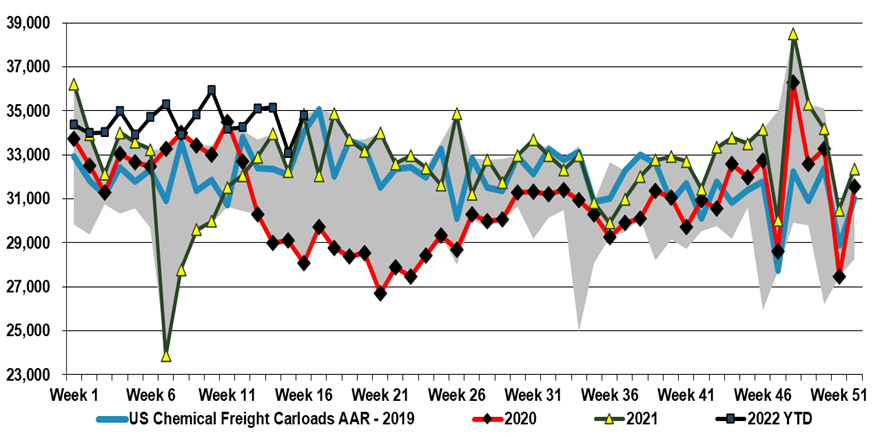

Chemical railcar volumes remain very strong in the US, despite some issues with exporting polymers, which has led to inventory builds on the coast, especially the Gulf Coast, and despite the implied consumer volume purchase decline in 1Q GDP estimates (sales grew but prices rose 500 basis points more than sales growth – suggesting an equivalent decline in volumes). As we noted yesterday, some companies closer to the consumer are indicating demand weakness and are more cautious about 2Q outlooks. If a higher than usual proportion of rail freight is moving into inventory, either at customers or stuck in rail cars – something Union Pacific has signaled – we could see a correction.

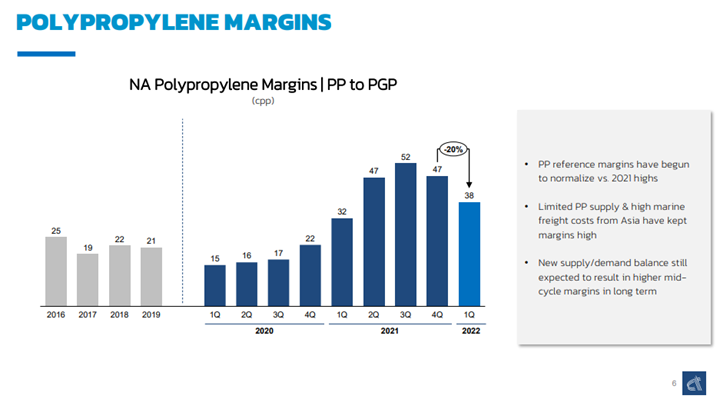

While Alpek shows a decline in the polypropylene to propylene spread in the exhibit below, it is important to note how high margins remain in the US. It is also important to note that the company points to high freight costs from Asia as one of the key drivers. China has significant polypropylene surpluses, and the price delta with the US is very high and, on paper, looks high enough to encourage imports into the US. But it is not that simple. The freight rates for containers from Asia are just one of many roadblocks, including wait time – on the water and the docks – and product quality. A US converter will likely not risk buying a few spot containers from China if focused on a product spec for a US customer. One way to get more material into the US would be for the end-user to buy the product – durable manufacturer or packager – and then ask its supplier to effectively toll-process. That way the product quality and logistic risk sit with the end consumer rather than the converter in the middle. The longer US domestic polypropylene prices remain inflated versus Asia, the more end-users may look at this option.

