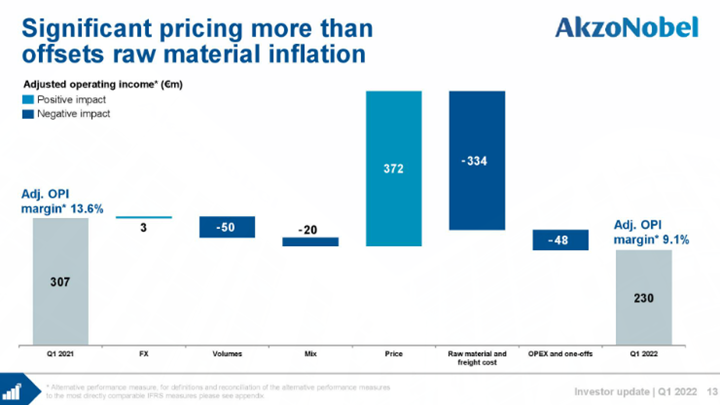

We have discussed in several recent reports the very mixed fortunes in the intermediate and specialty chemical sector related to whether companies have been able to move prices fast enough to cover costs. The two large blue bars in the AkzoNobel chart below show that Akzo was close, but did not make it. We expect other examples like this over the coming weeks but we also expect some companies to have done better – some of this depends on mix and contract terms, but a lot has to do with how early you acted on the rising cost trend and how aggressive you were willing to be with customers. Dow is another example of a company struggling to get pricing high enough to cover cost increases, although Dow and others have aggressive price increase announcements in the market for polyethylene for April and May that would make a significant difference to US margins if successful.

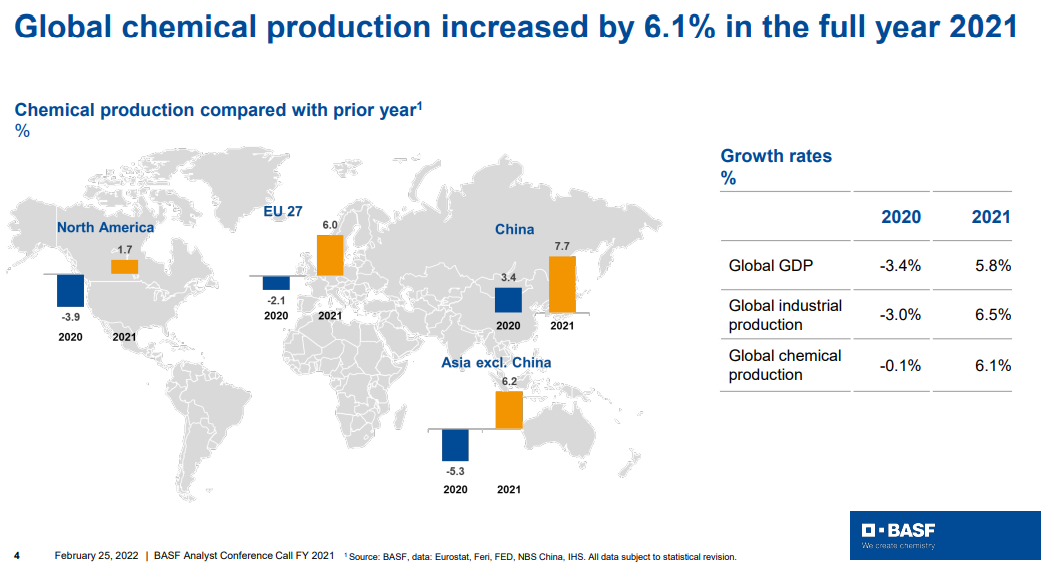

Fear of shortages is the one factor that is most supportive in terms of helping to push through pricing and the events in Europe and their associated impact on energy prices should be all the support that the chemical and polymer industry needs to push pricing through that will cover cost inflation. Buyers of raw materials and intermediate products will naturally look to buy a little more than they need in the near term, both to ensure that they get something ad to try to build a bigger inventory cushion. This will have the effect of pushing apparent demand higher, making the pricing initiatives easier. Few will push back on pricing if their primary concern is availability. Looking at the BASF results summarized in the chart below, demand is already very robust and this will lead to higher utilization rates and higher volumes for chemical producers as well as high pricing. The commodity producers are likely more interesting here as they can move prices much more quickly than the specialty companies who might see margins squeezed over the next couple of months. None of this is good for inflation. See more in today's daily report.

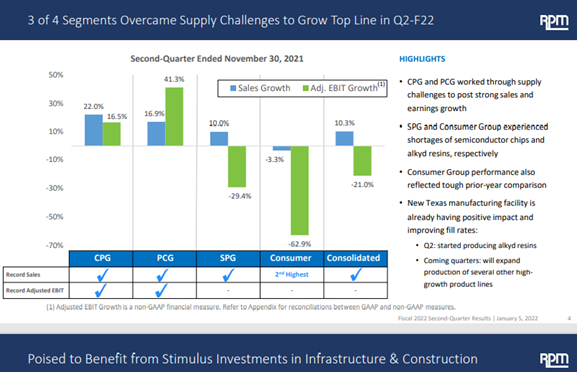

Following on again with our inflation theme, which features heavily in today's Daily Report, note that RPM’s release is riddled with references to inflation impacting results negatively as raw material and logistic costs increased. The commodity chemical and polymer producers have much more pricing flexibility than the specialty makers like RPM, and they can generally pass through higher costs quite quickly. For the specialty companies, there is generally a lag, as is clearly shown in RPM’s results, but they generally catch up with pricing as long as demand is robust, which it appears to be. The benefit for the specialty companies is that they can often hold on to price increases or at least some of the increase longer than a commodity producer can as raw materials and fundamentals ease. We expect the intermediate and specialty chemical producers in the US and Europe to have strong demand growth in 2022, as the reshoring momentum should continue and offset any risk of weaker consumer spending on durables as the year progresses. We have been more focused on companies that are selling materials into construction and renewable energy and EV markets, but RPM has enough exposure that it should also be a beneficiary as long as prices can keep pace with costs.