The Lanxess guidance below is likely the right way to go for now. The medium-term effects of the Russia/Ukraine crisis are unknowable today and all companies can monitor is the immediate impact on their businesses. Most had entered 2022 seeing very strong demand growth and the promise of a much better year as COVID restrictions were lifted and economic activity picked up generally. Now all bets are off, as it is not just the primary impacts that matter – such as a companies’ direct exposure to Russia or Ukraine – note McDonald's is suggesting that pulling out of Russia will cost the company $50 million a month, for example – but also the secondary impacts of what the conflict is doing for supply-chains and pricing. Higher hydrocarbon pricing in Europe, for example, will impact the economics of all production, not just the products sold to Russia or Ukraine. There will also be some demand adjustments directly related to the conflict – disaster relief for example – more PPE – more spending on defense and defense-related materials – DuPont’s kevlar business should be seeing a benefit for example.

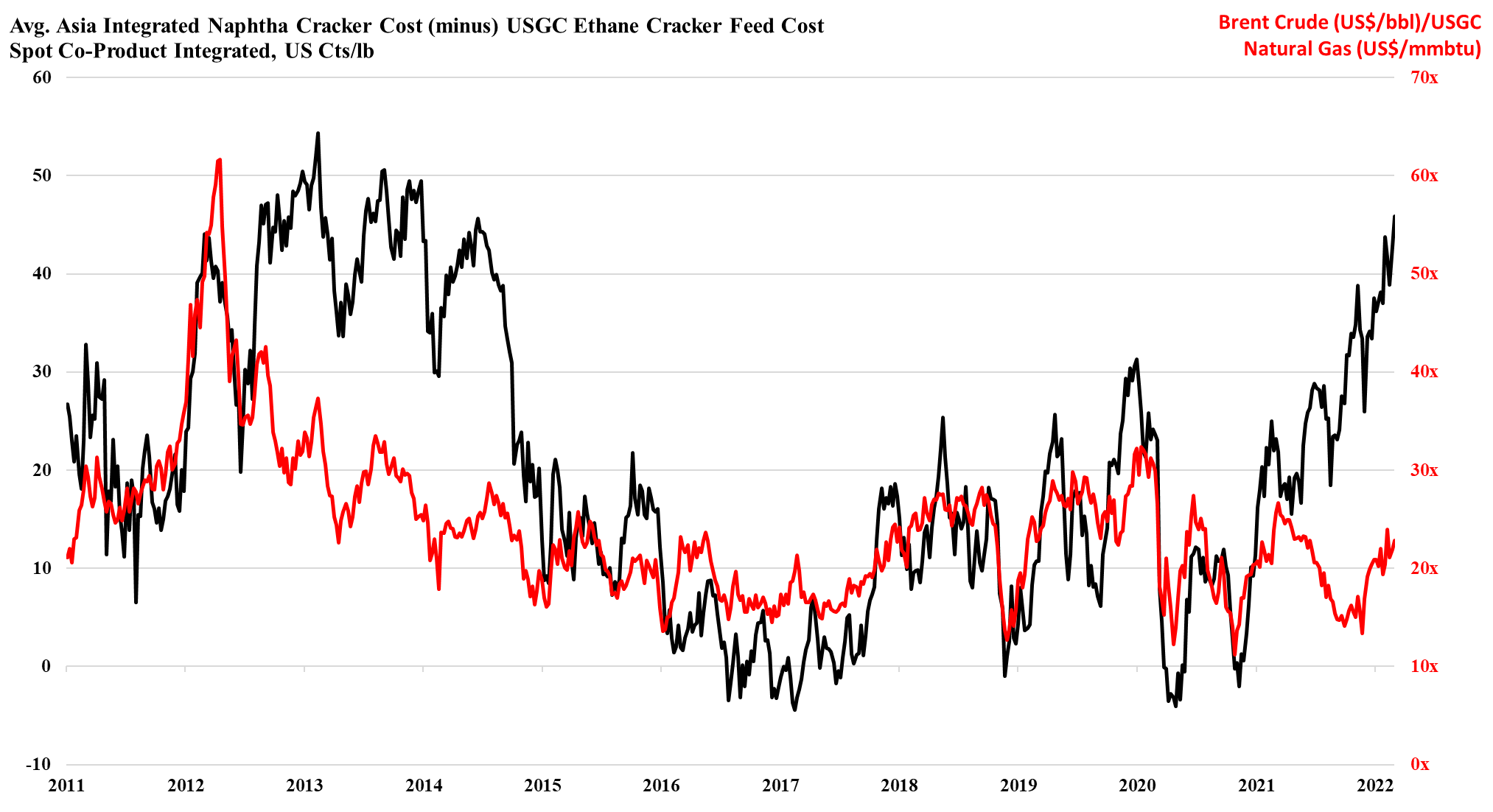

As the ratio of pricing between Brent crude and US natural gas rises, the US ethylene cost advantage is spiking, and as long as the US is producing enough natural gas to feed domestic demand and allow the LNG facilities to run at capacity, the advantage can remain. This gives the US a significant cost advantage and assuming that there is spare capacity the US industry can step up and support Europe if needed. However, it is not clear that there is much spare capacity, either in the production units or in the logistics to get the product to ports or across the Atlantic. There is a surplus of liquid and gas carriers today, but the container problems are global and the inflation and supply chain issues that we seem to be stuck with are likely to keep containers tied up in excess inventory that consumers will want to keep building as a cushion for a less certain supply outlook. The shipping issues are only part of the problem for Asia, as even with better opportunities to export, the region is seeing escalating production costs because of the movement in crude oil and naphtha pricing. We are in an unusual position where strong demand in the US is keeping domestic prices higher than in Asia, despite costs in the US that are low enough, especially for polyethylene to move material to Asia at costs well below the cost of manufacture in Asia. This dynamic can last for a lot longer in our view as long as oil prices remain elevated versus US natural gas. An abrupt turn will occur if US natural gas production falls below domestic demand and LNG demand – this would cause a spike in US natural gas prices. For more see today's daily report.