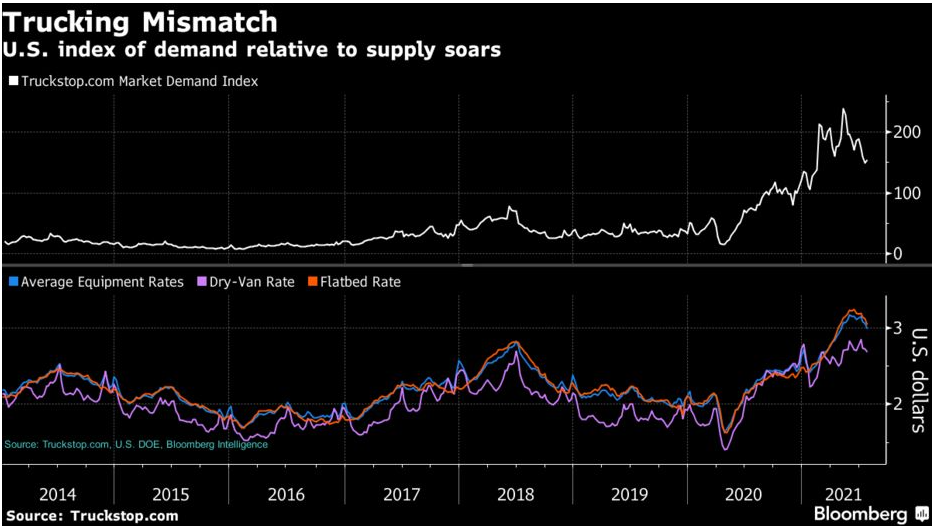

Our Sunday thematic and weekly recap report covers how the US is short of truck drivers (60,000) during a period when freight is struggling to move from congested ports – holiday buying will add more stress. This matters because we have record shipments of containers on the docks at US ports and record shipping backlogs waiting to unload as well as well documented shortages of durables in warehouses and at retailers.

The image below shows the mismatch in driver availability and trucking rates:

