The AkzoNobel comment today on completing its share buyback is a reminder that the chemical industry, in general, is reporting earnings that for the most part include record or near-record profits today and very strong momentum into 2Q 2021. They should all be prepared to answer the question of what they plan to do with the cash. The temptation is to build because prices are high and in some cases, customers are short of product and pleading for more supply. We often talk about the economics of NOW being used to justify spending far more than it should be – not just in Chemicals but also in other industries. In some areas, we are genuinely short of materials and semiconductors are a clear example of where underlying global demand has caught up with supply. Materials suppliers into this space are likely to see new capacity well utilized. For many of the other chemical segments, there is too much near-term noise to say with any certainty what is structural versus an immediate shortage. COVID, weather, a blocked canal, and unusual patterns of consumer spending have all played a part in inflating demand relative to supply, and we could be looking at a very different dynamic in 6 months.

Recent Posts

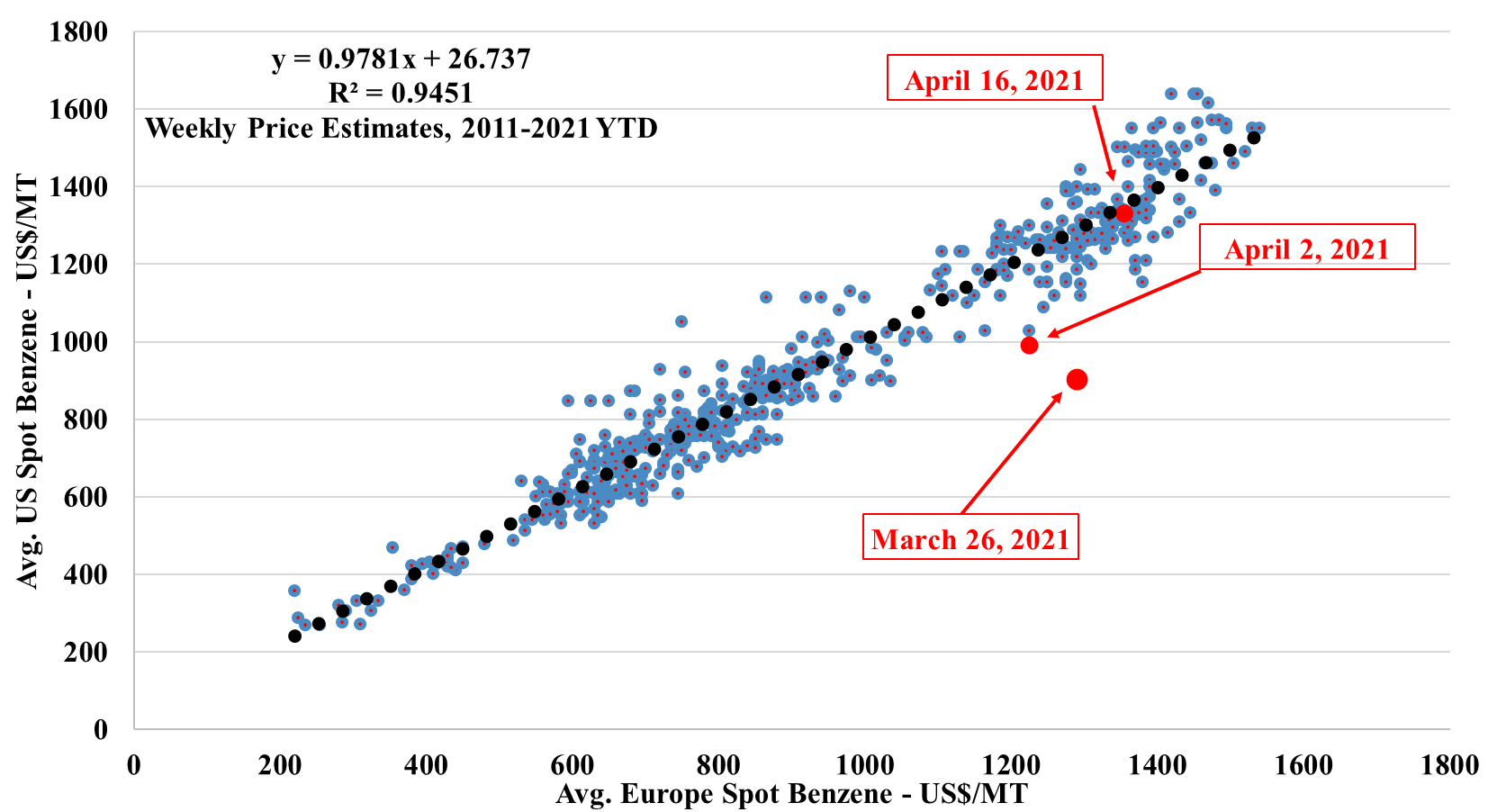

So, if you had been able to play the obvious arbitrage in the exhibit below when we published it first in March, you would have done quite well. You would have done better if you had just bought benzene on both continents, but you would have taken more risk. We like these scatter charts and we will use them more often when there are obvious regional arbitrages or just product arbitrages within a region. The overall benzene tightness has been caused by production outages in the US, shipping issues to Europe, and very strong demand for benzene derivatives. The start-up of the Shell POSM unit in the Netherlands has likely added to the imbalance as the facility is a major ethylbenzene consumer.

As the Exhibit below shows, the US manufacturing industry is on fire, driven by strong domestic demand and all of the logistic and social issues associated with importing. There is both a consumer and a big box retailer desire to buy “American” and it helps to explain why we are seeing such significant raw material shortages in the US. The China export headline linked is also probably correct as it applies to shipments to the US and to Europe, where the higher costs of freight are adding cost pressure and making the “buy locally” decision easier. For the chemical industry, this is more US domestic demand versus exports for most products, which is a net positive. For Europe, it will likely be more net chemical and polymer imports, which will be good for EU producers as prices will be higher and good for US exporters as Europe is close and has higher pricing.

