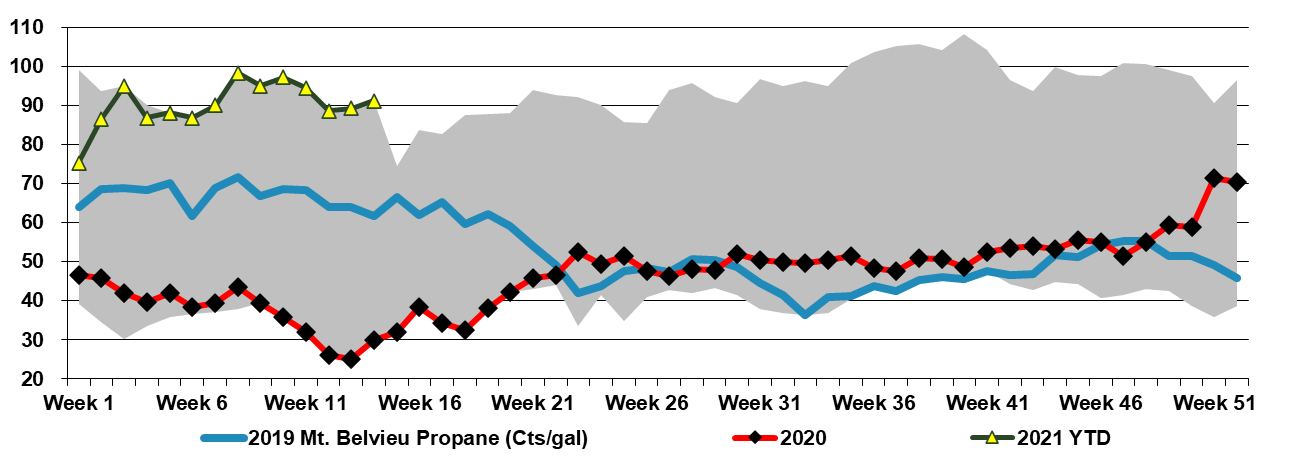

The Exxon/Chevron shale headline is interesting, as the oil majors have made some commitments to shareholders concerning investment and capital spending since the Pandemic began, and while they appear to be sticking to their projections, it must be increasingly uncomfortable to do so. This is because the economics now work in the Permian and the independents are back with a vengeance. Historically, market share arguments would be made to ramp back up again, especially as Exxon, Chevron, and Oxy likely have the lowest incremental F&D costs in the Permian. Chevron and Exxon have the balance sheet flexibility to stick to their plans and make further consolidating moves if the oil price pulls back – Oxy does not. All three companies would likely face investor backlash if they increased E&P spending today.

Recent Posts

We note the increasing news on more geographically diverse investments in battery manufacture – see the Canada headline below. With the Intel chip investment in the US and battery investments all over the world, it is very clear that the automakers no longer wish to be so dependent on imports from Asia. In our Sunday Recap (Ship to Wreck: And The Supply-Chain Challenges Continue!), we discussed the possibility of a major wave of manufacturing investment in the US, with some but only a little marginal help from the Biden Administration. The consumer and retailer demand is there for more US content and the supply issues over the last few months have only increased the level of interest in having more local production.

Two thoughts that we published on Sunday:

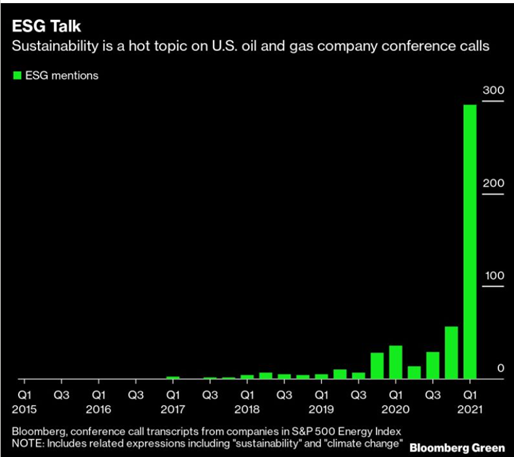

- The buzz acronym of the year is ESG, as clearly shown in the chart – and we believe that it will become increasingly difficult to get any new investment in the US (and Europe) off the ground without a robust climate-friendly plan, focused on energy use, the product life-cycle and emissions and waste disposal.

- We saw NextDecade strike a deal with Occidental last week to capture and use the carbon dioxide associated with its delayed LNG facility in Southeast Texas. The plant has all of its regulatory approvals and we believe the move was to satisfy some of the potential LNG customers for the facility, who are showing concern around the large carbon footprint of natural gas liquefaction. NextDecade’s move may provide regulators with a precedent as they think about new US investments.

