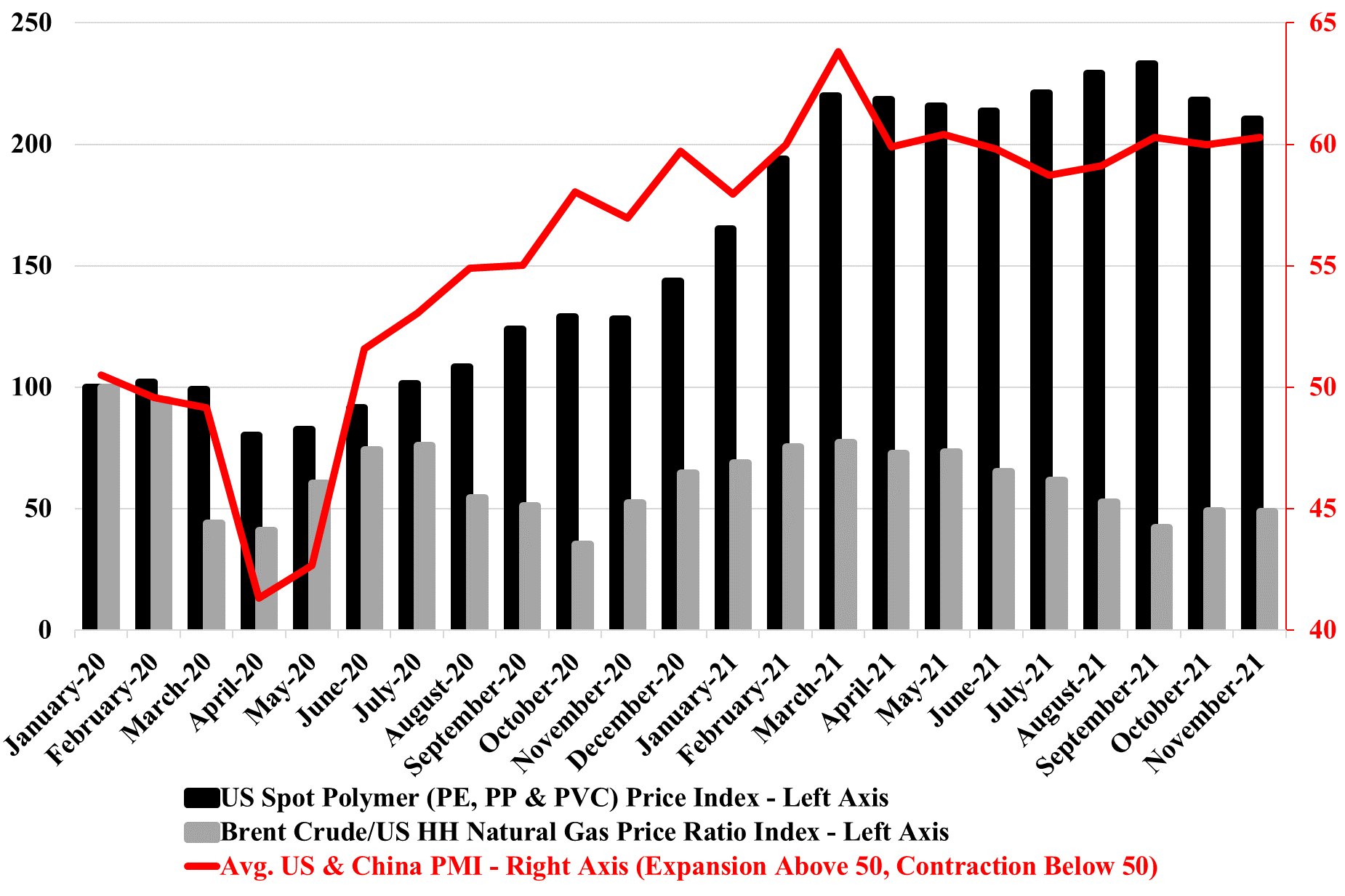

We have been asked a couple of times in the last week how US polymer (polyethylene in particular) pricing can remain so robust in a market where there is an inventory build going on. The PMI numbers are part of the answer. While we may be in the seasonally weaker part of the year, customers are still looking for more material than a year ago, and this makes the “we need a lower price” argument much harder, especially when the memory of 1H 2021 acute shortages is still fresh in the memory and when, more than likely, they are getting signals from their customers of a further step up in demand in 2022. We have done some traveling recently and the incremental demand for packaging polymers is very evident in the travel and leisure business, even if the number of travelers is still down. There is more packaging on airline and airport food and hotels are offering pre-packaged food for breakfast that would previously have not been individually packed. The reasons are obvious – safety and hygiene from the consumers' end and costs from the providers' end, as prepackaged food, can be bought in bulk and more cost-effectively and they likely have a longer shelf life.