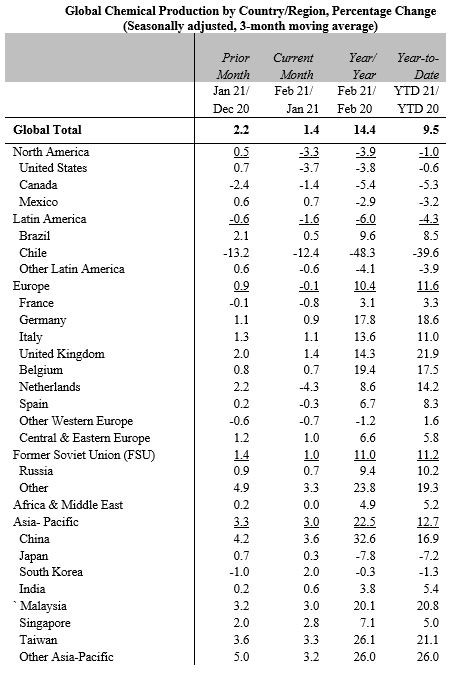

We are seeing some very strong global production growth in the ACC statistics for February – see table below – both on a year-on-year basis and month-on-month. As we look at China and parts of Europe we should remember that the year-on-year comps are easy as the COVID-related shutdowns were in full swing in February 2020 in China and beginning in Europe. But the month-on-month data is as strong for China as it was for January and it reflects both the wave of new chemical capacity and strong domestic demand, both for domestic consumption of durable and consumables and exports of durables – which continue to keep freight rates high (see above) and ports at capacity (see the last section below). February global numbers have been held back by the Texas freeze issues and this helps to explain the step down in plastic resin growth in particular in February, despite the new capacity in China and some new capacity in the US. The lower production growth relative to underlying demand, especially in the US, helps to explain why pricing has been so high.

About a year ago we wrote a piece highlighting the longer-term risks to plastics supply and demand because of oil company interest in chasing a market that they perceived to be growing faster than other oil products markets, and potentially running headlong into a plastic market that was either seeing slower growth because of concerns around plastic waste and sustainability or was declining.

A year of COVID-related uncertainty put some of the projects on hold, but as we move through 2021 we have a couple of factors driving the plastic bet again. First, demand for plastics is very high and pricing is “off the charts”, suggesting that converting oil to plastics could be profitable as well as a home for some of the oil. Second, with the climate agenda now front and center in every economy and more discussions around electric vehicles, hydrogen, and biofuels, the future for oil demand is looking incrementally bleaker. The economics of NOW thesis would support large-scale investment in oil to chemicals – either directly – or through refining to more common feedstocks. But…

The price dynamic discussed in today's report and shown in the exhibit below looks unusual in a recent historic context and is unlikely to last very long, but it is worth noting that the recent history does not reflect the longer-term history.

