The US chemical rail volumes should be considered in the context of some of the slowing demand that has been indicated by companies downstream of chemicals, and we see this as further evidence for possible inventory build through the chain. Earlier in the year these builds would have been justified by supply chain issues that have plagued all segments of retail and manufacturing for close to two years, but today we should be at or above inventory comfort levels. We are calling for weakness in demand and some margin erosion in US chemicals and polymers in 2H 2022, before a strong rebound as early as 2024, but if buyers of polymers and chemicals and their customers look to reduce inventories more quickly, the landscape could change quickly. While this is possible, with the threat of higher energy prices very real, we would be surprised in anyone was interesting in dramatically lowering inventories today.

More earnings releases and more discussions of disruptions and higher costs! One thing that is clear from all the reports we have followed, whether from basic chemical companies or those downstream, is that no one has any expectation that the supply disruptions and inflationary drivers are going to end soon. In our Sunday Thematic, we talked about the possibility of demand remaining robust and possibly absorbing new supply in 2022 because of further inventory builds. The idea is that holding more working capital, while possibly less efficient financially, may be more prudent from a business continuity perspective, especially given the reputational risk of failing to fulfill customer orders. While there is appropriate concern that interest rates could rise significantly, lending rates are so low that the cost of holding more inventory would be immaterial for many companies. For many products in the chemical chains and across materials more broadly, global oversupply, where it exists, is not high, and a further upward swing in inventories in 2022 could easily keep tight markets tight and swing some more balanced markets to shortages.