- We should also not underestimate the pressure being placed on investment banks by their stakeholders when it comes to lending standards, and any new US project that requires debt financing (so any project of size), will find that their potential lenders are as tough on them if not tougher than regulators when it comes to environmental footprints.

- This could be good for the chemicals and plastic industry in the US and it would most likely increase domestic demand and make the industry less reliant on exports. Chip manufacture requires many chemical inputs from substrates to photoresists to industrial gases. Many of the other manufacturing opportunities would also consume chemicals and plastics:

- Auto parts

- Household goods

- Medicines

- Packaging or all of the above and other products

- The facility constructions would be good for building-related products such as polyurethanes and PVC.

Given the much lower margins that US polymer exporters are getting versus selling domestically today, higher levels of domestic demand would be a net positive.

A couple of headlines stand out today but the BASF capital markets day is probably not one of them. This is now becoming the norm; to provide an investor update tailored at focusing on clean energy and sustainability goals, and BASF’s expectations are not much different from others – there is a bold claim about 2050 and some harder targets by 2030. So far we have yet to see one of these presentations where the math is believable, and the investment targets in dollar terms all seem too low to meet a net-zero goal. To be fair, it is hard to know what will happen in 5 years, let alone from 2030 to 2050, and we would doubt that anyone has a good estimate today. BASF and others will likely end up spending multiples of what they currently project, but this may not be a bad thing – much of the spending will be backed by incentives (or encouraged by penalties) and all of the spending will be good for jobs and economic growth.

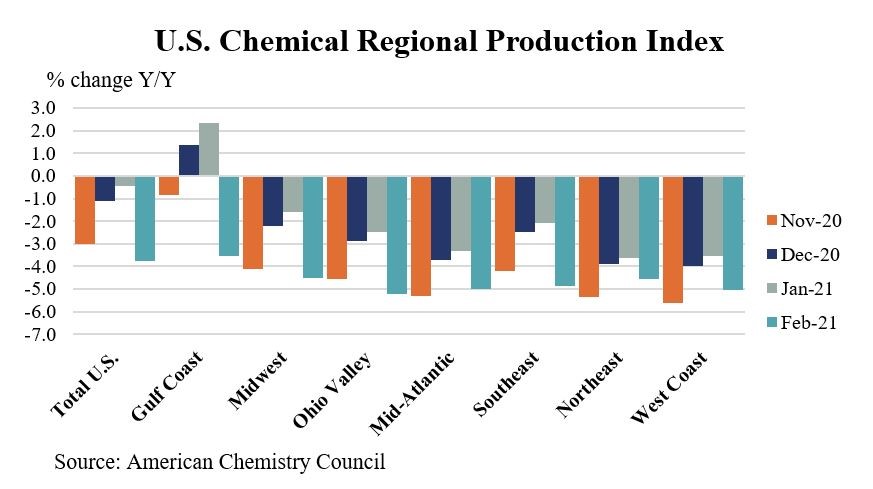

It remains very interesting to us that despite the apparent major shortages of chemicals and polymers in the US, the industry continues to operate at rates below those of a year ago, according to the ACC. We fully understand the Gulf Coast swing in February and are surprised that it was not worse, given the extent of the shutdowns we have been monitoring – March should be bad also because many of the shutdowns extended into March. While the bulk of the US chemical industry is in the Gulf Coast – as can be seen by the Gulf Coast influence on the “total US” bar, why production remains below 2020 levels in other regions is a little surprising. Granted, February 2020 was not impacted by the Pandemic and the economy was strong and demand for materials high, but with the import issues of the last 4 months and the move by US manufacturers and retailers to source more product from the US, we remain surprised that regional chemical production outside the US Gulf has not at least matched 2020 levels.

