The spread of the US supply problems to Europe is an indication of how much US polymer has been moving to Europe and how dependent the region has become on US material. This is not evident in publicly traded deals, as most, if not all f the material moving is on contract and intra-company (Dow moving to Dow’s customers, ExxonMobil to their customers, etc). But the production shortages in the US have impacted customers in each region.

The US polymer shortage is impacting supply in the rest of the world where the US is a major global supplier, but the benzene comments below suggest that this may not be the case where the US is not a major global player. Demand for styrene is high and prices of styrene and polystyrene are higher globally, but this alone is not enough to support benzene in Asia, where there has been a lot of new supply from ethylene units and where there has also been a strong pull on paraxylene to supply new PTA capacity. Reformer-based paraxylene has benzene as a co-product and the PTA expansion in China has been meaningful in the last few months. Separately, the phenol side of benzene demand is not looking as exciting as the polymer markets especially in some of the epoxy resin markets and in particular those facing the aerospace industry. This is a more significant demand impact in the US and Europe, but should also be felt in Asia.

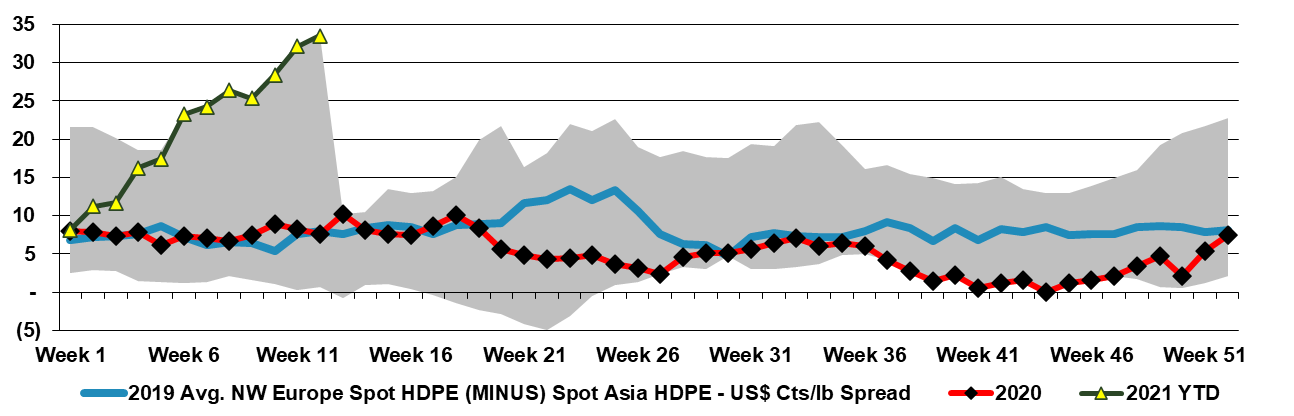

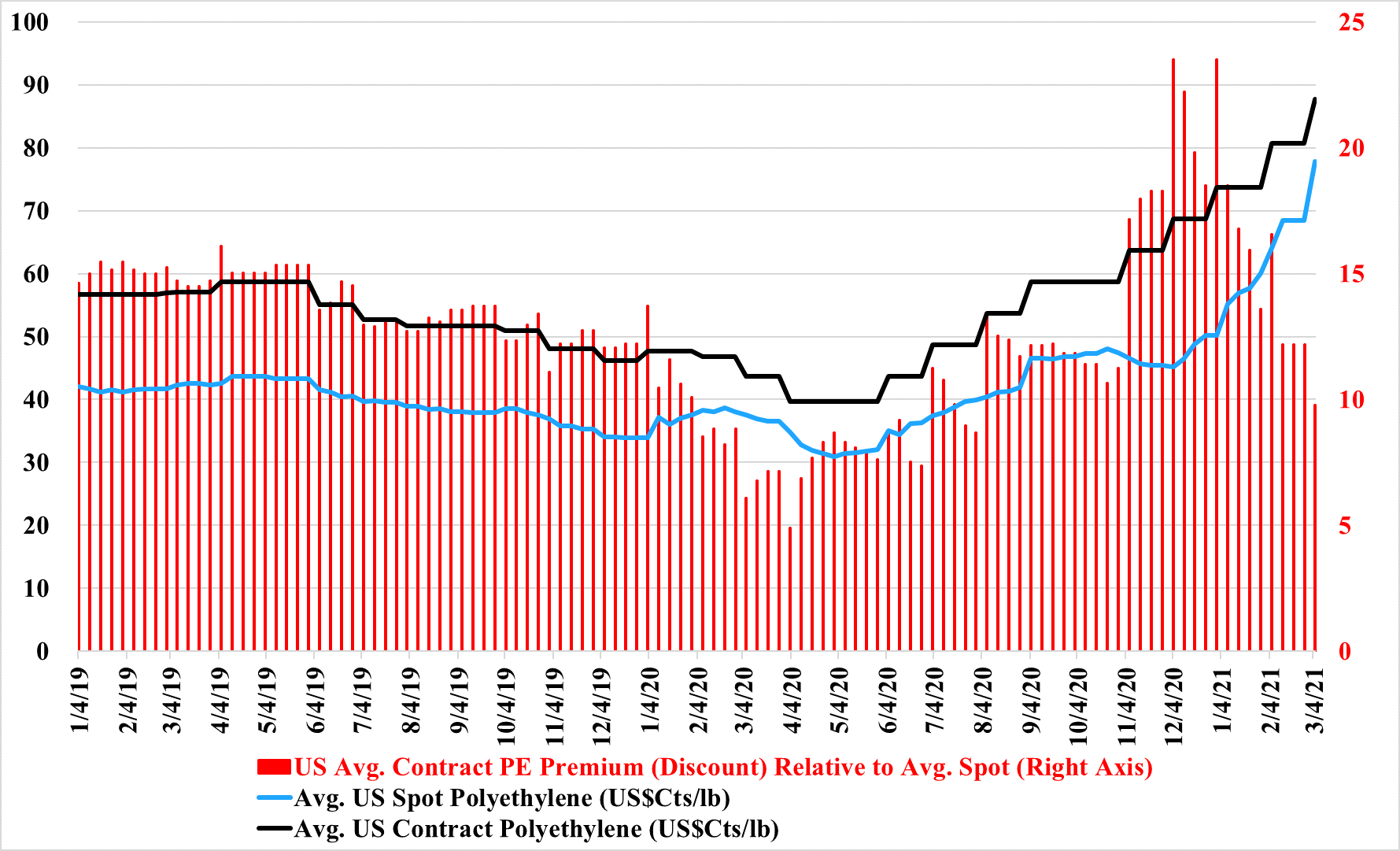

The exhibit below shows a “crazy” 5-year extreme price difference between polymer pricing in Asia and the US, and scanning our longer-term database we believe this is an all-time extreme not just for the last 5 years. This is very bad for US polymer sellers in the medium to long-term, despite some windfall profits that may extend through 1H 2021. The high prices are doing a couple of things, they are encouraging plastic consumers to experiment with alternative materials and they are encouraging them to experiment with other suppliers, including imports.