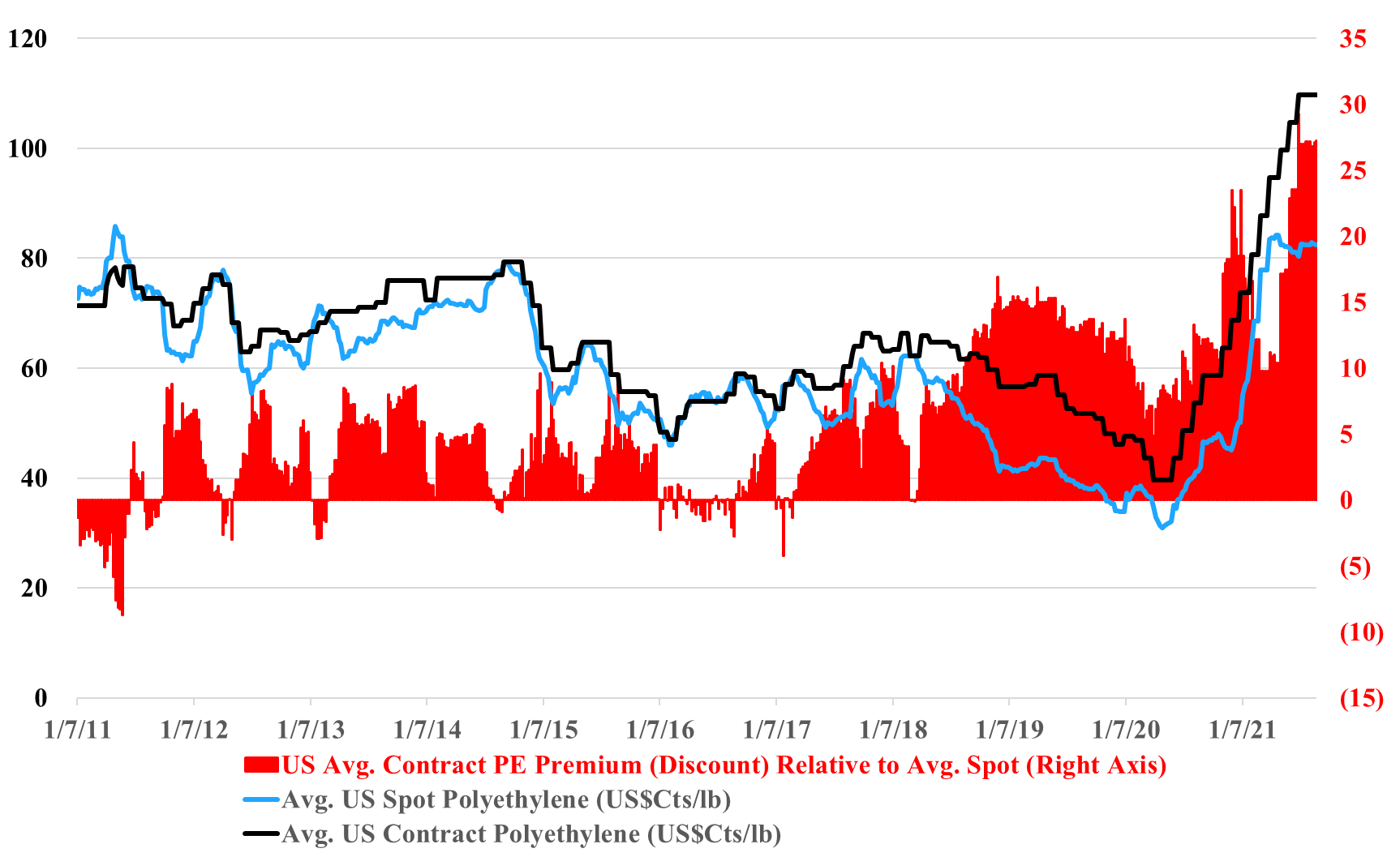

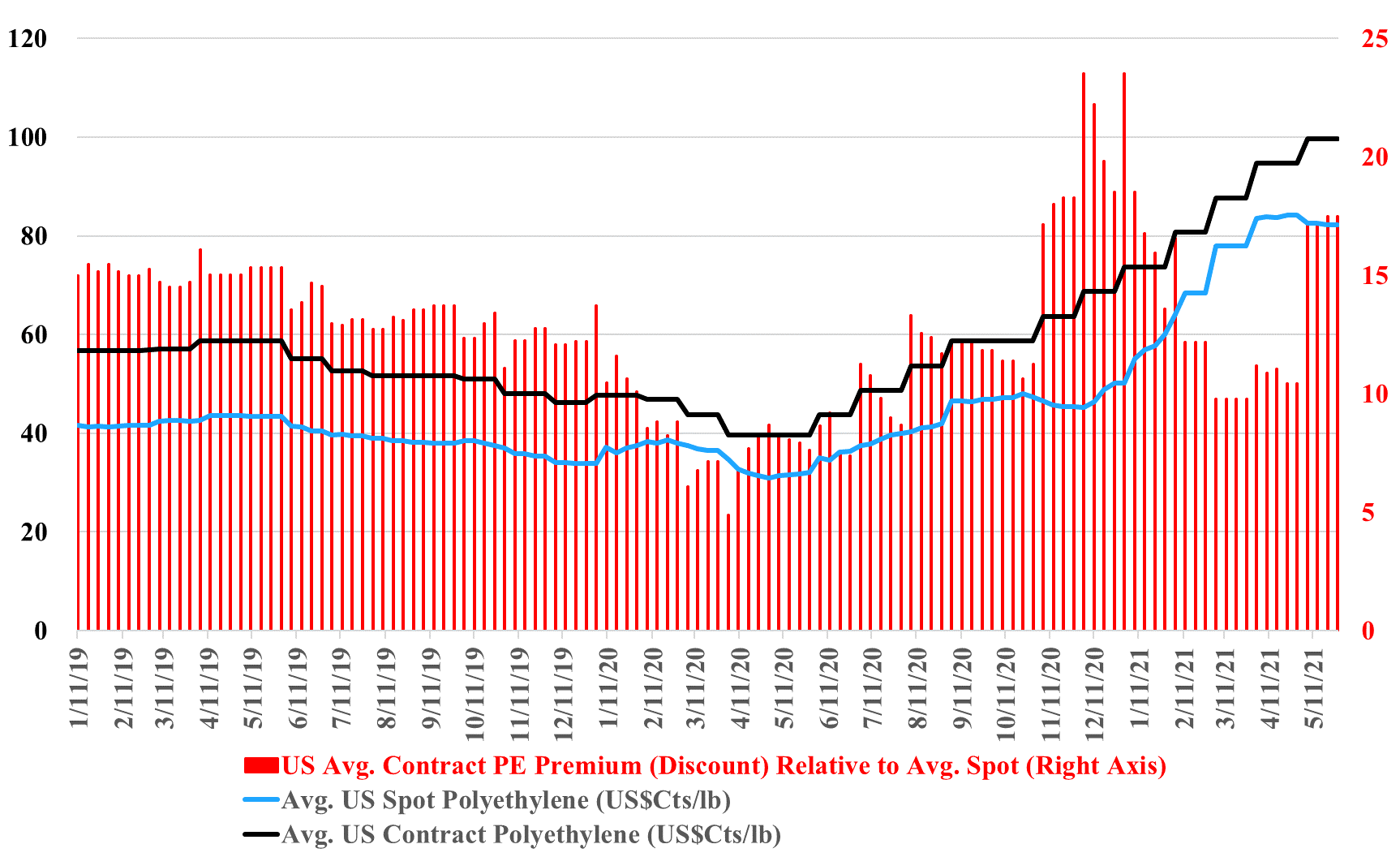

We discuss recent historic highs reached in China to US container freight rates in our daily research today, and (absent Ida) we note that freight charges remain a major component in favor of US polymer price support. With current container rates so high, it is difficult for US consumers to get access to cheaper material from Asia, even if they are willing to try the untested grades in their equipment. Absent the freight extremes today, we would be much more definitive in declaring that the US's record spot/contract polyethylene price difference was unsustainable and would be corrected quickly. While there appear to be some surpluses of US polyethylene today, such that producers are testing the incremental export market, the same producers can hide behind the freight barrier as they make arguments to support domestic pricing. Some US buyers may be getting pricing relief because they have price mechanisms that partly reflect the spot price. It is also possible that large buyer discounts have risen through this period of very high pricing (this has happened before).

While we continue to see valiant efforts from the polyethylene producers to increase prices further in June, this is what we used to refer to as a “cow in front of a train” strategy. In that throwing a cow in front of a train was not going to stop it, but it might slow it down a bit! Barring weather, it is inevitable that US polyethylene prices shown in the chart below will start to give back some of their premium pricing over the coming months. One factor among several others pointed out on today's Daily Report is that Ethylene is much weaker and the international markets are materially out of line, and if freight rates have peaked, the arbitrage will undermine prices in the US. Producers will do their best to hang on to the high margins for as long as they can, and a few more cows may be sacrificed, but the weather is their only hope.