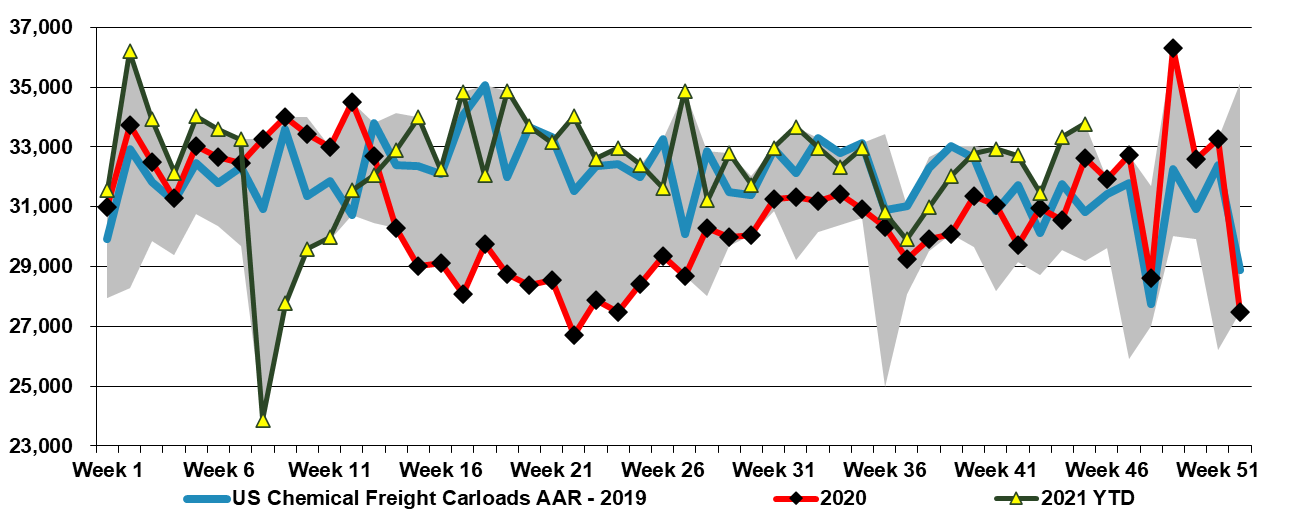

In the first Exhibit below we show a 5-year high in chemical rail-car movements. We have noted in research since early October that 4Q production in the US could be very high because of a combination of available capacity – following a year of weather-related delays – and very attractive margins and demand. We have been at the high end of rail car volumes for most of the quarter, and this may be part of the reason why we are seeing some price weakness for polymers in the US. Most of the polyethylene exported from the US moves from the manufacturing site to the export port via rail, so increased exports would also drive higher rail car numbers. As long as pricing and margins remain high and customer demand robust, we would expect these higher volumes to continue. This does not make us any less concerned that somewhere in the chain there is now an inventory build going on and that fortunes could reverse in 2022.

