We have talked at length in today's daily and recent Sunday recaps about our expectation for a mega-cycle in chemicals because of an unwillingness to deploy capital as uncertainty rises. The exception is likely to be large oil producers looking at long-term downstream integration plans, with the primary objective of consuming captive crude oil. The Aramco ambitions in China bear some similarities to the ExxonMobil investment announced for China last year. While the crude oil market may be tight and prices may be high today, few oil producers believe that demand will not ultimately be hurt by renewable penetration and EV and hydrogen growth as transport fuels. Looking for captive crude oil demand is a logical step for the major and it is likely that the Aramco ambitions include refining as well as chemicals in China.

The Huntsman activist defense presentation highlighted below does a very good job of explaining why Starboard is focused on a set of concerns that the company has already addressed and while we would generally not comment on something like this, we agree with Huntsman’s assessment that the proposed Board changes bring nothing to the table. Where the Starboard activity may help is improving Huntsman’s communications, as while the company has done a good job, in our view, of repositioning, it has done a less good job, until now, of communicating what the changes mean. The presentation linked below does a much better job than anything we have seen from the company in the past. To be fairer to Huntsman, the chemical industry has always had trouble communicating strategy shifts and portfolio transformations to stakeholders and there have been several instances of good stories not turning into good businesses – Eastman had some false starts in the past but has not been alone with these problems. It often takes some time for investors to believe in a new business model and this is where good corporate communications strategies can help. This presentation is a good start for Huntsman.

More earnings releases and more discussions of disruptions and higher costs! One thing that is clear from all the reports we have followed, whether from basic chemical companies or those downstream, is that no one has any expectation that the supply disruptions and inflationary drivers are going to end soon. In our Sunday Thematic, we talked about the possibility of demand remaining robust and possibly absorbing new supply in 2022 because of further inventory builds. The idea is that holding more working capital, while possibly less efficient financially, may be more prudent from a business continuity perspective, especially given the reputational risk of failing to fulfill customer orders. While there is appropriate concern that interest rates could rise significantly, lending rates are so low that the cost of holding more inventory would be immaterial for many companies. For many products in the chemical chains and across materials more broadly, global oversupply, where it exists, is not high, and a further upward swing in inventories in 2022 could easily keep tight markets tight and swing some more balanced markets to shortages.

With the linked Ashland release, we see another example of a downstream chemical maker struggling with higher input costs and general logistic constraints, and an inability to push through pricing quickly enough to avoid a margin squeeze. The opaqueness that Ashland discusses concerning some of the planning metrics for the near-term is impacting forecasts and estimates for many more companies than just Ashland but given the costs and the supply chain challenges, all are encouraged to push through pricing aggressively, and this suggests that we are far from done with the materials inflationary pressures that we have discussed at length in prior reports and the higher costs of some of these specialty chemicals will start to impact customer margins through 2022. Almost all the earnings reports that we see discuss strong end-market demand and whether this is final customer pull-through or a need to address chain inventory or both, it should support further price initiatives. For more on our inflation views see Inflation (Especially Energy Costs) – Biggest 2022 Wildcard.

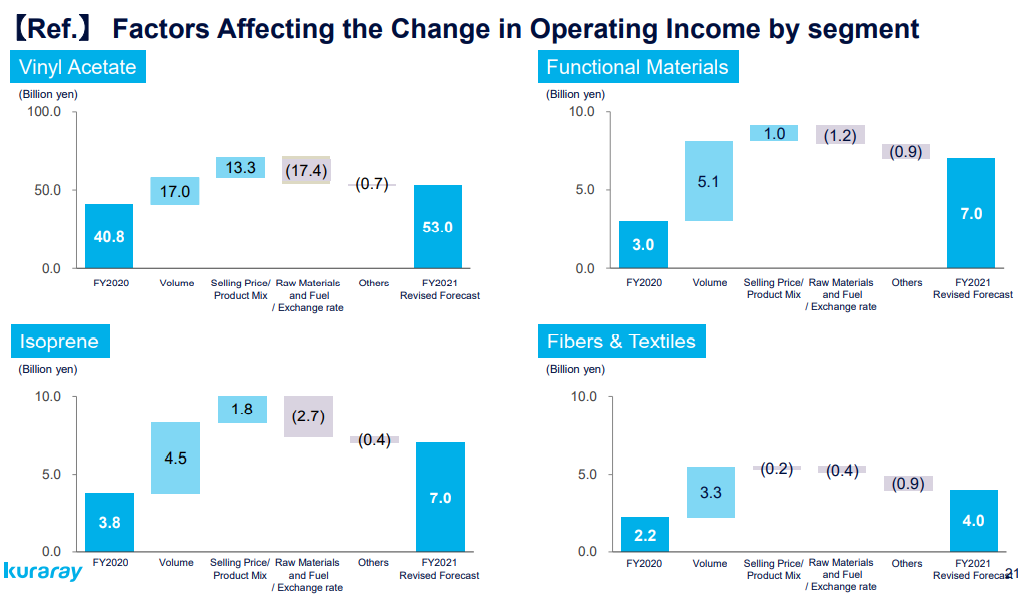

The 2Q volume driver of Kuraray’s earnings recovery was substantial, partly because end-market demand is strong and because this more mid-stream and specialty portfolio has significant operating leverage, much more than you would see from the commodity producers. We find this as a notable downstream sector trend to keep in mind. As seen below, increased selling prices are an important driver of Kuraray full-year profit growth expectations, but the volume piece is the most critical component, in our view. As discussed in our daily report today available in LINK, we continue to see volatile but elevated basic chemical prices.