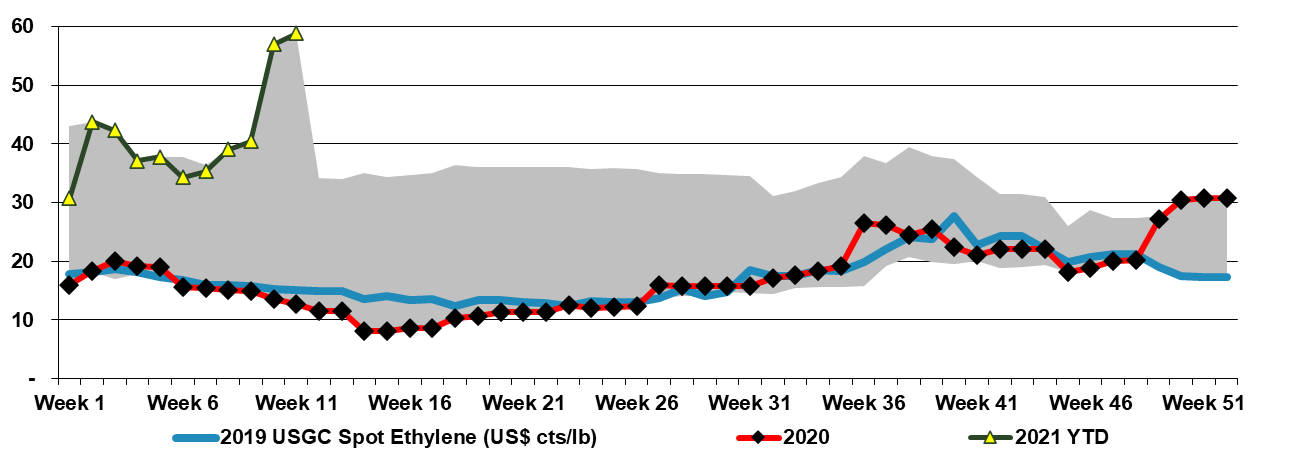

While we are looking at price increases all across the board, the more interesting factor is the primary driver, which is the delayed restarts of enough US Gulf capacity to make a meaningful difference to availability. As noted in one of the headlines below, there will be corrective mechanisms and one of those may be the closure of some derivative consuming facilities, either because they cannot get enough product to operate or because they cannot pass through escalating costs. The current situation is likely to roll through into selective product and consumer good shortages, especially where the polymer or chemical content is high and the value of the product is low – some cheap plastic durables for example, or lower quality household products.

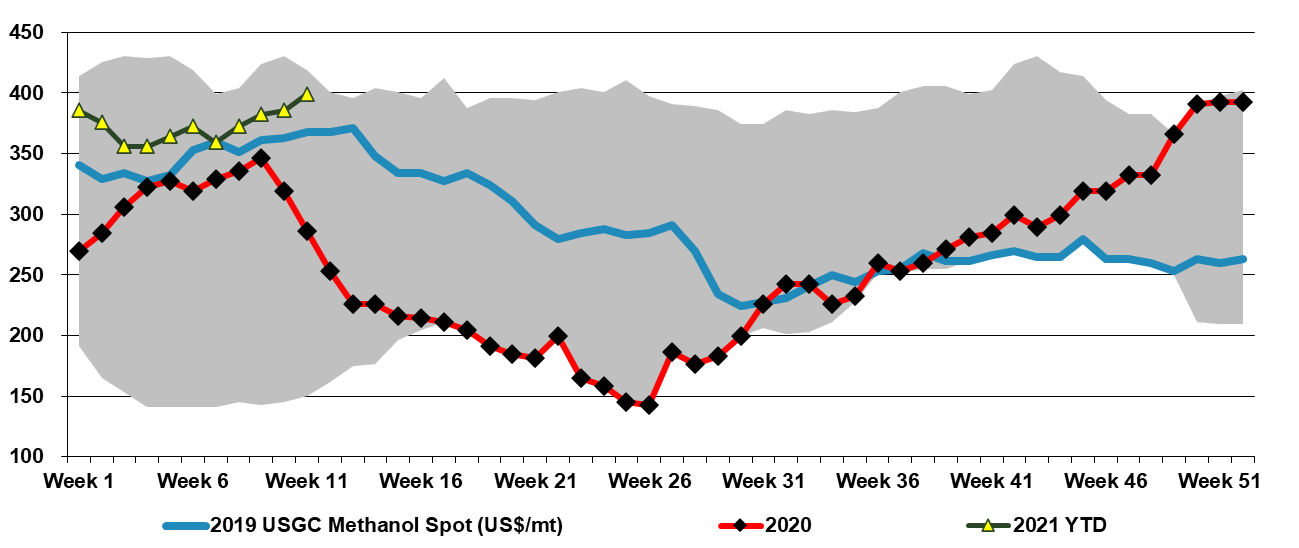

In today's daily, we discuss methanol pricing and show that the arbitrage with Asia is now negative, based on the near-term increase in US spot pricing. As with polyethylene, the major exporters are more concerned about the export margin over their costs, versus the difference between spot prices in each region. Certainly, where they have flexibility some US producers will try to divert methanol to the domestic market, but likely not at the expense of important export relationships and contractual obligations.

The theme of product shortages continues, with prices in China reflecting the global tightness and signaling that the import dependence is still there for some products, despite the recent and continuing capacity additions. The base chemical price rises in the US are contributing to the rising US producer price index for February and given that we have seen further price rises since February, March could show another jump.

