As noted in Exhibit 1 from today's daily report, the jump in oil prices has plunged the European polyethylene producers into the red and pushed Asian polyethylene producers further into the red. This will inevitably result in price increases as basic chemical and polymer producers will shut down at negative margins, and these price rises offer an opportunity for the US, Middle East, and select other producers.

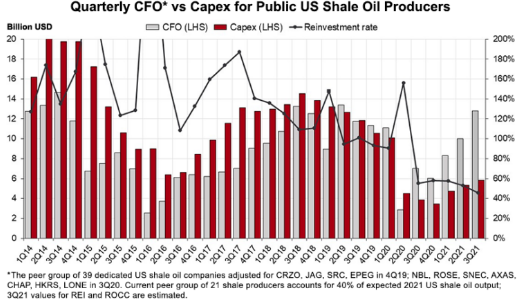

We should probably link the message in the exhibit below with the write-ups in both today's daily report and today's ESG and Climate report. The drop in E&P spending relative to cash flows and the shortage signals that are evident from the current oil and natural gas prices is likely to bump into rising hydrocarbon demand for the next several years, while the rate of renewable investment tires to catch up with energy growth before it can focus on energy substitution as meaningfully as the climate agenda would like. We also cannot look at the chart below and say that it does not matter because oil is less important in energy transition than natural gas. The oil-based investments in the Permian and Eagleford plays, in particular, have significant volumes of associated gas, and much of the natural gas supply growth in the US has come from these oil-centric investments. As they slow down, natural gas supply and NGL supply will be impacted, and while we are seeing increased rig counts in the natural gas biased regions, such as the Marcellus, the potential declines from the other fields will be hard to make up for.