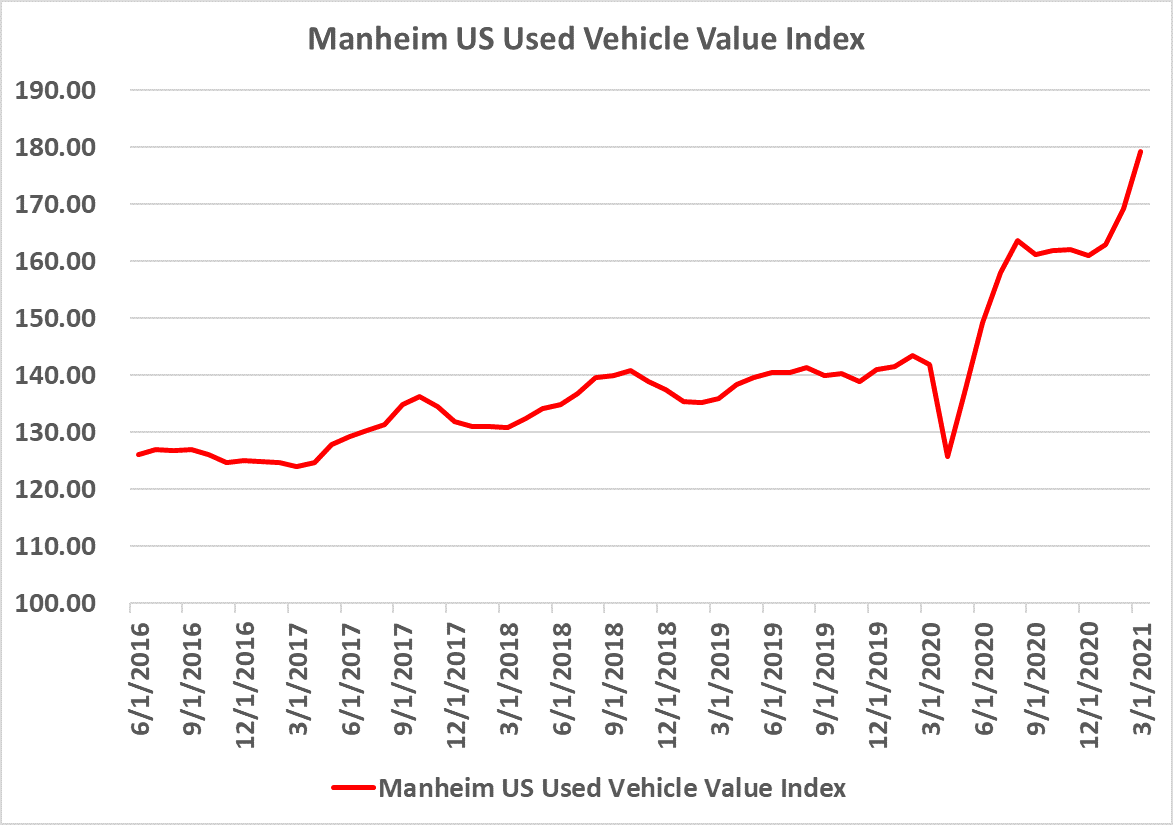

US auto sales remained robust in 1Q21 (see Exhibit below), while our checks around Houston suggest car lot inventory has notably diminished and used vehicle values remain robust (2nd Exhibit). They are likely to stay that way in the near-to-medium term.