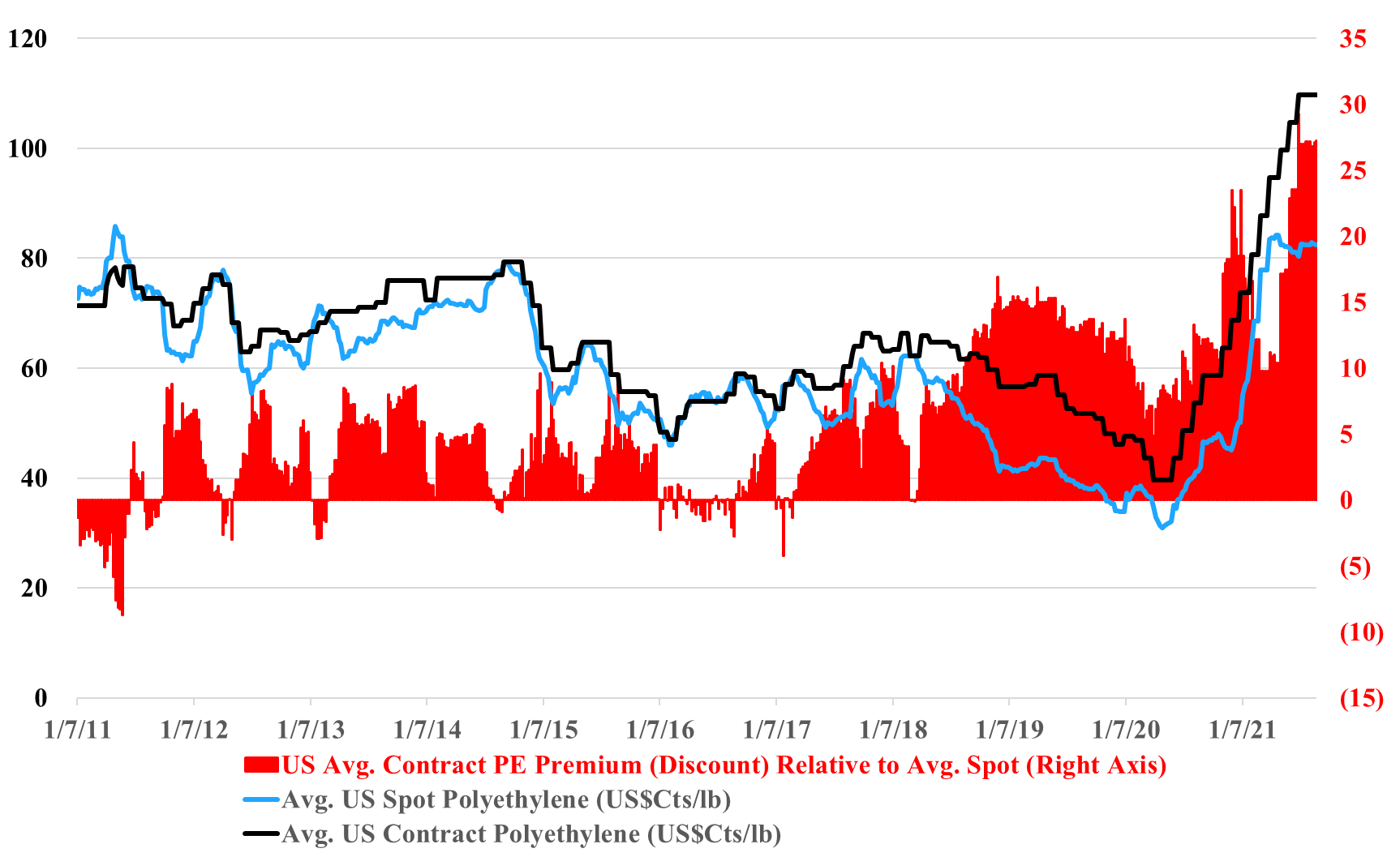

We discuss recent historic highs reached in China to US container freight rates in our daily research today, and (absent Ida) we note that freight charges remain a major component in favor of US polymer price support. With current container rates so high, it is difficult for US consumers to get access to cheaper material from Asia, even if they are willing to try the untested grades in their equipment. Absent the freight extremes today, we would be much more definitive in declaring that the US's record spot/contract polyethylene price difference was unsustainable and would be corrected quickly. While there appear to be some surpluses of US polyethylene today, such that producers are testing the incremental export market, the same producers can hide behind the freight barrier as they make arguments to support domestic pricing. Some US buyers may be getting pricing relief because they have price mechanisms that partly reflect the spot price. It is also possible that large buyer discounts have risen through this period of very high pricing (this has happened before).

