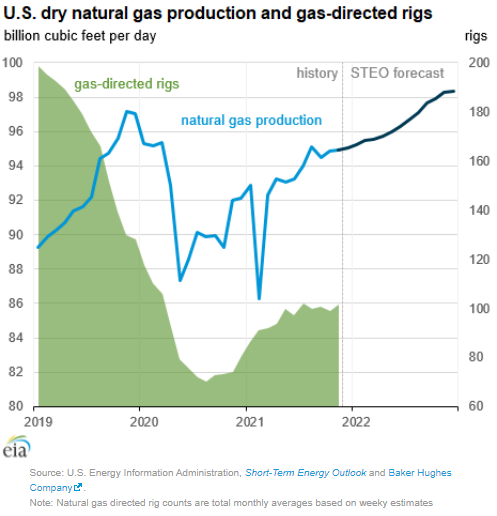

The theme of our Sunday report (to be found here) will be inflation this week and the signs that we are seeing across multiple industries which suggest it could be more problematic and worsen in 2022. One of the focuses is energy and how the pressures to be seen as good citizens is lowering investment in oil and natural gas production, while the world is not far enough advanced on energy transition to be able to substitute for the missing hydrocarbons. We would agree with many of the recent comments from some segments of congress, which is that the answer is not to curtail exports of LNG and crude, as by doing so we will starve the rest of the world of hydrocarbons and create worse shortages than Europe and China are seeing today. The better solution would be to support “clean” US production of the lowest emission fuels possible – especially for natural gas. As we have noted in prior research, with a global solutions hat on, the relatively low costs of natural gas F&D costs in the US, when combined with what we expect to be relatively low costs of emission abatement in the US, should drive more investment in the US, creating jobs and export income.

At this point, it has stopped being a story about how transient higher energy prices might be and instead become a story of how high could they go as well as how long the higher prices could last. With sentiment easing in the US because of an expected milder October, we also have the headline of the restart of Cove Point LNG, which should add to natural gas demand. The EIA, in the chart below, shows US prices peaking through the end of the year before falling again in early 2022. There remains an expectation that the rest of the world will be short of LNG and so we will either see the US natural gas competitive advantage remain strong, or the US LNG facilities will stretch their underutilized nameplate capacity and this could be supportive of higher US natural gas prices. New LNG capacity does not hit until late 2022 and how much is exported until them will be a function of the throughput of the existing terminals – which today look like they were very prudent investments.