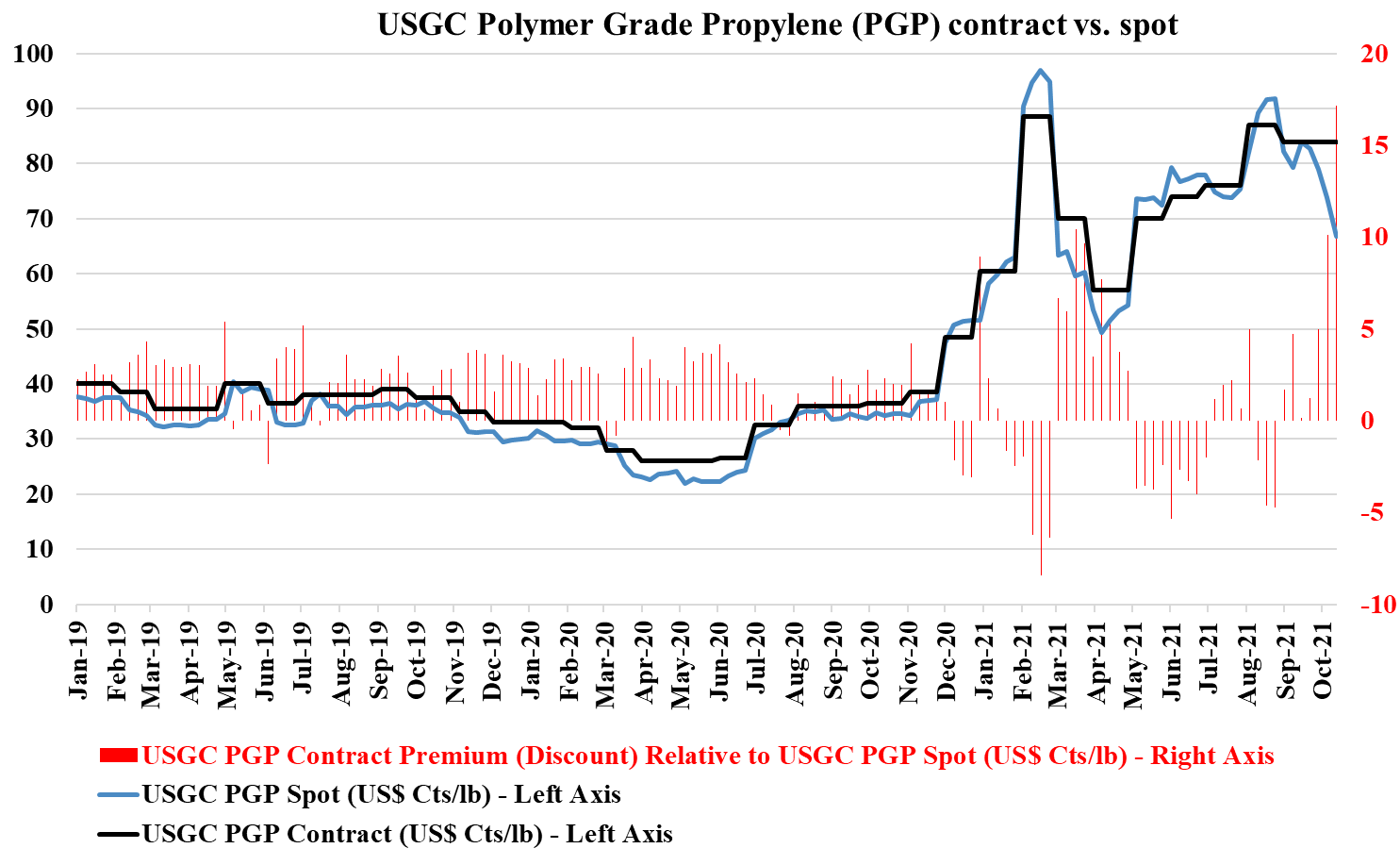

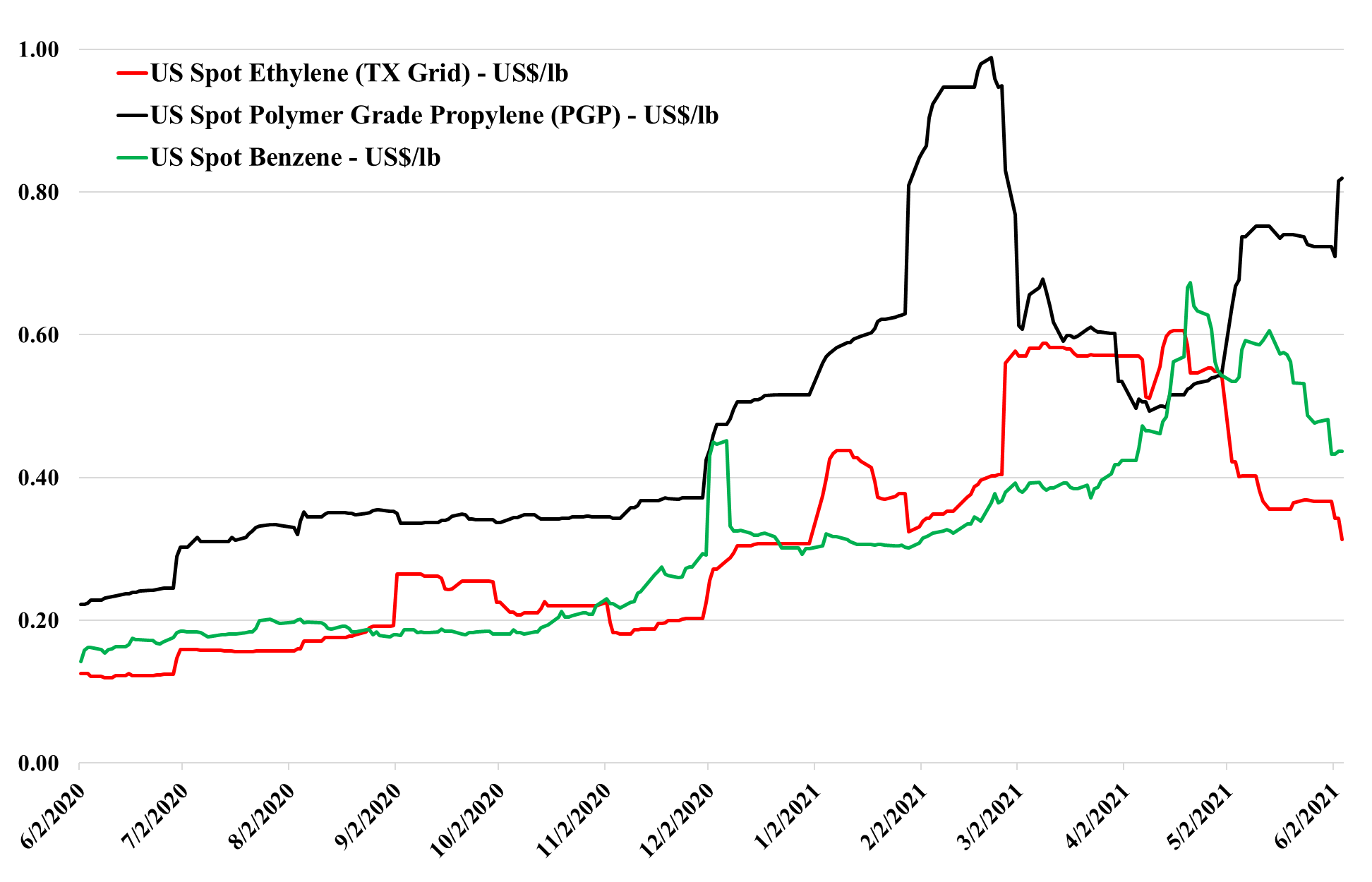

The propylene chart below shows a significant disconnect between spot and contract prices – more than at any point in recent history, and if the US contract price does not fall it will likely be an indicator that either discounts have increased or that more volume is moving against a spot price marker. The pressure is also on to lower ethylene contract prices, but the propylene spread is far more extreme.