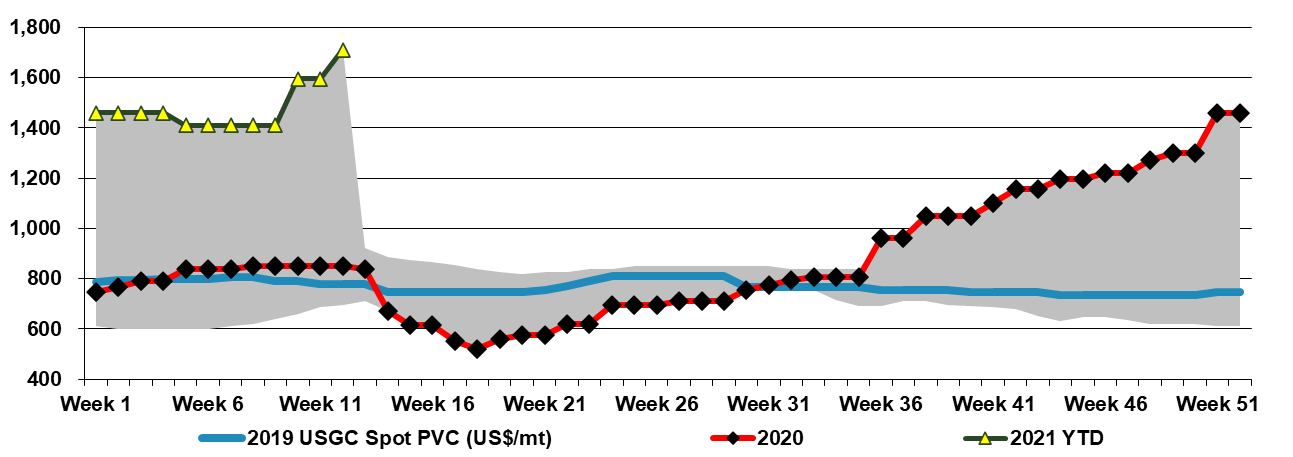

Asia polyvinyl chloride (PVC) prices reflect a five-year low relative to US spot levels, but both price points reflect five-year highs on an absolute basis.

The spread of the US supply problems to Europe is an indication of how much US polymer has been moving to Europe and how dependent the region has become on US material. This is not evident in publicly traded deals, as most, if not all f the material moving is on contract and intra-company (Dow moving to Dow’s customers, ExxonMobil to their customers, etc). But the production shortages in the US have impacted customers in each region.