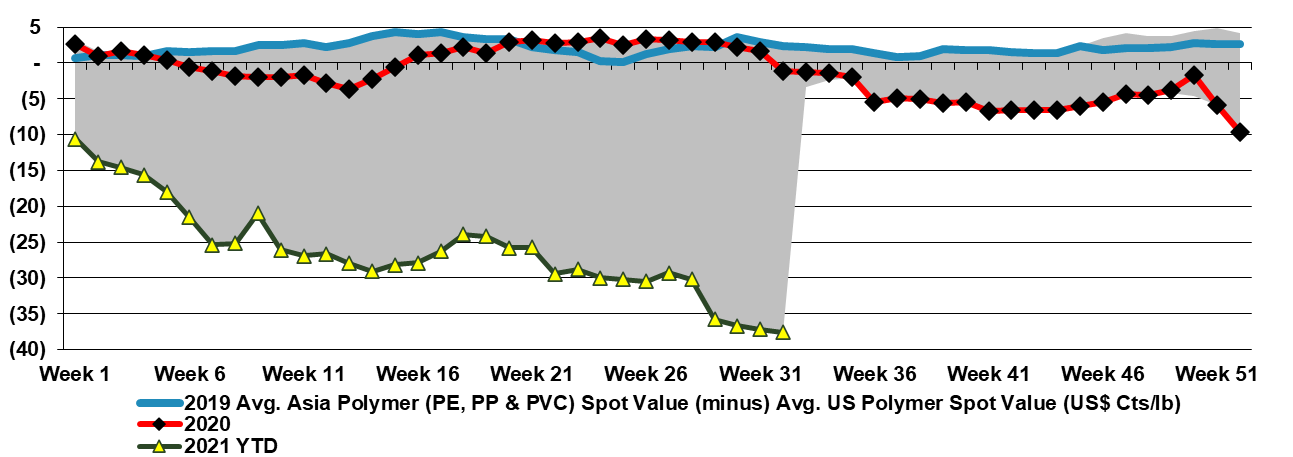

The regional polymer price chart below shows the extreme divergence of prices between the US and Asia, and it has hit a level that has never been reached before. It is in part a function of the wave of new capacity that hit China in 2H 2020 and 1H 2021, which spurred oversupply in some chains, and the dysfunctional global trade backdrop that has kept global supply chains out of balance. As we noted earlier this week, the container costs alone to move polymers from Asia to the US are, best case, 34 cents per pound today, and this is estimate does not include the cost of moving the product to a port in China or from one in the US and also does not include a working capital charge for the time in transit. There would need to be an arbitrage of 10-15 cents a pound above this to make product movements between these regions worthwhile, assuming you can find a buyer in the US willing to experiment with imported products. The other trade impact is that US retailers and manufacturers are pulling on their US suppliers to maximize supply, pushing domestic demand for polymers above trend. The lumber price moves in the US – Exhibit 1 in today's daily report – if they spur incremental home building, it will be another boost for domestic PVC demand.