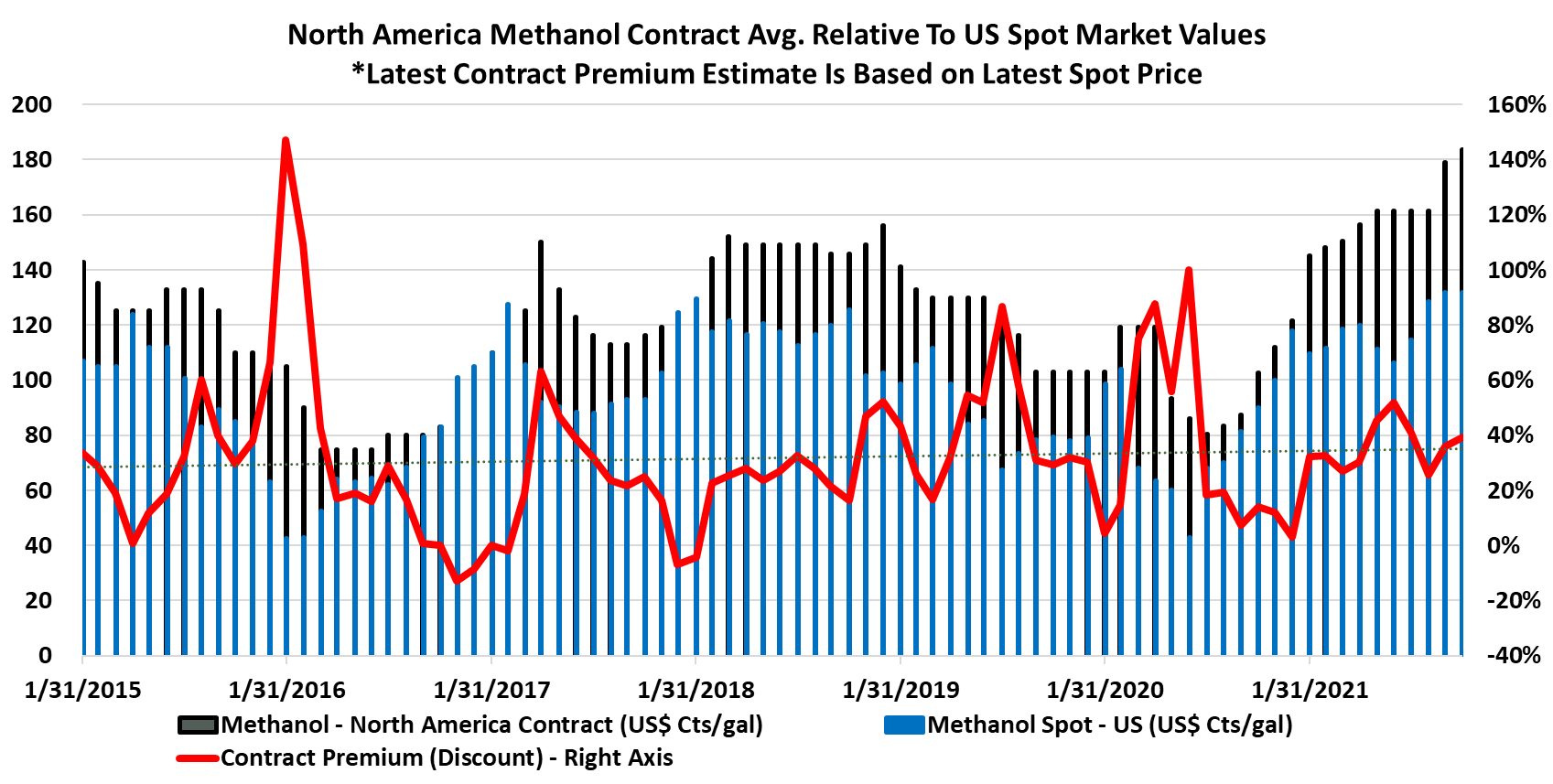

The charts below show that North American methanol pricing is seeing support from higher natural gas prices as you would expect, but we are also seeing some significant price improvement in China, See more in today's daily report. If China is coal constrained, as suggested in many of the power-related stories, it may be impacting chemical production from coal at the margin. Alternatively, with LNG prices so high and imported naphtha and propane prices rising in China, the country may be using more coal at the margin to make chemicals.