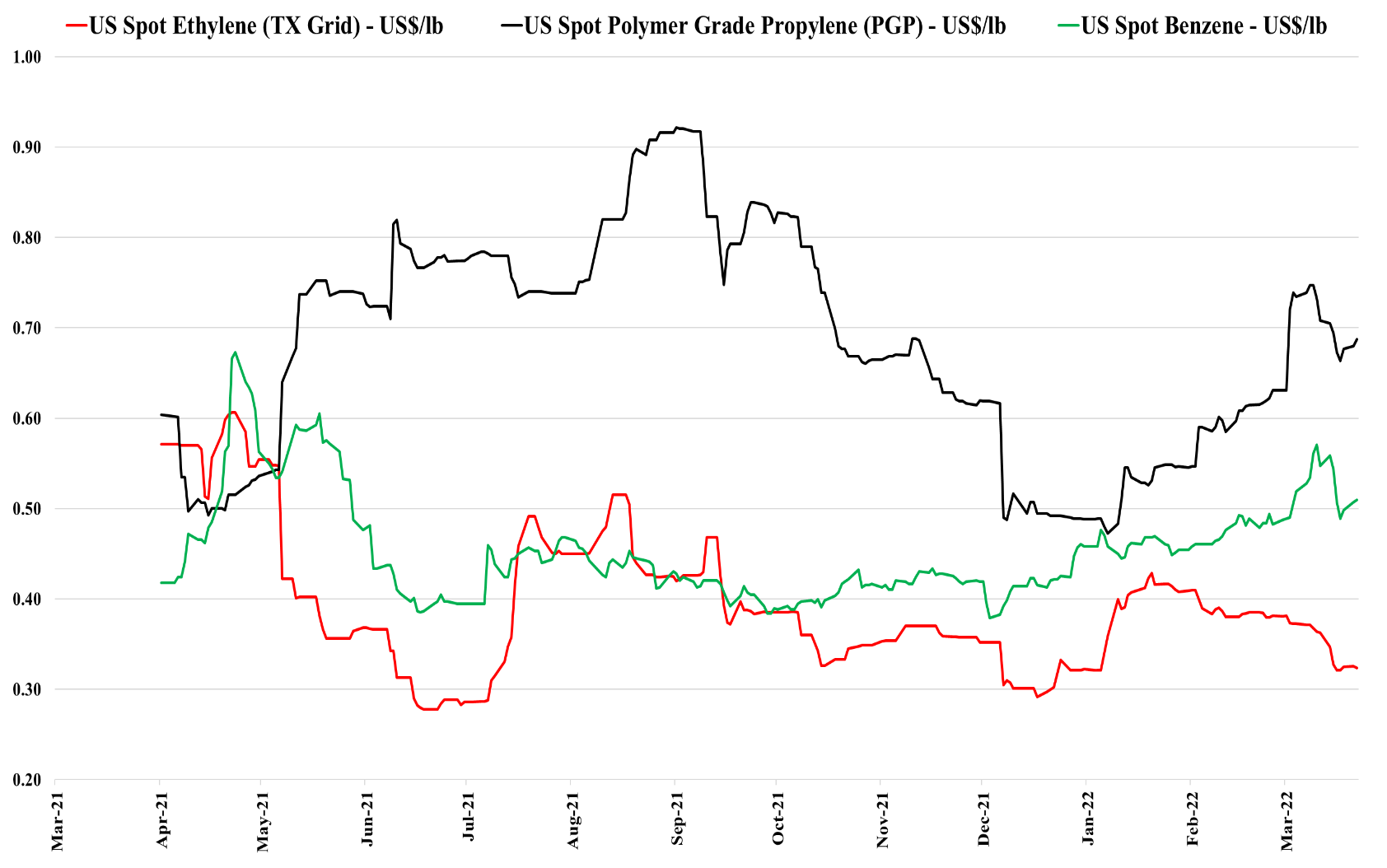

There is an interesting difference between the base chemicals markets and some of the other broad commodities and intermediates, and we have economic growth that is testing the capacity limits for many commodities and downstream products, but the overbuild in basic chemicals, most recently in China, is putting significant downward pressure on pricing, as we highlighted in yesterday’s Weekly Report. Capacity shortages in intermediates and some specialties, which are driving the investments we highlighted in today's daily report and which are a steady flow of news this year, are leading to some expanding margins over base chemicals in select areas where capacity has not kept pace with demand.