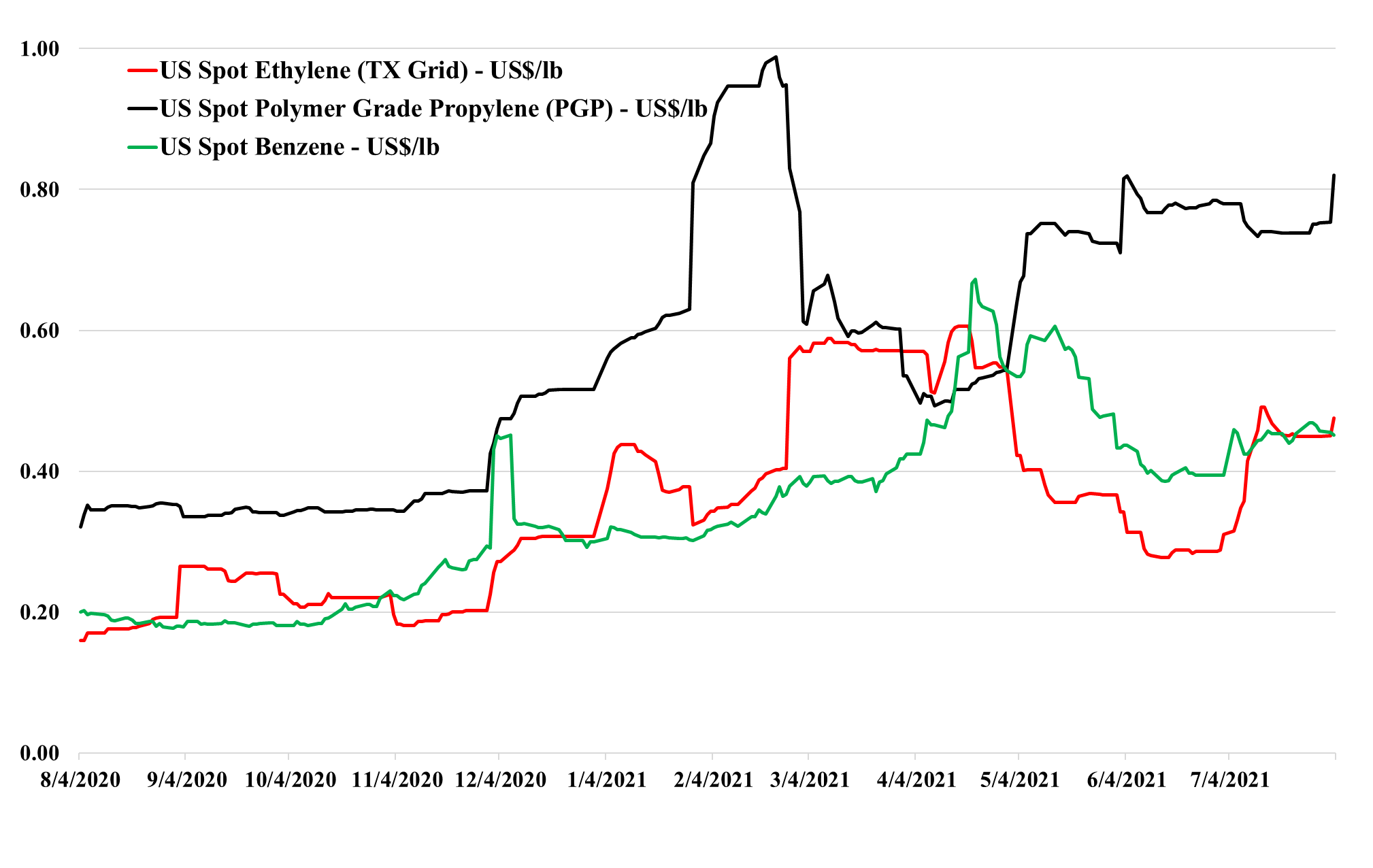

If this commodity cycle has the same drivers as prior cycles, producers like LyondellBasell and others will make comments like “stronger of longer” until prices turn, and if history is any guide, that turn will catch everyone by surprise, and even if it does not, there is no upside for any producer in predicting its end. As with all commodities, markets are tight until they are not, and markets are long until they are not. If you look at the ethylene and propylene price movements in the exhibit below you can see the speed of change that is possible and while the slope may be less severe for polymers in both directions, it can still be abrupt. The worst-case for the US industry would be a step down in demand coincident with the rising natural gas trend. There is no evidence of demand weakness today, but there will not be until it is happening. The extraordinary incremental freight rates shown in Exhibit 1 of today's daily report, make it increasingly unlikely that anyone sitting on surplus polyethylene or polypropylene in Asia can exploit the regional price difference. When demand and sentiment around supply chains turn, we would expect this spot shipping rate to collapse also – but there is no sign of that today.

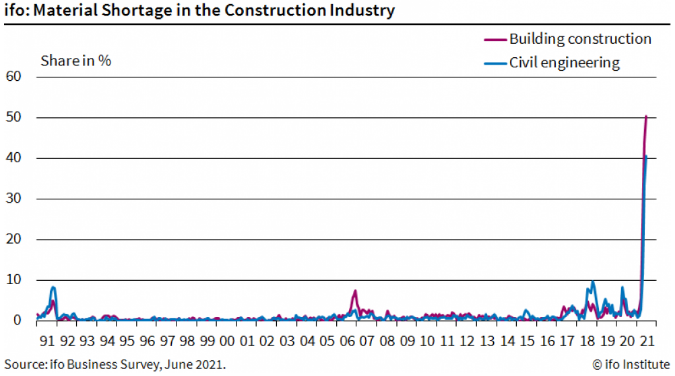

The German materials shortage chart below is certainly eye-catching. There is nothing even remotely close in 30 years of history. We see this as further confirmation that we should continue to expect high shipping rates and congested ports until surveys like this show significantly better results and it is also further supportive of inflation. While it is extremely difficult to forecast from here, we would use the pendulum or spring metaphor – the further you pull either in one direction, the further they swing or spring back. The current dislocation is so extreme that everyone in the chain is likely acting instinctively and working to find greater supply and greater supply security. At some point, both end-demand and demand to fill inventories will normalize – either back to trend or back to a higher trend, but the inventory build piece will end and we will either get a gradual retreat in the scary data – such as the spike in the chart below – or we will see an equally quick collapse, at which point pricing will likely take a hit down the chain, with basic chemicals particularly vulnerable because the world has been adding substantial new capacity over the last several years in the US and China. More investment may be needed to keep up with higher trend demand in many intermediate or end-products that consume base chemicals and this could keep pricing supported, but basic chemicals and polymers look especially vulnerable to a reversal in the supply chain build we have seen for the last 9 months. For more see today's daily report.

