We should not be surprised by the blow-out earnings this week from Livent and Albemarle, as our “critical metals” analysis has been highlighting the runaway prices for lithium all year. This price rise has a much more profound impact on the current suppliers than the start-ups that either have minimal volumes to sell today or none at all. Both Livent and Albemarle were established players in lithium long before the current hype. The higher valuation for Albemarle is both a blessing and a curse in our view as the company is now a little hamstrung with respect to further portfolio changes, given that no one will pay as much for the catalyst and bromine businesses as is reflected in current valuation. You would need to be very convinced that the more focused lithium portfolio would see a further step up in valuation multiple to account for what would inevitably be earnings dilutive divestments.

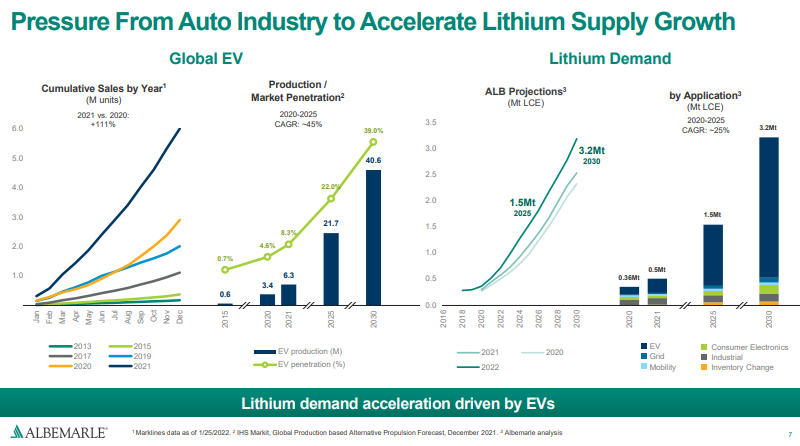

Albemarle’s share price is tumbling today on the news that the company is experiencing cost over-runs in its lithium business and that this resulted in a 4Q loss. The company has tried to deflect with some very bullish views of potential lithium demand, based on EV production growth estimates, but the cost over-runs are another indication of how much inflationary pressure is within all industries today and this news will likely have a negative sentiment impact for any company with material capital spending plans for 2022. The loss at Albemarle comes despite higher lithium selling prices for existing output. We remain very concerned that, despite high capital costs, the technology barriers to entry for the more commodity grades of lithium required for most batteries are very low, and that with the hype around potential demand – as indicated by Albemarle – too much lithium capacity will be built, ultimately causing wild swings in prices. If we get a negative swing in pricing coincident with new capacity start-ups, where the new capacity cost more than planned, we could see some poor returns on investment periods during this decade. To be clear, we expect lithium demand to grow very quickly, but we expect supply to grow quickly also. See more in today's daily report.