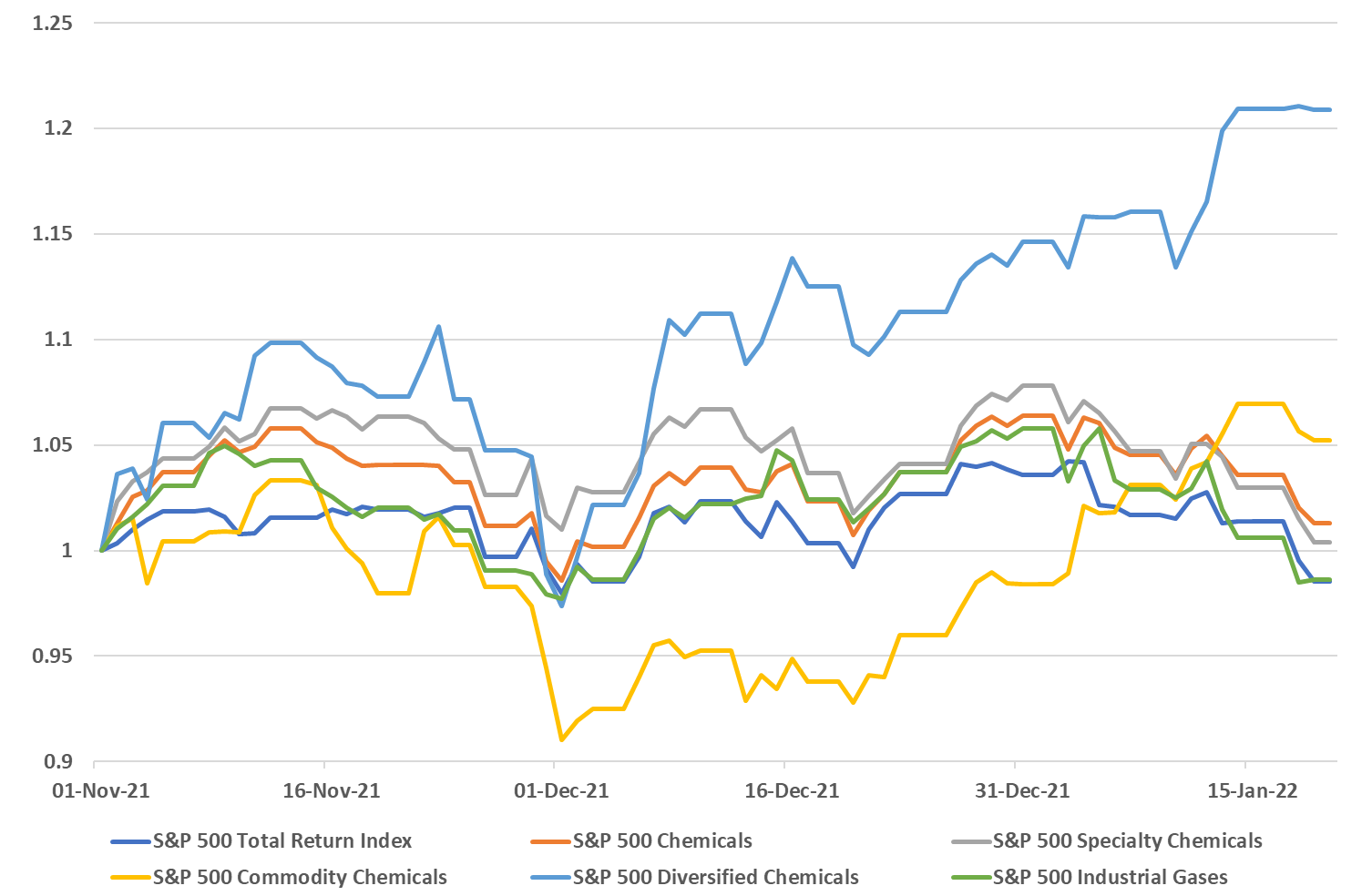

Following on from the core theme of today's daily report, demand could provide the lifeline that the US chemical industry needs to get through what looks like a potentially oversupplied 2022 – note the successful start-up of the ExxonMobil/SABIC facility in Texas, announced today. While we still think that the US market will be looser in 2022 than in 2021, barring any above-trend weather events, strong demand growth could offer some pricing protection for the industry – especially given the input inflationary pressures that we are seeing. If the customer base is looking for increases in deliveries, which we expect to be the case in 2022, it will be easier to defend pricing and gain pricing where costs are higher. Some of the momentum that we are seeing in the commodity stocks year to date is a function of a broader inflation trade, but some is likely in anticipation that 2022 will not be as bad as had been expected and on that basis, the sector looks particularly inexpensive – even today after the early year rally. It will be a little harder for the specialty and intermediate companies depending on how long they have to play a lagging catch-up game with costs. But if, and when, costs peak, they should see margin expansion as costs fall and will be able to keep some of the gains, especially if their demand is also growing.