We have a fairly stable week for US olefins so far – no new production disruptions, but the industry is still recovering from the storm-related shutdowns over the last 4 weeks. We still believe that there is a downside to ethylene and propylene in the US as production recovers and as demand normalizes (especially for propylene). With another month of hurricane season to go, however, it probably does not make sense to force surpluses into an export market where prices are much lower – especially for ethylene. As we have noted in the past, the right strategy in 2020 was to store the ethylene at this time rather than sell it. Inventories would likely have to rise further before those with surpluses were willing to take the cut needed to export. At the same time, rising natural gas and NGL prices are another reason to hold on to products as what you have today did not cost that much to make and costs may rise near term. See more in today's daily report.

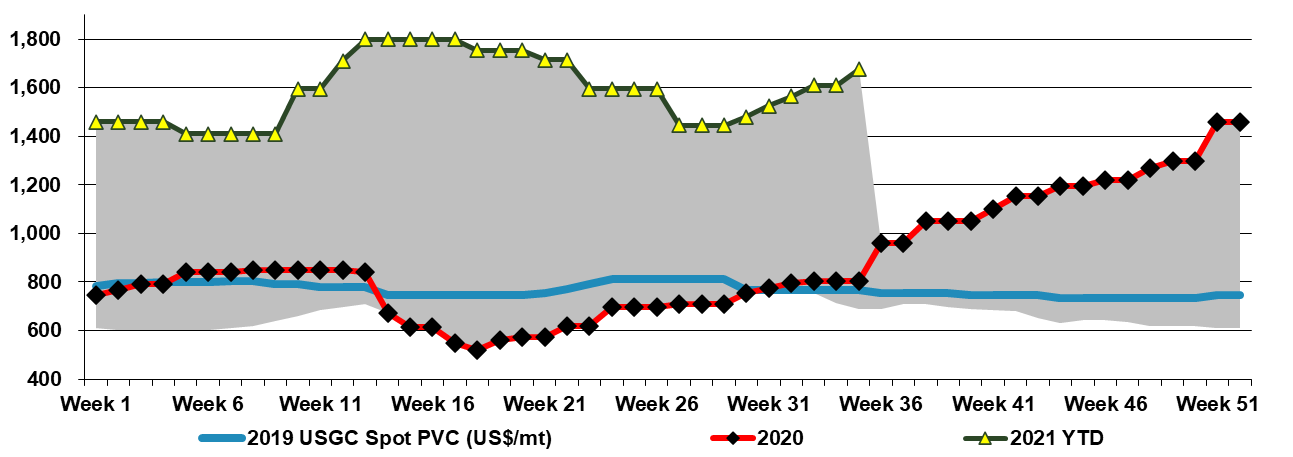

It is increasingly likely that Hurricane Ida will add another leg of strength to US chemical pricing more broadly, with a host of prolonged production outage news and force majeure notices, giving momentum to some price increase announcements for September, some of which looked very speculative at the time they were made. Buyers will have an eye on continued pockets of supply chain disruption, strong demand in general, particularly for those levered to holiday spending, and the not insignificant fact that we still have almost three months of hurricane season to go! Note that two of the more disruptive storms of 2020 hit in October. We talk specifically about PVC in today's daily - See price chart below.