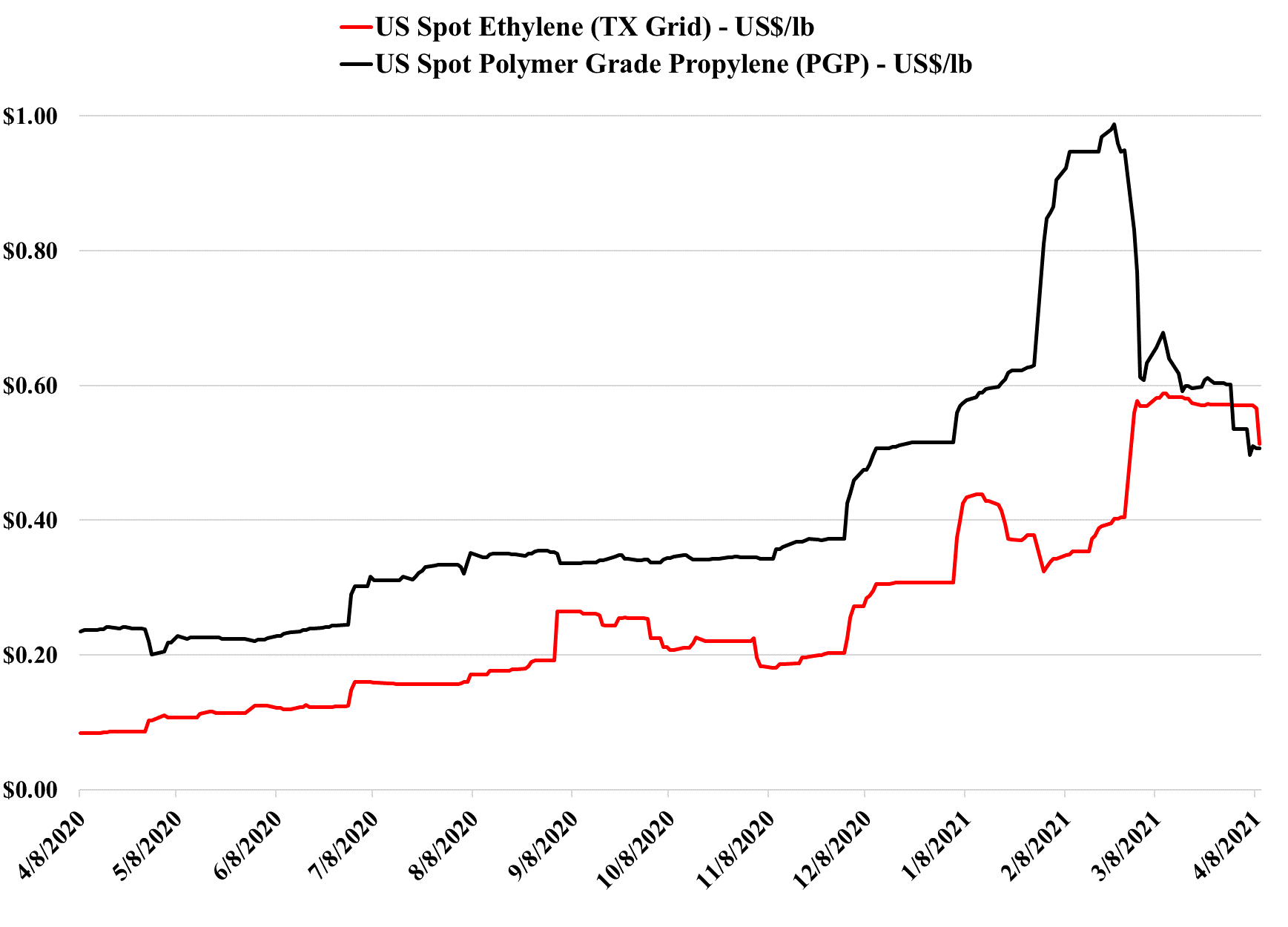

The propylene swing relative to ethylene in the US, as shown in the graph below is extraordinary. As we discussed yesterday it is a typical, albeit, tightly compacted commodity cycle, with the desperate shortage finding the incremental buyer who was more concerned about volume than price and the rapid supply and demand response that followed the peak in propylene pricing to correct the imbalance. The current price relative to ethylene does not look stable either and we would expect a reversal quite quickly – incremental propylene production from PDH is based on a higher cost feedstock than ethylene today – propane prices are higher than ethane prices, and while the volatility may remain in the relative price, we would expect to see propylene pricing rise back above ethylene again, fairly quickly. If polypropylene prices follow propylene and start to reflect a discount to polyethylene, that could also drive some polymer switching at the margin, which would help propylene relative to ethylene.