Today we had earnings reports from both Braskem and Lanxess. It is hard to fault either company for the tones and expectations lined out in today's report. This is an industry where forecasting is generally problematic as there are too many potential influences that are not only outside the control of the companies themselves, but also prone to surprise movements regularly. Who could have foretold COVID and the early impacts of COVID on all commodity and specialty markets. Equally, no-one forecast the rapid rise in durable demand in 2H 2020 the subsequent impact that it has had on global supply chains – and then there is the weather!

We are experiencing a perfect storm for chemical pricing. The supply chain dislocations are causing buyers right down the chain to think about both supply routes and how much inventory they should hold (we would expect a general working capital increase across manufacturing and possibly retailing over the next 6 months – price and volume-driven). The risk of over-buying is high, and, for example, plastic buyers may be pressing all suppliers for contract maximums, in the hope that one or two can deliver. Things will change when four or five deliver in the same week – unlikely before late 2Q 2021 in our view. When you add the supply chain issues to rising oil prices and the US base chemicals and polymer production issues, you have a global tight market that is expressing itself most aggressively in the US and creating some of the extraordinary trends in the charts we highlighted in today's daily.

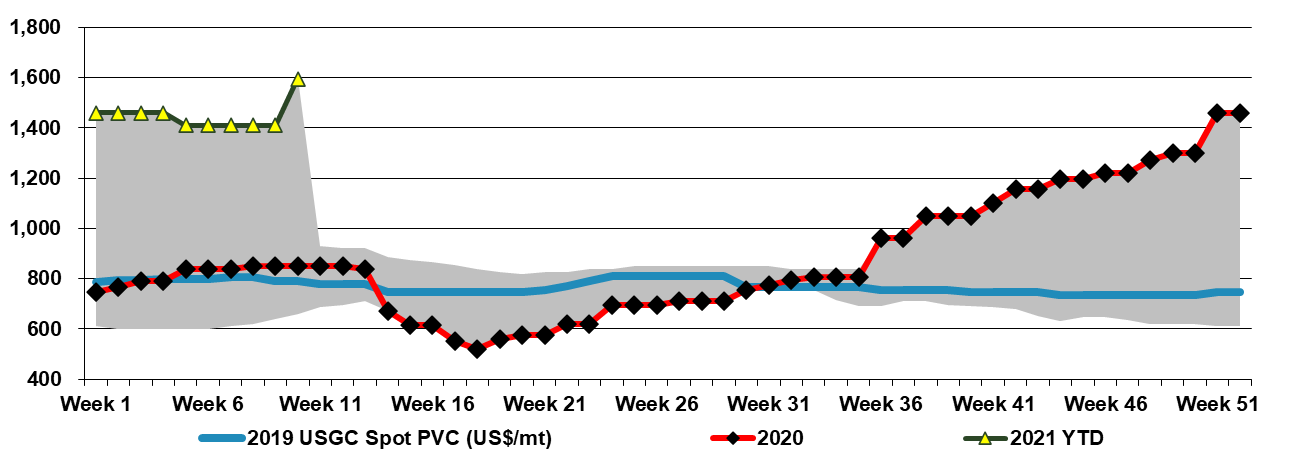

One of the striking conclusions from our Weekly yesterday (charts 41-43) was the steady upward march in PVC pricing in all regions – everywhere is at 5-year highs, the US, Europe, and Asia. While it is very easy to be distracted by the spikes in polyethylene and polypropylene pricing, we believe that these price rises are far more impacted by the spike in consumer durable spending, production outages, and global supply dislocations than PVC, which we have believed for some time has better longer-term fundamentals and will benefit from infrastructure spending increase, while not being materially impacted by a consumer flip from durables to travel.

As we anticipated (and have covered at length in our ESG and Climate service), we see a renewed increase in adding more US LNG capacity as global markets tighten again and as more emerging economies see LNG as a cleaner and potentially cheaper path to broader electrification. There is also talk of changing contract structures to share the pains and gains of LNG price volatility. This would be good for the buyers and is likely to generate more importer interest, but it will challenge some of the independent projects from a financing perspective if more variable price components become the norm in contract construction – this could create a competitive edge for the oil majors over the independents, as they would have less trouble raising the investment funds. One of the enabling factors of the early LNG projects was the fixed nature of contracts and the ability to lock in a largely fixed return for both equity and debt investors.