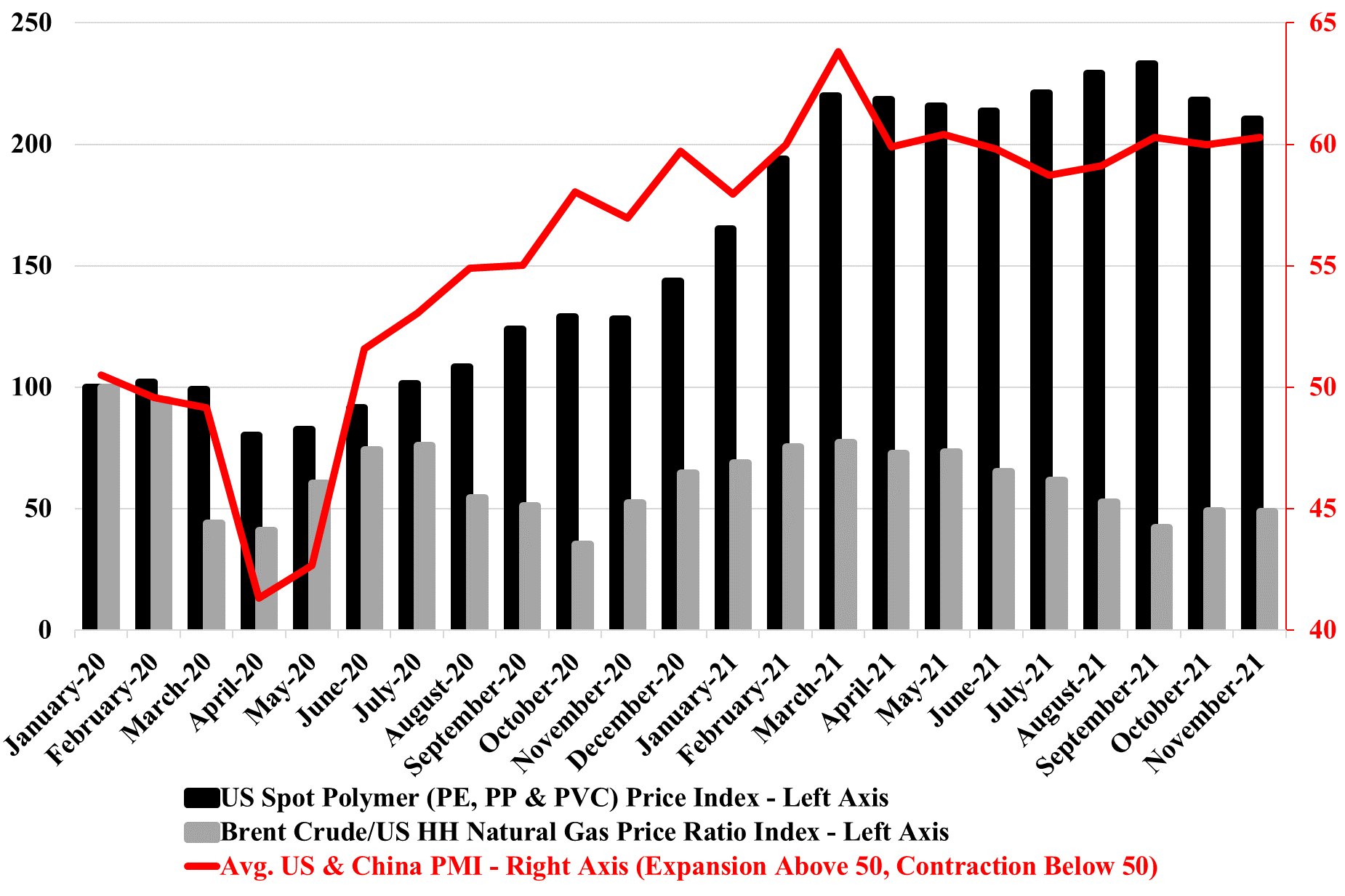

We have been asked a couple of times in the last week how US polymer (polyethylene in particular) pricing can remain so robust in a market where there is an inventory build going on. The PMI numbers are part of the answer. While we may be in the seasonally weaker part of the year, customers are still looking for more material than a year ago, and this makes the “we need a lower price” argument much harder, especially when the memory of 1H 2021 acute shortages is still fresh in the memory and when, more than likely, they are getting signals from their customers of a further step up in demand in 2022. We have done some traveling recently and the incremental demand for packaging polymers is very evident in the travel and leisure business, even if the number of travelers is still down. There is more packaging on airline and airport food and hotels are offering pre-packaged food for breakfast that would previously have not been individually packed. The reasons are obvious – safety and hygiene from the consumers' end and costs from the providers' end, as prepackaged food, can be bought in bulk and more cost-effectively and they likely have a longer shelf life.

The decline in US and global chemical pricing this week (as discussed in today's daily) is a function of oversupply in the US and lower costs in the rest of the world. The US has had an incentive to produce everything for most of the year and has had essentially full capacity to do so since the beginning of the 4th quarter. This will have collided with seasonally weaker incremental demand in December and the recent abrupt drop in oil and gas prices to swing momentum very much in favor of buyers. Polymer prices have to date been more stubborn in the US, but we expect continued weakness here also through the end of the year.

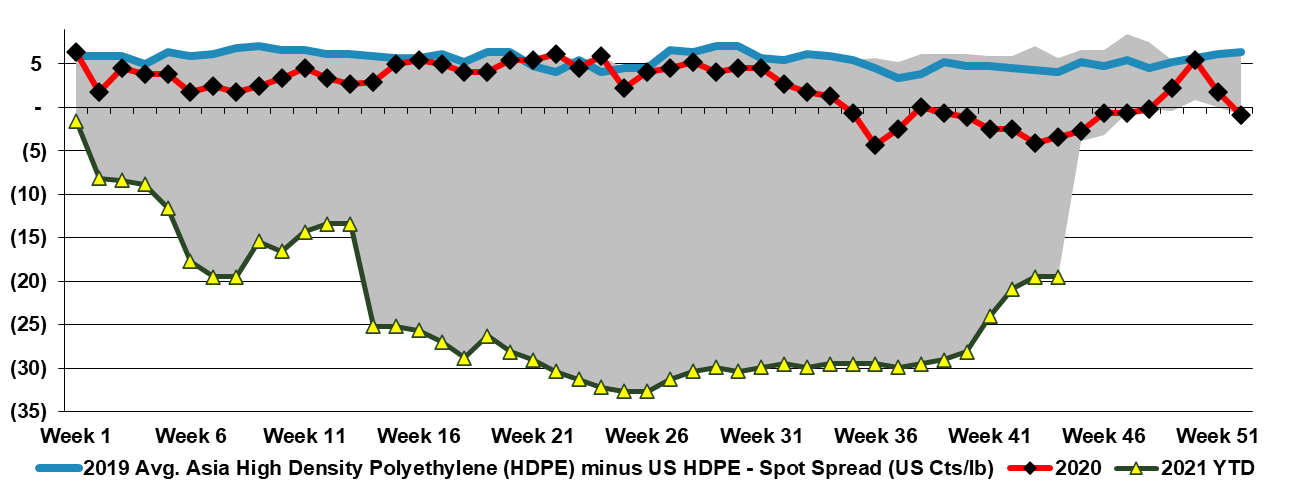

While we are beginning to see some easing in US polyolefin prices we note in today's daily that prices are not falling in step with monomers and so spreads are widening. Because of the very integrated nature of the polyethylene market, we see swings in where the margin is being captured based on relative tightness and today it is squarely biased towards polyethylene in the US. Despite the polymer price declines in the US we maintain a level of pricing that is well above Asia – Exhibit below, but not high enough to attract imports, given the high container rates and the long lead times on shipping. The same is not true for polypropylene, which maintains a spread versus Asia that can cover the very high current costs of transport (bottom exhibit).