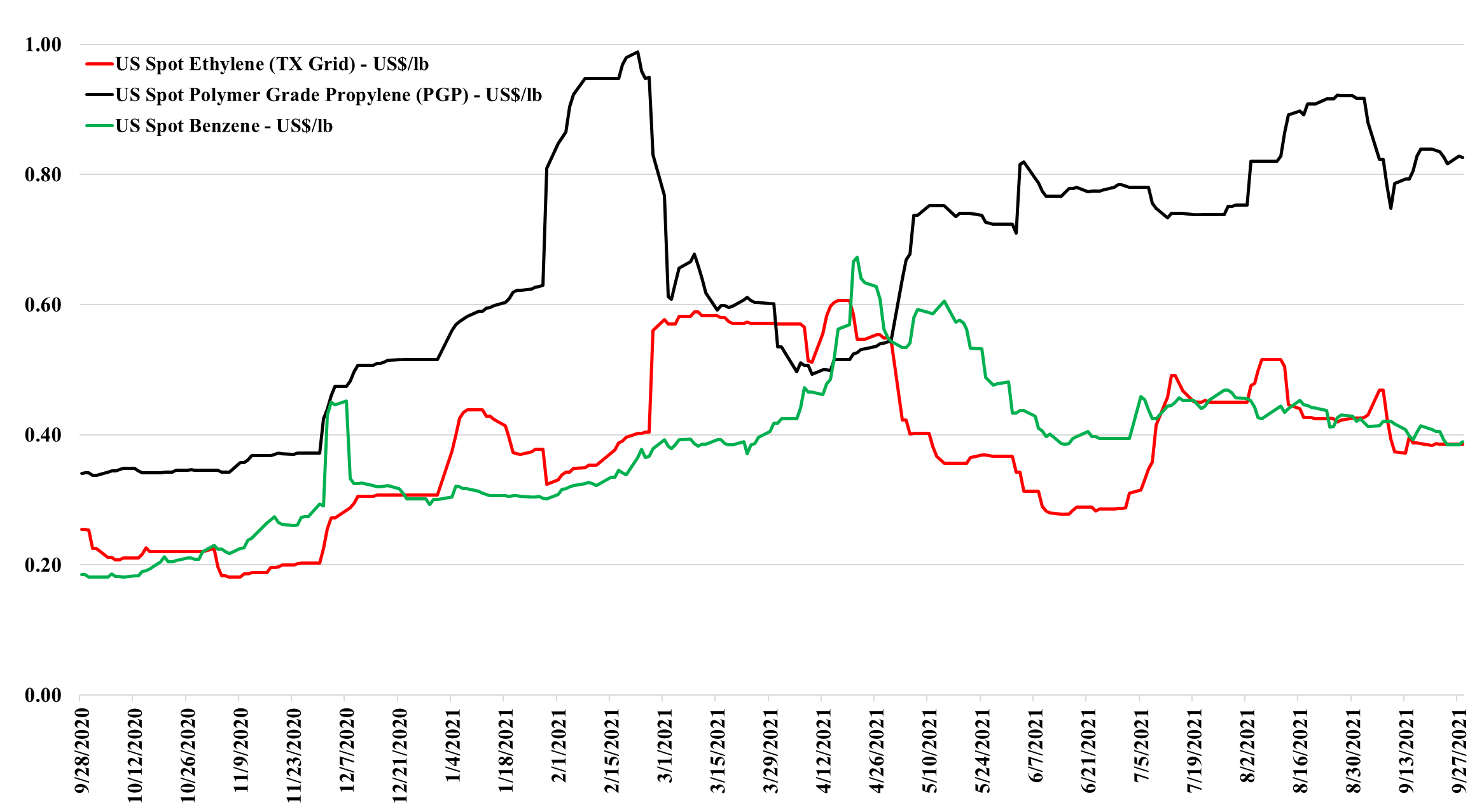

The oversupply in China for many commodities is becoming more evident daily. Our research depicts this as supply-driven, based on the surge of ethylene and propylene and derivative capacity since 3Q 2020. Notwithstanding the Dow commentary (in our daily report today), the weakness in Asia in polyethylene will ultimately impact the US, as the US relies on international demand for at least 25% of its polyethylene production – much less for polypropylene. The gyrations in the ethylene and propylene markets, as shown in the chart below, indicate the US dealing with the differences between the two monomer chains. Far more ethylene and ethylene derivatives move offshore than propylene and propylene derivatives. Despite the ongoing strength in derivatives, the ethylene market is loosening. At the same time, propylene shows extreme volatility because demand remains strong and has seen greater production issues on a relative basis, per our estimate. Supply is barely keeping up, even as refinery rates increase, because of problems with PDH units, pipelines, and splitters, which would not be meaningful in a more normalized market, but make a difference when refinery supply is constrained. High propane prices, which could move even higher, keep upward pressure because of PDH economics and because they keep propane out of ethylene units.