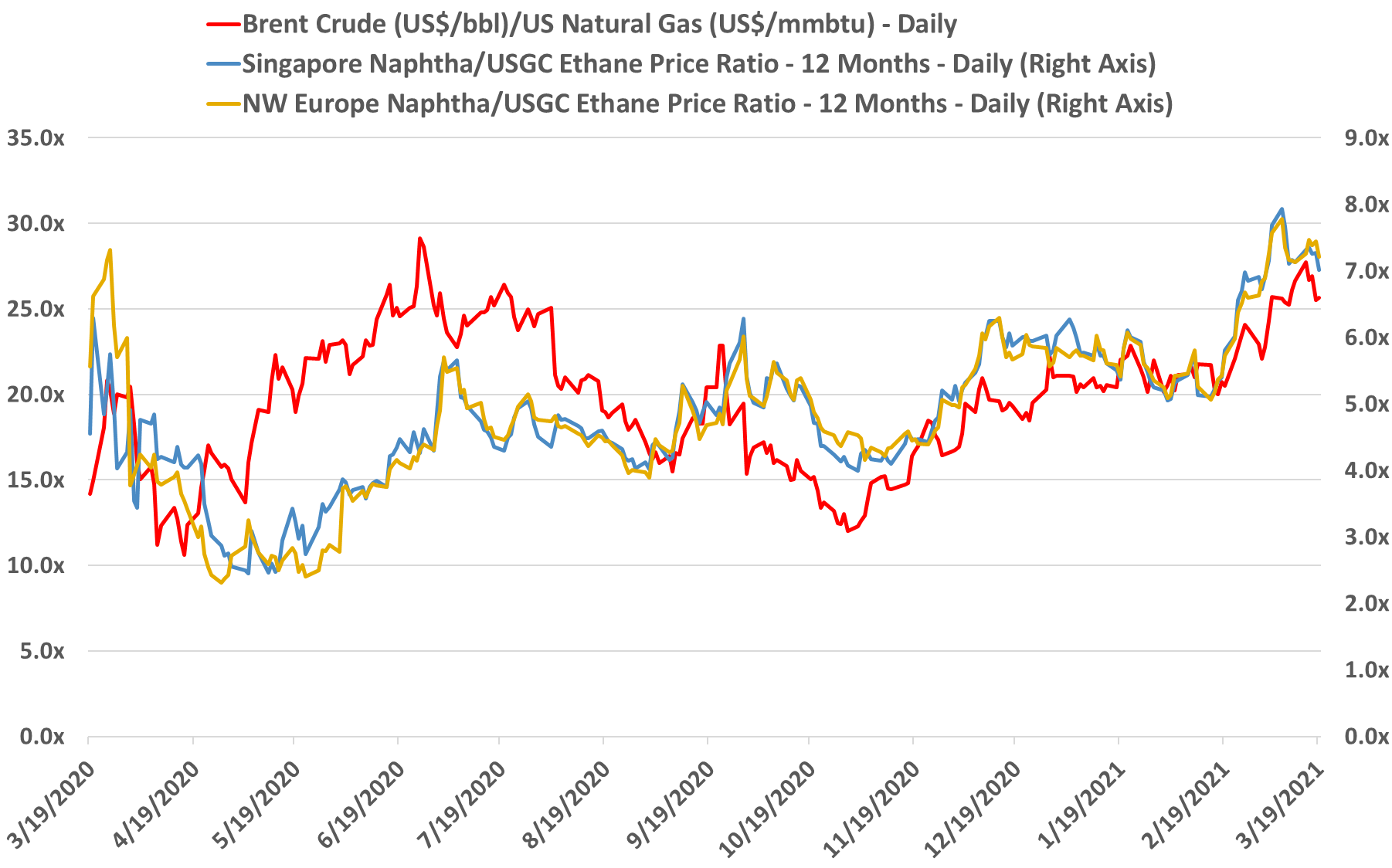

The US polymer shortage is impacting supply in the rest of the world where the US is a major global supplier, but the benzene comments below suggest that this may not be the case where the US is not a major global player. Demand for styrene is high and prices of styrene and polystyrene are higher globally, but this alone is not enough to support benzene in Asia, where there has been a lot of new supply from ethylene units and where there has also been a strong pull on paraxylene to supply new PTA capacity. Reformer-based paraxylene has benzene as a co-product and the PTA expansion in China has been meaningful in the last few months. Separately, the phenol side of benzene demand is not looking as exciting as the polymer markets especially in some of the epoxy resin markets and in particular those facing the aerospace industry. This is a more significant demand impact in the US and Europe, but should also be felt in Asia.