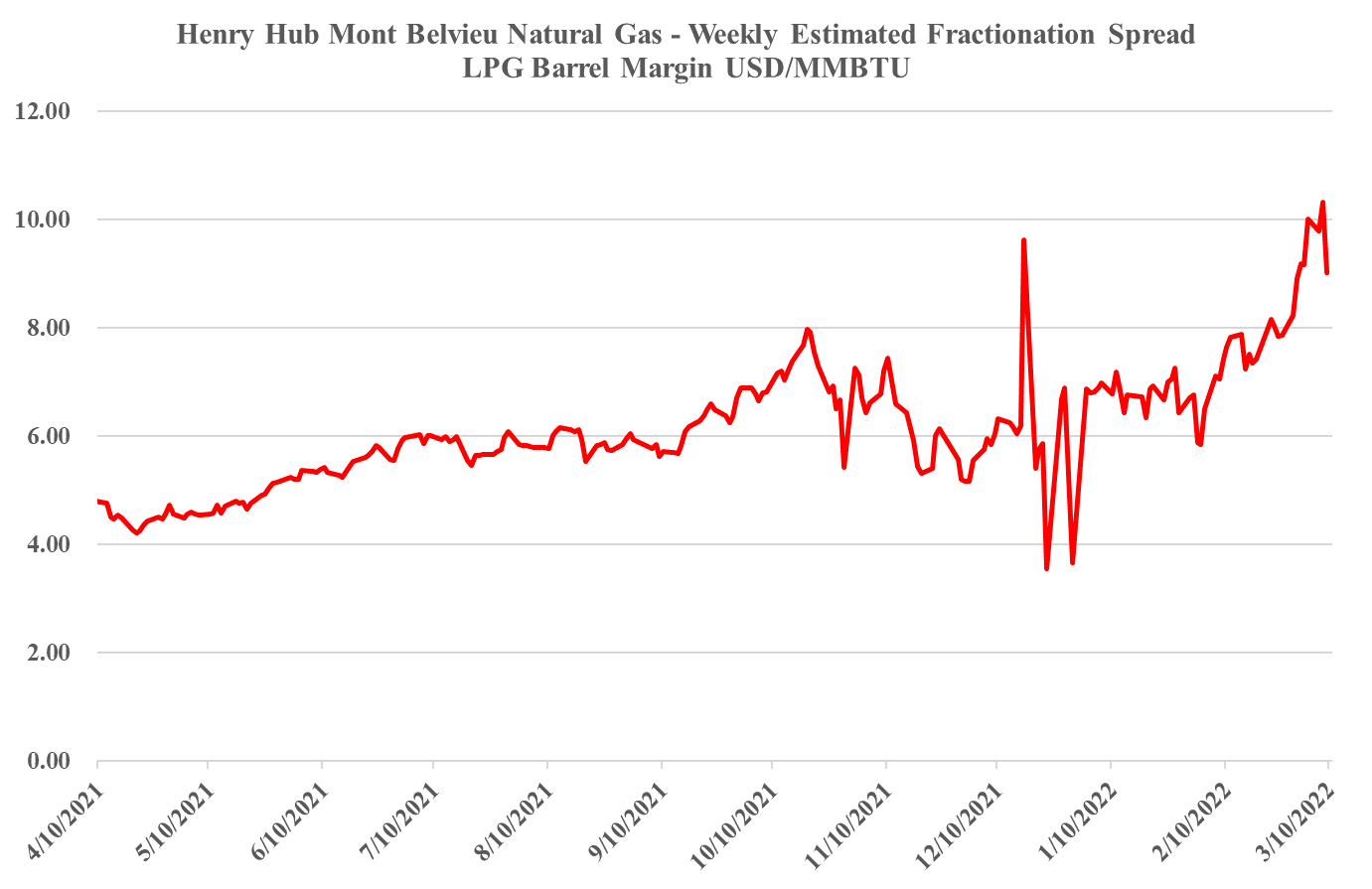

The US petrochemical production cost competitive advantage reflects a sharp decline at the feedstock level. Natural gas and natural gas liquids prices have risen faster than crude oil and Ex-US naphtha values since mid-1H21. In yesterday's report we identified the disconnect between propane and ethane pricing in the US. While both are high, propane is so high that it is now unprofitable to make ethylene from propane instead of just less profitable. The direction of the lines in the exhibit below shows the changing landscape clearly, and the only reason why the US chemical industry is so much more profitable than the markets in Asia is that chemical product prices are so robust, in part because of the high cost of freight between the regions.

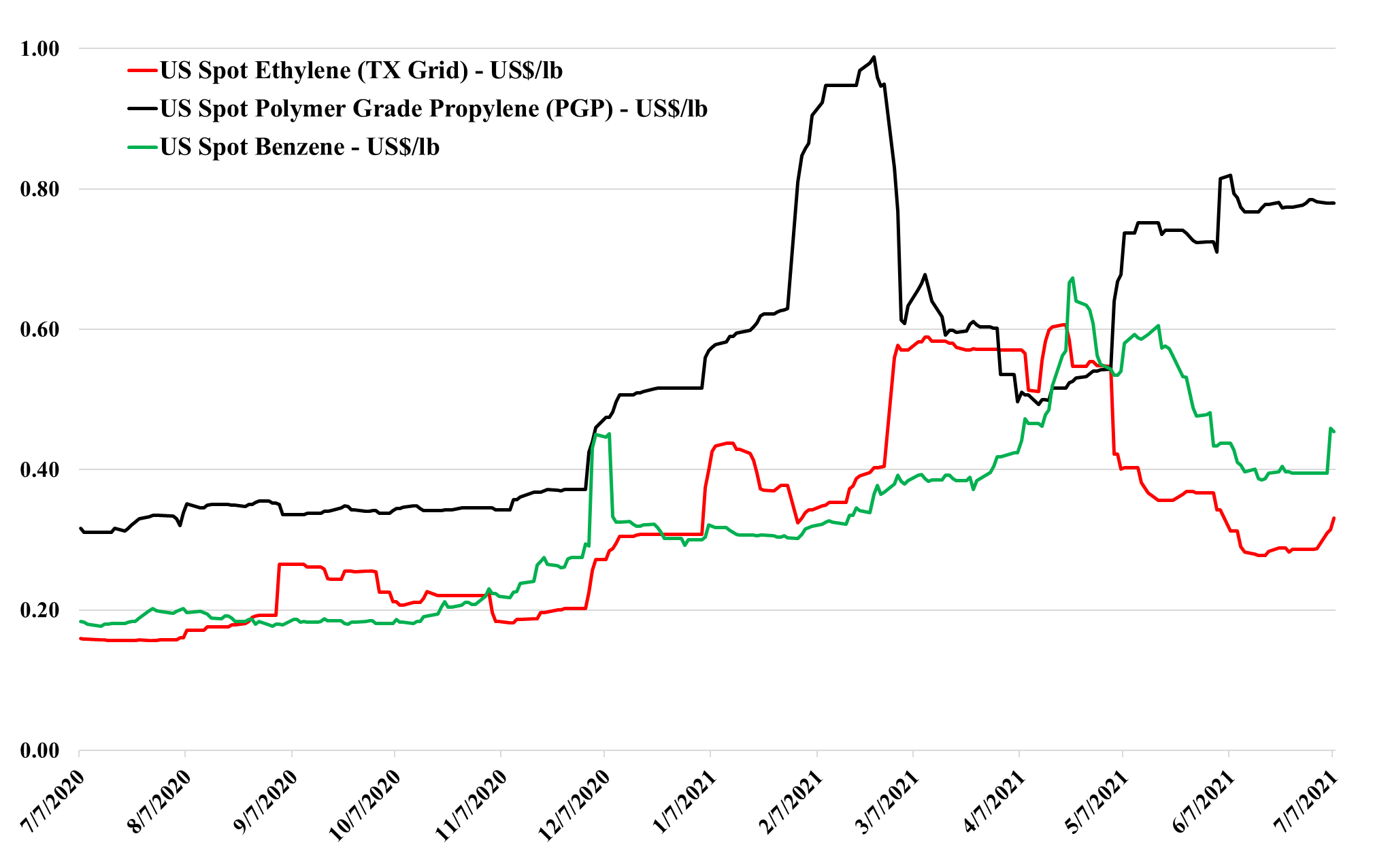

We have a fairly stable week for US olefins so far – no new production disruptions, but the industry is still recovering from the storm-related shutdowns over the last 4 weeks. We still believe that there is a downside to ethylene and propylene in the US as production recovers and as demand normalizes (especially for propylene). With another month of hurricane season to go, however, it probably does not make sense to force surpluses into an export market where prices are much lower – especially for ethylene. As we have noted in the past, the right strategy in 2020 was to store the ethylene at this time rather than sell it. Inventories would likely have to rise further before those with surpluses were willing to take the cut needed to export. At the same time, rising natural gas and NGL prices are another reason to hold on to products as what you have today did not cost that much to make and costs may rise near term. See more in today's daily report.

