More earnings releases and more discussions of disruptions and higher costs! One thing that is clear from all the reports we have followed, whether from basic chemical companies or those downstream, is that no one has any expectation that the supply disruptions and inflationary drivers are going to end soon. In our Sunday Thematic, we talked about the possibility of demand remaining robust and possibly absorbing new supply in 2022 because of further inventory builds. The idea is that holding more working capital, while possibly less efficient financially, may be more prudent from a business continuity perspective, especially given the reputational risk of failing to fulfill customer orders. While there is appropriate concern that interest rates could rise significantly, lending rates are so low that the cost of holding more inventory would be immaterial for many companies. For many products in the chemical chains and across materials more broadly, global oversupply, where it exists, is not high, and a further upward swing in inventories in 2022 could easily keep tight markets tight and swing some more balanced markets to shortages.

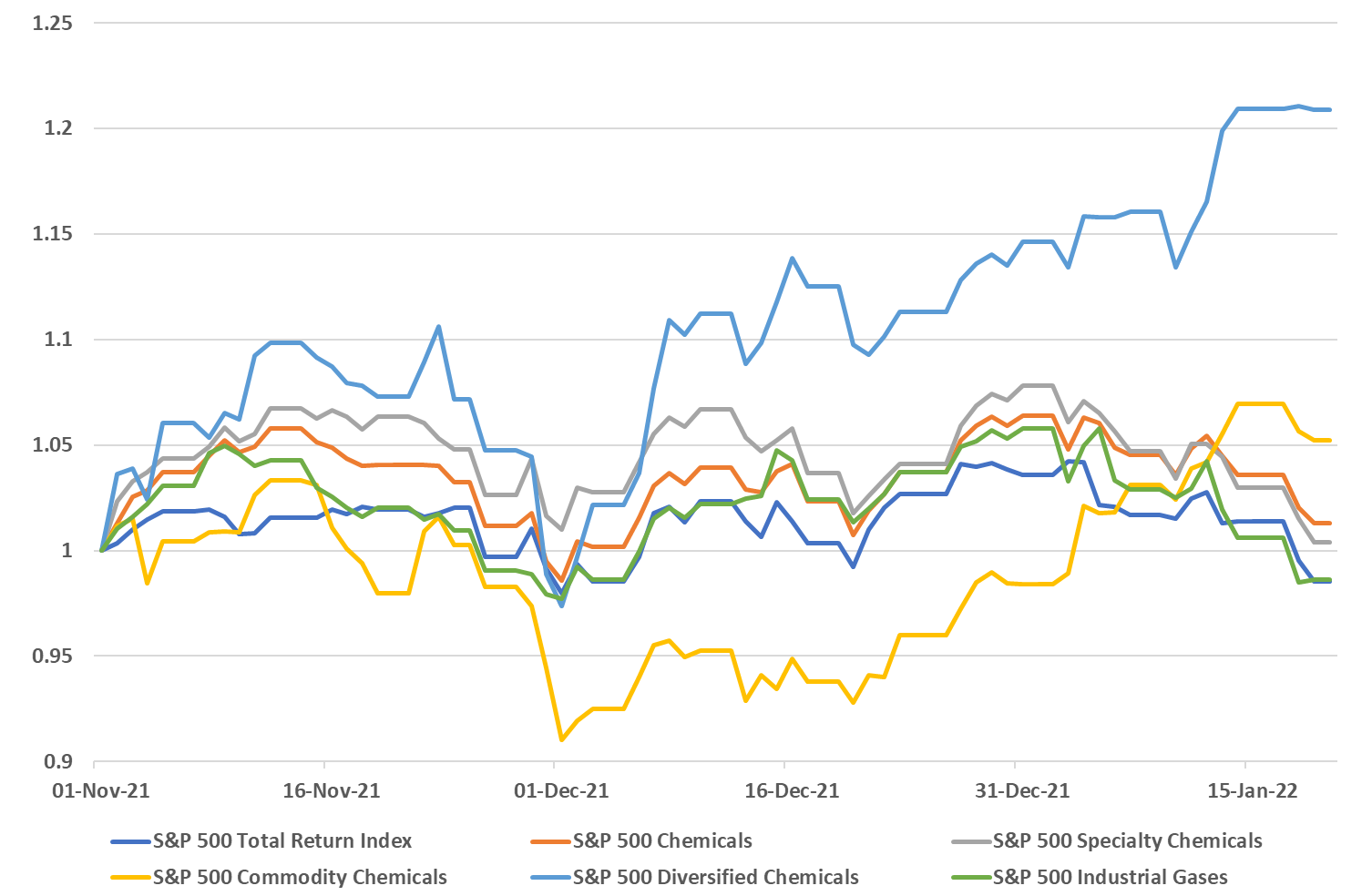

Following on from the core theme of today's daily report, demand could provide the lifeline that the US chemical industry needs to get through what looks like a potentially oversupplied 2022 – note the successful start-up of the ExxonMobil/SABIC facility in Texas, announced today. While we still think that the US market will be looser in 2022 than in 2021, barring any above-trend weather events, strong demand growth could offer some pricing protection for the industry – especially given the input inflationary pressures that we are seeing. If the customer base is looking for increases in deliveries, which we expect to be the case in 2022, it will be easier to defend pricing and gain pricing where costs are higher. Some of the momentum that we are seeing in the commodity stocks year to date is a function of a broader inflation trade, but some is likely in anticipation that 2022 will not be as bad as had been expected and on that basis, the sector looks particularly inexpensive – even today after the early year rally. It will be a little harder for the specialty and intermediate companies depending on how long they have to play a lagging catch-up game with costs. But if, and when, costs peak, they should see margin expansion as costs fall and will be able to keep some of the gains, especially if their demand is also growing.

We are seeing pockets of real demand strength in some areas of chemicals, such as building products, and this is allowing producers to push through price increases to reflect higher costs and most likely add some margin. In other areas where the fundamentals might not be quite as supportive, we are still seeing attempts to pass on higher costs. Sika has supported what we have heard from many over the last few weeks, which is that the building products chain remains tight, as demand is strong, capacity is running hard and logistic issues continue to cause problems in some cases from a raw materials perspective and in others from getting finished products to market. Where there is limited ability to increase supply, those selling into the building products space are likely to make more money as they should have strong pricing power – in the US chemical space, we would favor Westlake as a potential big winner from this trend, but Huntsman should also be on the list.