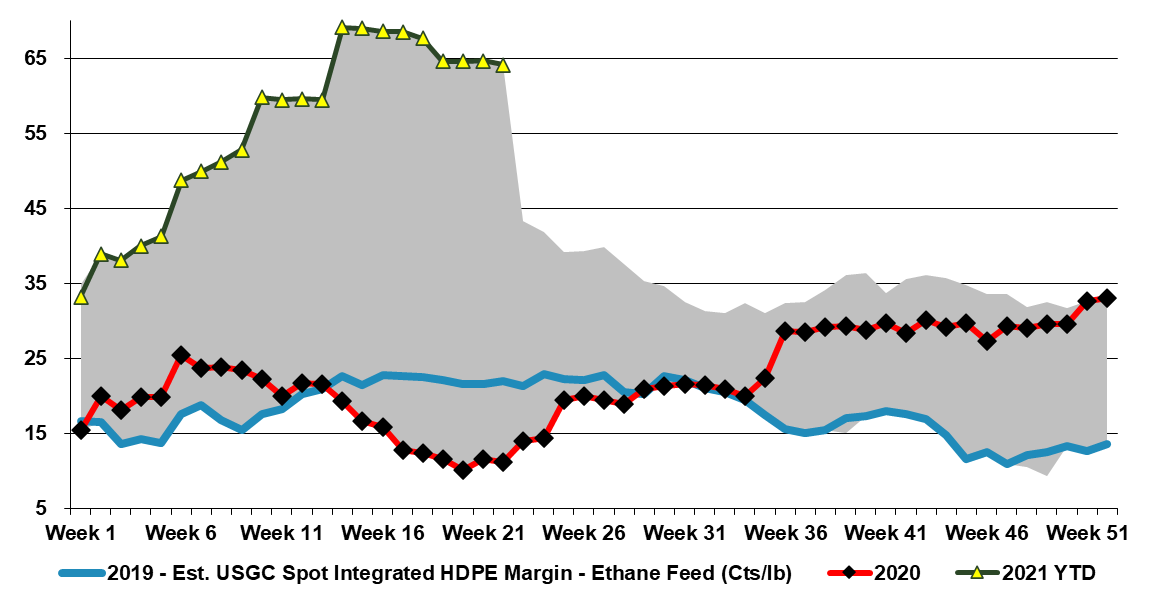

The Dow announcement yesterday speaks to a much larger issue within the investment community in our view, which is that research fees have come down so much over the last ten years that the sell-side gets paid very little for doing any real research. We talked about the upside in 2Q for the commodity polymer producers for months. Still, we know that we cannot get paid for maintaining the models needed to get to the numbers with enough confidence to publish estimates. The buy-side does not have the budget. In the past, as sell-side analysts, we would subscribe and talk to price discovery consultants, such as the predecessor companies of IHS (now in the middle of an acquisition by S&P) and CDI (in the middle of a merger with ICIS). This data and these dialogues would allow us to adjust earnings estimates during the quarter and keep up alongside our other work (e.g. corporate marketing/roadshows, etc.) as analysts. There is enough data in our weekly report – published each Monday to do this for many companies. (See an example in the chart below). Today, IHS has made its service so expensive that it is difficult for sell-side analysts to justify the cost when they are not getting paid by clients for real, fundamental research. The JP Morgan alleged base fee for research for an entire platform would not cover 25% of the IHS subscription cost for olefins and polyolefins data alone, per our estimate. Plus, all the merger activity at the data providers is causing some to question quality. The result is limited mid-quarter analysis from the sell-side and moves like Dow’s so that they can have realistic conversations with investors. In the case of Dow, it was to get the message out ahead of the Bernstein Conference.