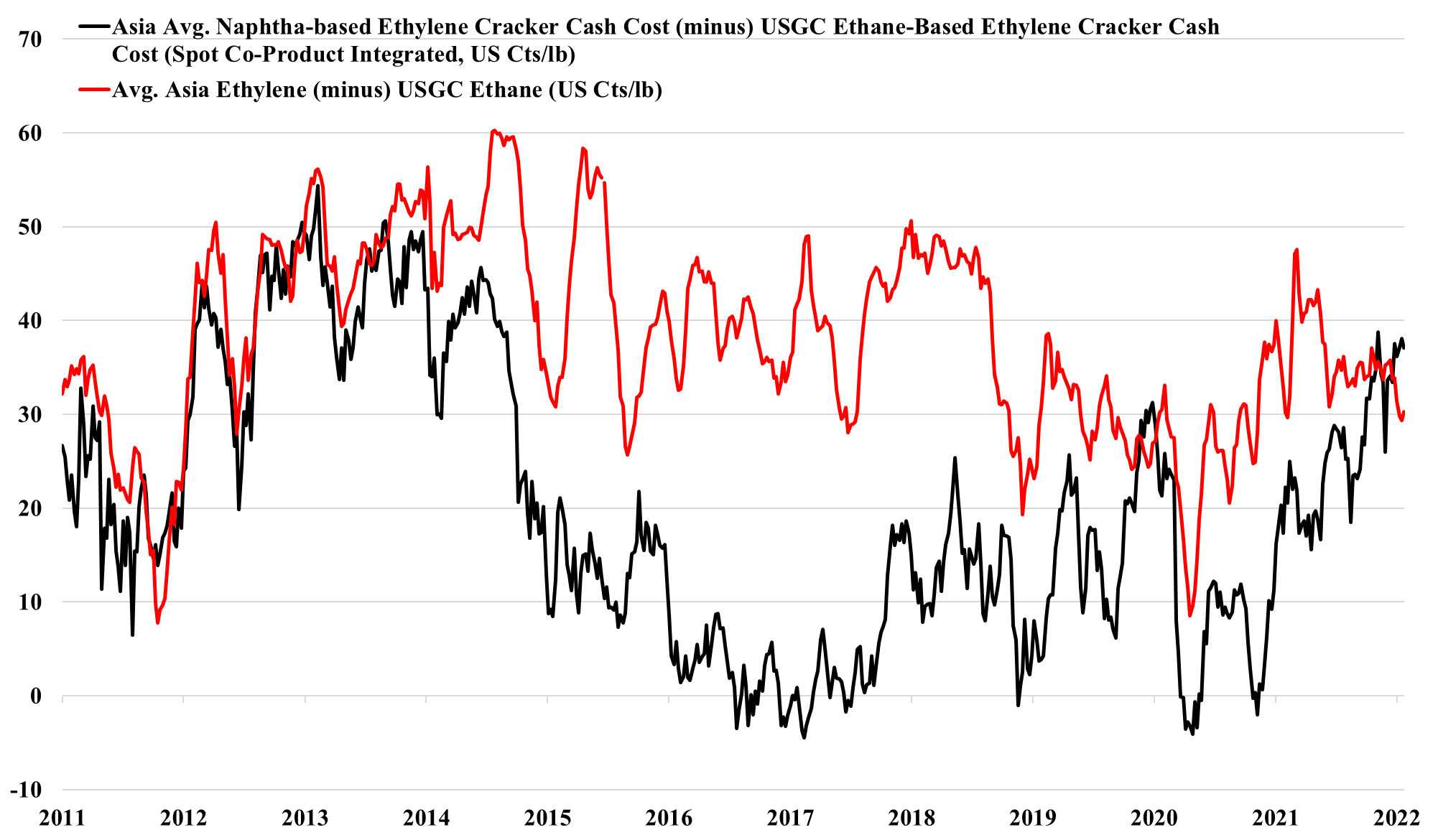

2022 has started very strongly for US chemical and polymer producers, in part because demand growth remains very robust based on early reads from those that have reported earnings, and in part because of the ever-increasing competitive edge that the US is enjoying over Asia – see exhibit below. US producers can maintain strong margins in the US, while easily pushing any surpluses into export markets where local suppliers cannot compete. At the same time, higher production costs and very high logistic costs make it almost impossible for those regions with capacity surpluses to move products into the US, and it is challenging also to move products into Europe. If this production and logistic cost environment persist, not only should US prices stabilize, but for select companies – those with a strong US production bias – we should see estimates for 2022 start to rise.