The US ethylene market strengthened slightly in early July, most likely because of supply disruptions as it is hard to see how domestic demand could improve from here. There is not much room to increase prices further if the export market is the balancing mechanism through July and August, as prices remain depressed in Asia and any arbitrage would close quickly if prices in the US moved any higher. Despite the rising NGL prices discussed in today's daily report and on Sunday, the US has plenty of margin left in ethylene, and prices could go lower if that is necessary to move additional volume. While we talk in the opening paragraph about increased inventories of finished goods in anticipation of the year-end holiday season and continued supply constraints, and how this is leading to a shortage of warehouse space, we suspect that everyone upstream of the finished good suppliers is also looking at adding or maintaining a larger inventory cushion than they have in recent years. We still believe that it is a tough call today as to whether you should sell surplus ethylene or store it as we head into hurricane season in the US.

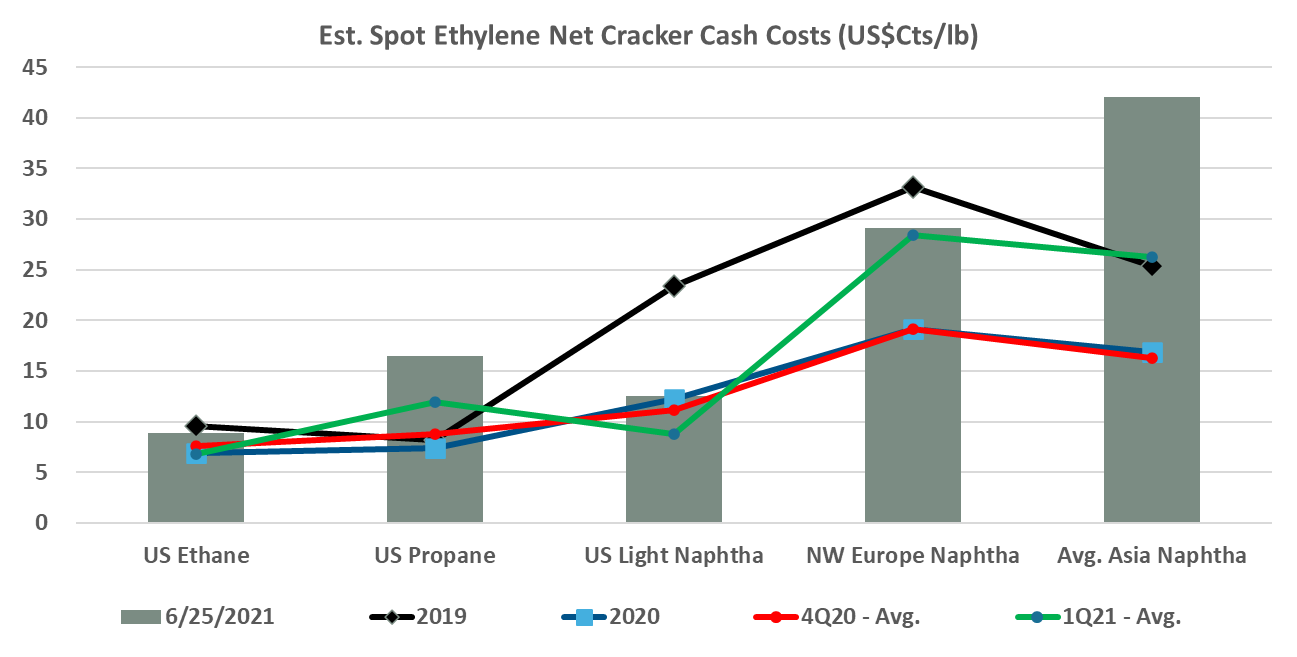

The chart below focus on the ethylene cost curve and show that the US currently retains a distinct cost advantage despite escalating domestic feedstock costs. The current cost advantage in the US is sufficient to move ethylene derivatives into most markets profitably and while US spot prices for ethylene may not quite reflect the levels needed to stimulate exports today – US ethylene costs certainly do. The restart of the Nova unit in Louisiana may put some further downward on US ethylene prices but as we discussed yesterday, given the weather risks in 3Q it is an interesting dilemma today over whether you sell surplus ethylene or store it on the basis that spot prices will rise because of production outages – this time last year the “store it” decision would have been the right one as spot prices rose through 3Q.