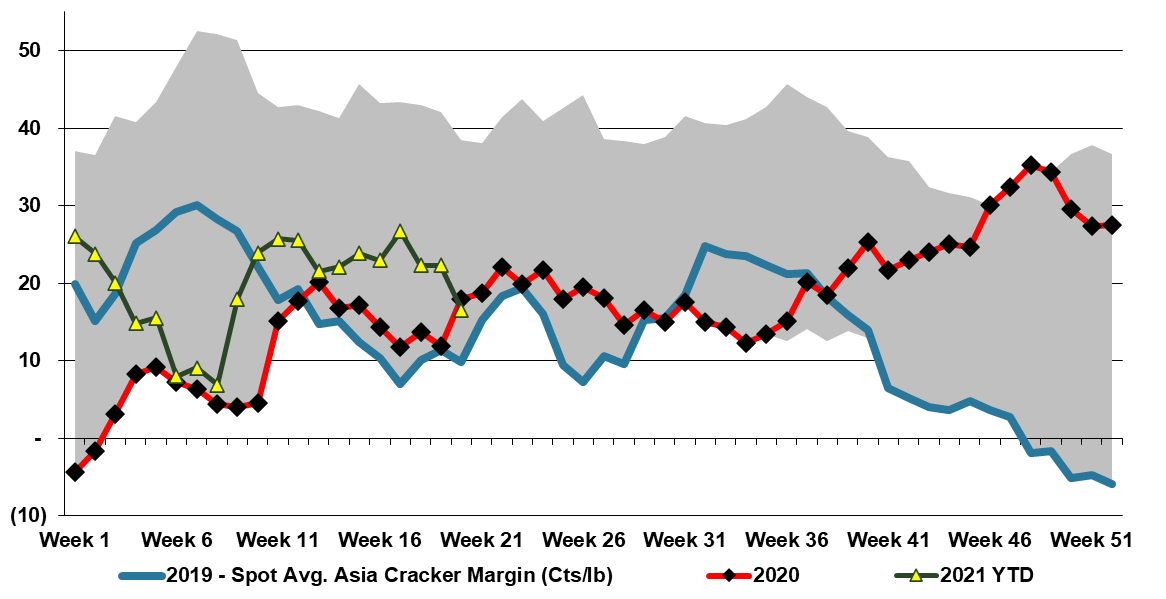

This headline about China creating petrochemical deflation is largely based on the rate of capacity addition within China and that base chemical pricing in China still sits well above costs – but the argument may be flawed on a couple of levels. First, costs may not fall materially, given the increased thirst for imported naphtha and propane, as well as crude to fill new refining capacity. If crude prices fall, China will see lower costs, but then so will others. The margin issue is also in question because the wave of China’s new base chemical capacity is arriving amid a surge in demand growth, and this is why margins in Asia have not fallen closer to costs yet. China remains a meaningful importer of many base chemicals – less than two years ago for many products, but still meaningful, and it is the surpluses in the US and the Middle East that may drive deflation should supply chains stabilize and production rates remain high.