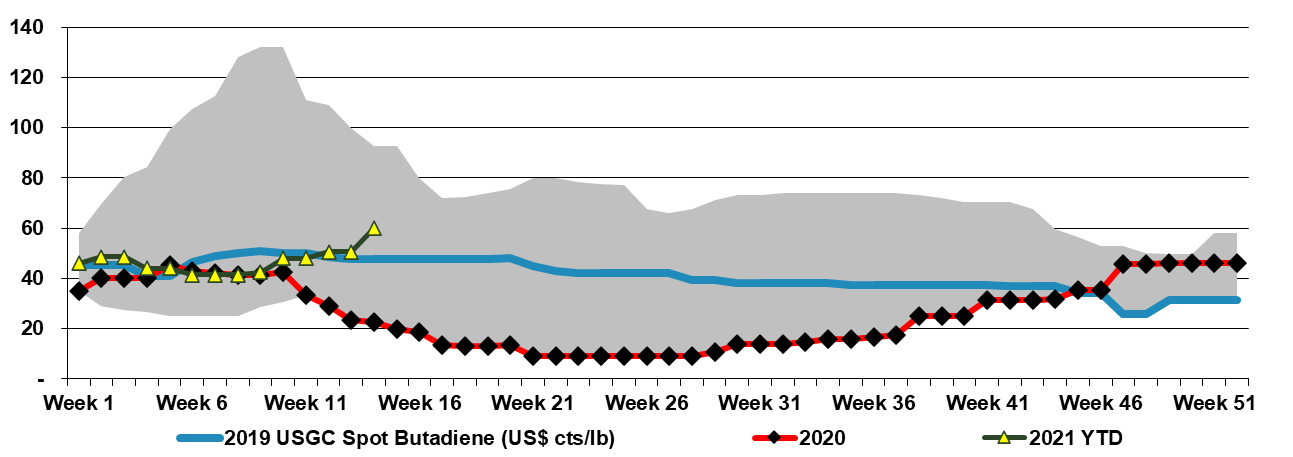

Last week we talked about the robustness of the US propane market and the China PDH headline is another example of offshore propane demand that we believe will keep US propane prices high, and probably high relative to ethane. This will mean that ethane stays favored as an ethylene feedstock but it will keep US PDH costs higher than they have been over the last 5 years. With propane and naphtha staying out of US ethylene plants we are seeing strength in butadiene, as domestic demand picks up and production remains constrained. Butadiene could see price support for some time as the ethylene economics are unlikely to change, especially if we see more Permian output in 2Q and into 2H 2021 as this will keep ethane supplies high.

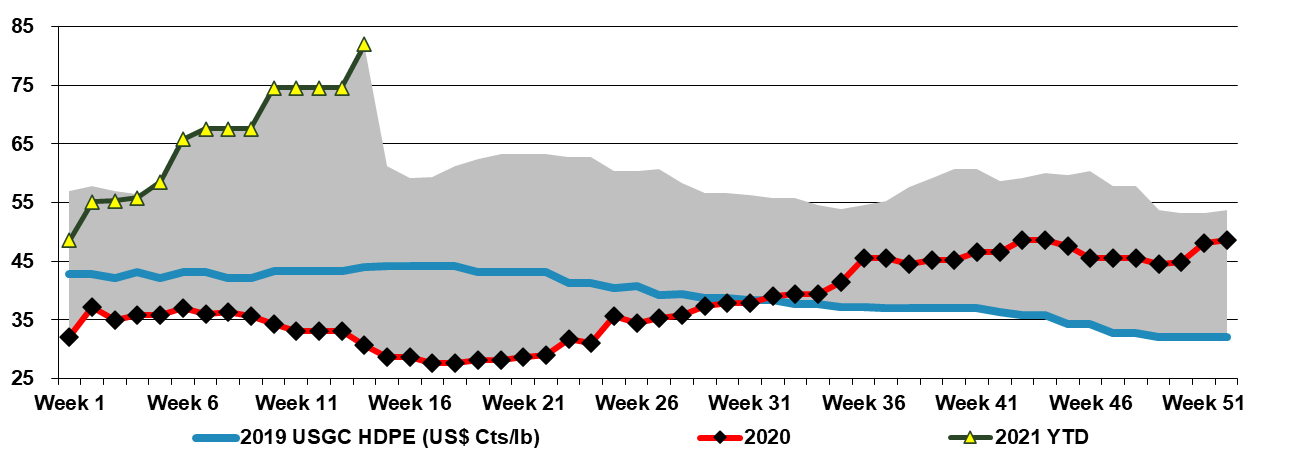

The fall in Chinese imports is not a surprise given the significant capacity additions over the last 6 months. There is an additional wave of investments planned for the next 6 months and we could see imports fall further as the year progresses. Even with strong demand growth in Asia and other parts of the world, this could leave the major exporters – the Middle East and North America with surpluses, although that is not evident today. Prices continue to rise for polyethylene in the US (see chart below) and Europe, partly because of the lingering impacts of the freeze, but also because apparent demand is high. This is going to be a tough year to call as we expect to see the supply chains over-compensate for the problems that have existed since the last quarter of 2020 and chain inventories to build. This could add several hundred basis points of demand in 2021, masking the new capacity in China and the theoretical oversupply that would exist if all global facilities were operating. This could set up 2022 for disappointment, and impact the longer-term supply/demand balance negatively, as the high profits of 2H 2020 and 2021 could encourage more investment such as the ones highlighted by SABIC, and India.