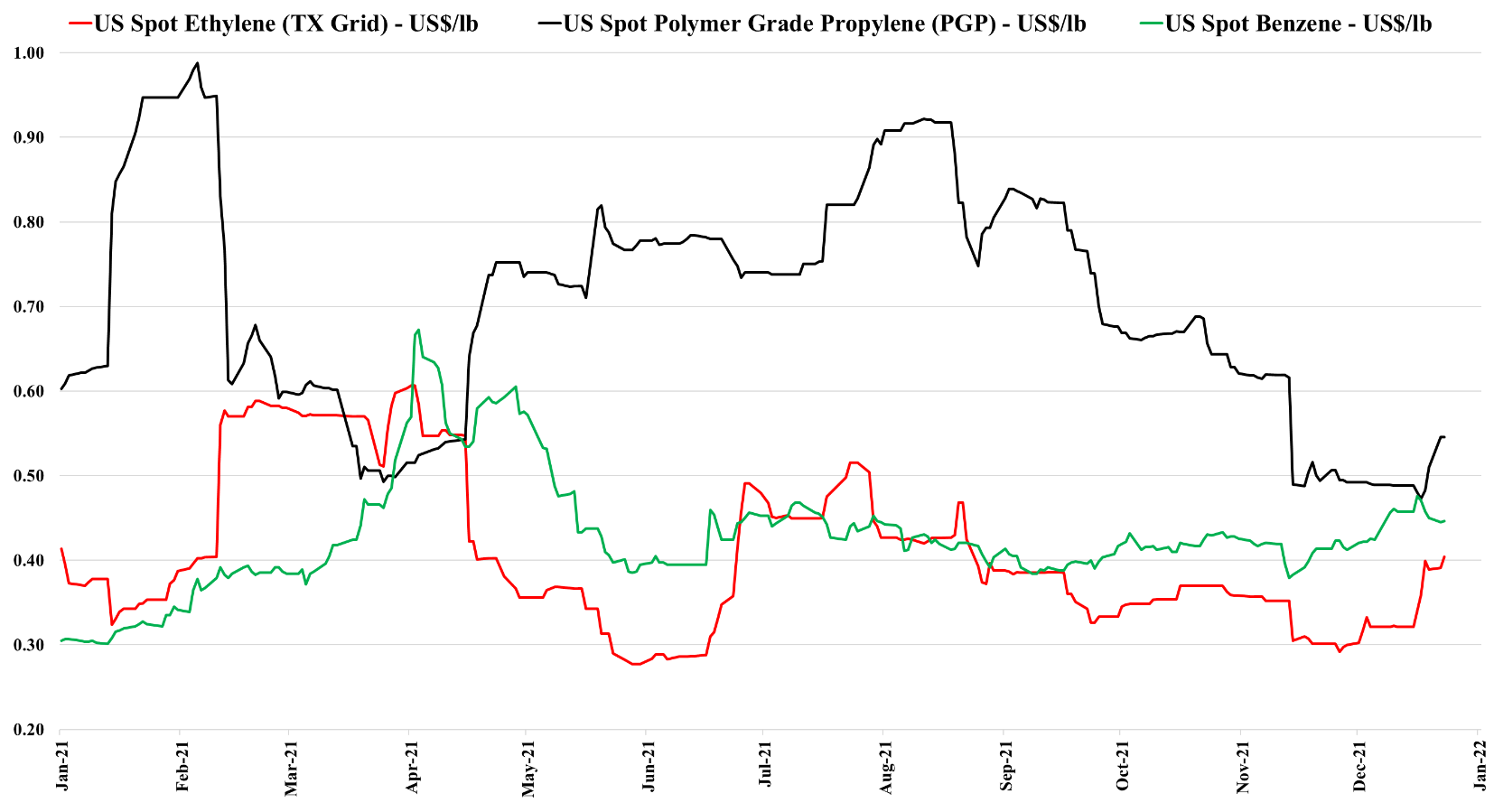

The ethylene price recovery in the US, discussed in today's daily report, is again a function of supply disruptions against a backdrop of robust demand. The net effect is to keep ethylene prices well above costs, at margins that justify investment and it is interesting to see the quick return of the CP Chemical project to the front burner. We could make a case that another ethylene facility in the US is likely a bridge too far at this point, despite the compelling current economics. The deep dependence on the export markets makes the US model very vulnerable to cyclical oversupply, and the current tight market is completely obscuring this risk and lulling producers into what we believe will be a misled sense of security. It is likely that the plants already built will prove to be good investments, not least because of the opportunity profits they are making in their early years of operations, but you would need to have a very bullish longer-term view of oil prices relative to natural gas to invest further, as even with an aggressive on-shoring manufacturing program in the US, the net export nature of the polyethylene businesses in the US is unlikely to change much. New capacity means more ethane demand, against a backdrop of lower E&P investment, and while Chevron has access to equity ethane from its US E&P operations, which may guarantee supply, it does not guarantee the price. Separately, while we believe that recycling targets in the US and the rest of the Wold will disappoint, they will still eat into virgin polymer demand. More chemical recycling will mean more “recycled” polyethylene available from heavy crackers – not ethane-based crackers.