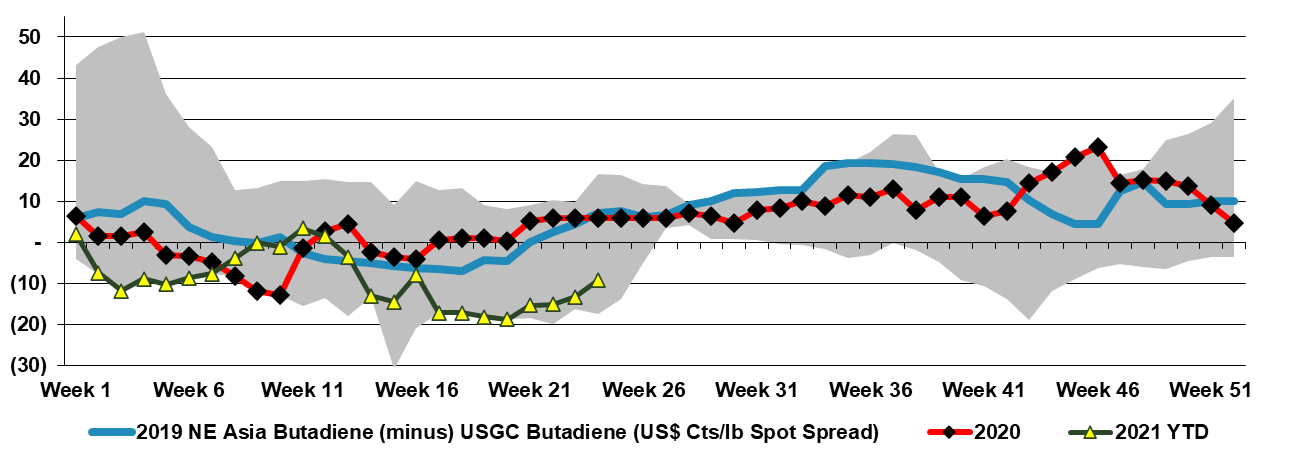

The exhibit below looks at the difference between a strong butadiene market in the US and a much weaker one in Asia. The strength in the US is a function of the stronger US economy and consumer spending as well as logistic issues with products containing butadiene derivatives, but also because there is no incentive to increase heavier cracker feedstock use right now in the US and consequently co-product butadiene supply remains constrained.

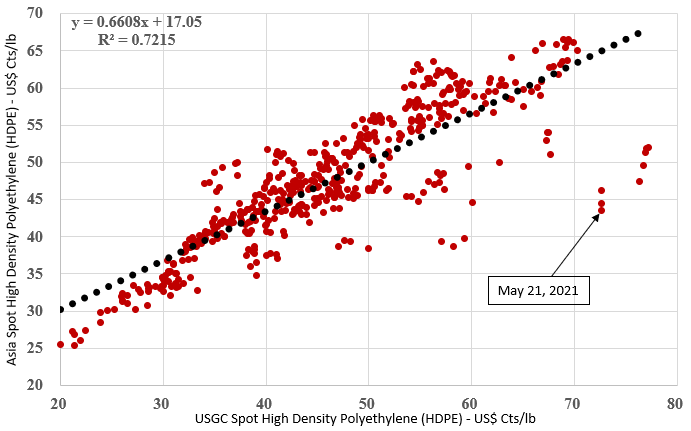

Scatter charts with significant outlying points are always eye-catching and the exhibit below is no exception. The extremes of the chart are interesting as they show that when US polymer prices are low, Asia generally trades at a premium, and when US prices are high Asia trades at a discount. But today’s discount is several standard deviations from the norm, and it is too compelling a trade to ignore. If the US was short polyethylene we would be less focused on this arbitrage but that is not the case. Unilateral decisions from US producers to keep production in line with contract demand could maintain pricing support, but the competitive disadvantage that this places on US consumers – especially in durable applications (where the polymer is a larger part of the finished product cost) is significant. It is also a major cost headwind for the packaging companies in the US, and tough to pass through in most cases on staples and household products, because of the buying power of the major food and drug retailers.