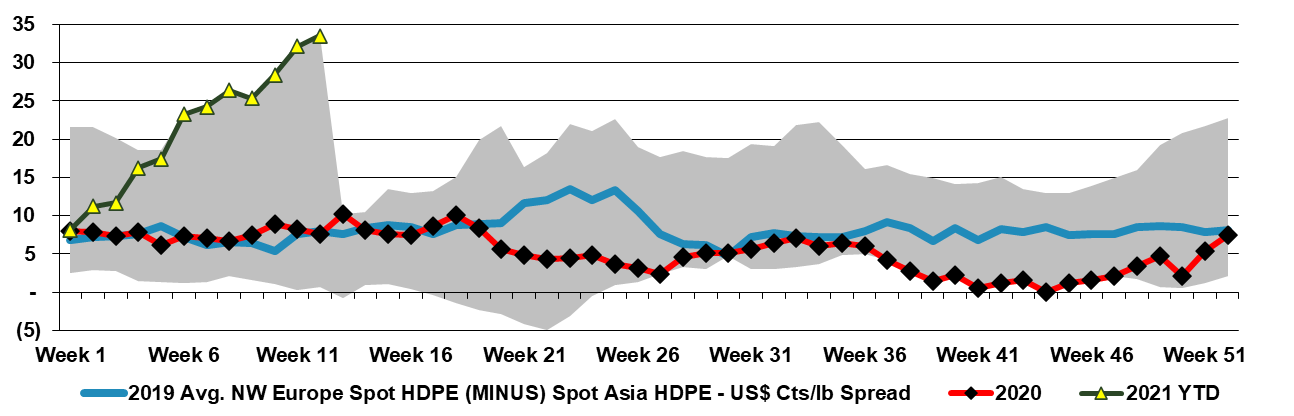

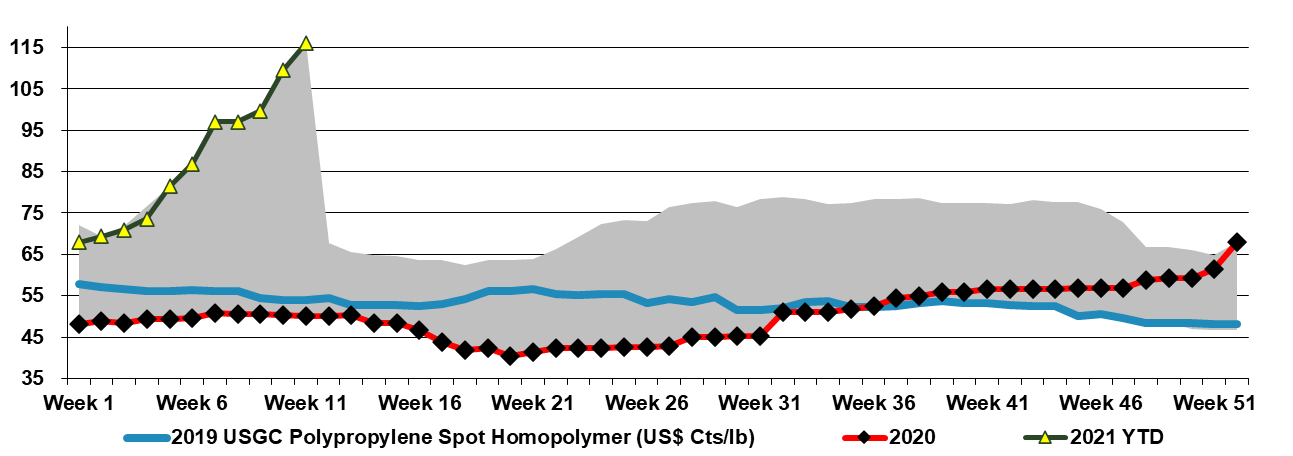

The exhibit below shows a “crazy” 5-year extreme price difference between polymer pricing in Asia and the US, and scanning our longer-term database we believe this is an all-time extreme not just for the last 5 years. This is very bad for US polymer sellers in the medium to long-term, despite some windfall profits that may extend through 1H 2021. The high prices are doing a couple of things, they are encouraging plastic consumers to experiment with alternative materials and they are encouraging them to experiment with other suppliers, including imports.

While we are looking at price increases all across the board, the more interesting factor is the primary driver, which is the delayed restarts of enough US Gulf capacity to make a meaningful difference to availability. As noted in one of the headlines below, there will be corrective mechanisms and one of those may be the closure of some derivative consuming facilities, either because they cannot get enough product to operate or because they cannot pass through escalating costs. The current situation is likely to roll through into selective product and consumer good shortages, especially where the polymer or chemical content is high and the value of the product is low – some cheap plastic durables for example, or lower quality household products.

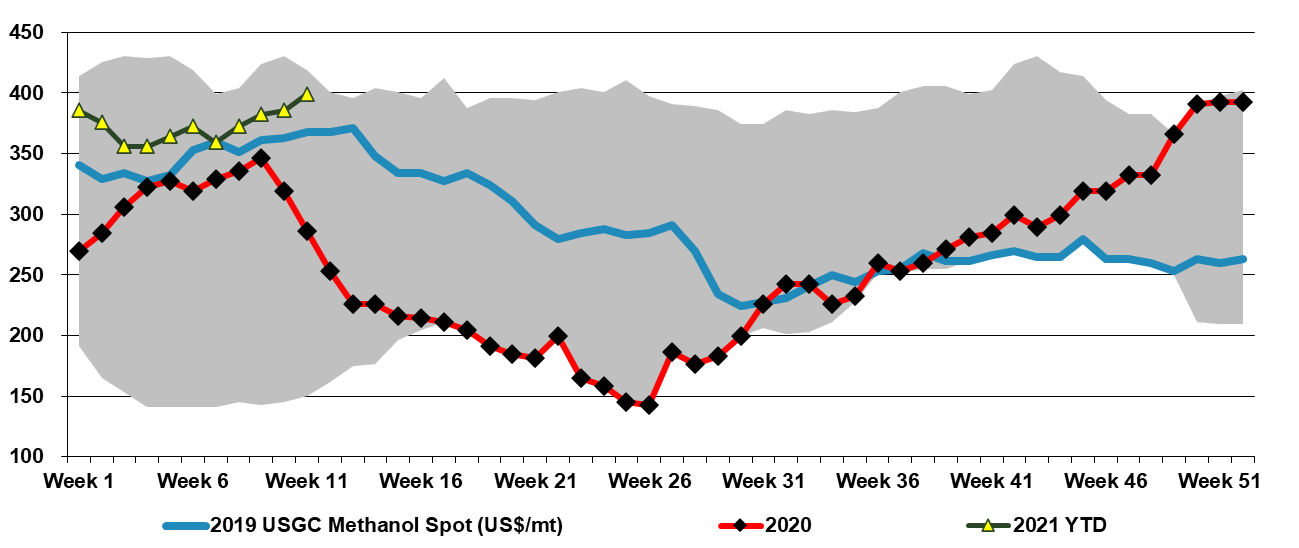

In today's daily, we discuss methanol pricing and show that the arbitrage with Asia is now negative, based on the near-term increase in US spot pricing. As with polyethylene, the major exporters are more concerned about the export margin over their costs, versus the difference between spot prices in each region. Certainly, where they have flexibility some US producers will try to divert methanol to the domestic market, but likely not at the expense of important export relationships and contractual obligations.