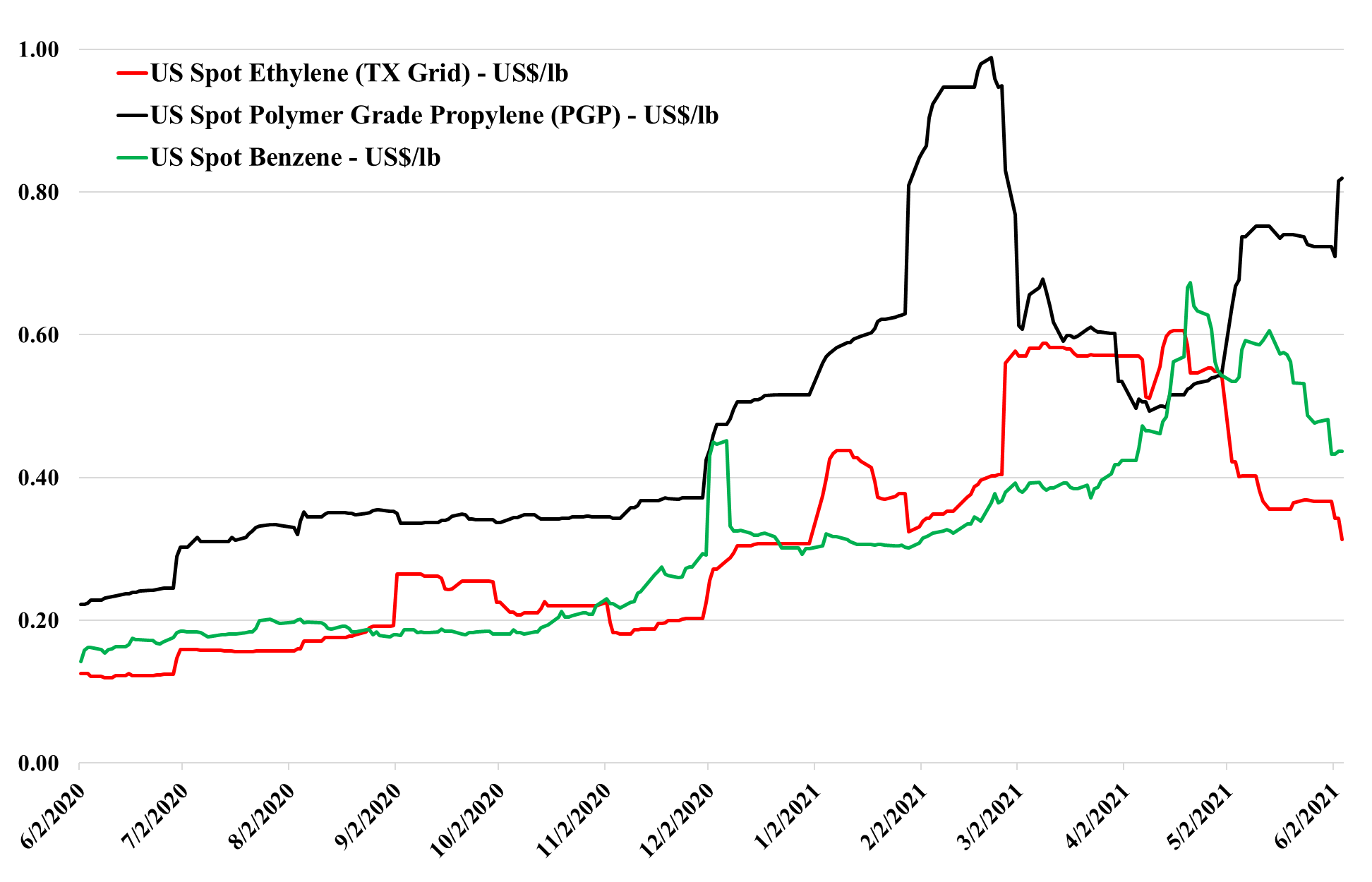

The oversupply in China for many commodities is becoming more evident daily. Our research depicts this as supply-driven, based on the surge of ethylene and propylene and derivative capacity since 3Q 2020. Notwithstanding the Dow commentary (in our daily report today), the weakness in Asia in polyethylene will ultimately impact the US, as the US relies on international demand for at least 25% of its polyethylene production – much less for polypropylene. The gyrations in the ethylene and propylene markets, as shown in the chart below, indicate the US dealing with the differences between the two monomer chains. Far more ethylene and ethylene derivatives move offshore than propylene and propylene derivatives. Despite the ongoing strength in derivatives, the ethylene market is loosening. At the same time, propylene shows extreme volatility because demand remains strong and has seen greater production issues on a relative basis, per our estimate. Supply is barely keeping up, even as refinery rates increase, because of problems with PDH units, pipelines, and splitters, which would not be meaningful in a more normalized market, but make a difference when refinery supply is constrained. High propane prices, which could move even higher, keep upward pressure because of PDH economics and because they keep propane out of ethylene units.