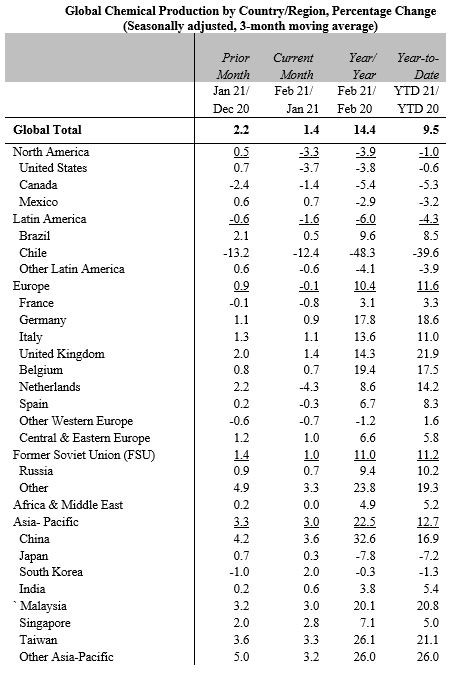

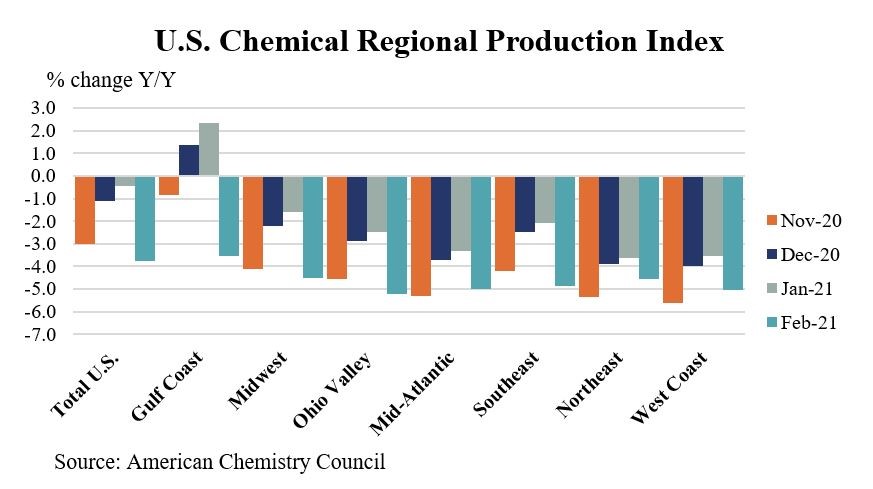

We are seeing some very strong global production growth in the ACC statistics for February – see table below – both on a year-on-year basis and month-on-month. As we look at China and parts of Europe we should remember that the year-on-year comps are easy as the COVID-related shutdowns were in full swing in February 2020 in China and beginning in Europe. But the month-on-month data is as strong for China as it was for January and it reflects both the wave of new chemical capacity and strong domestic demand, both for domestic consumption of durable and consumables and exports of durables – which continue to keep freight rates high (see above) and ports at capacity (see the last section below). February global numbers have been held back by the Texas freeze issues and this helps to explain the step down in plastic resin growth in particular in February, despite the new capacity in China and some new capacity in the US. The lower production growth relative to underlying demand, especially in the US, helps to explain why pricing has been so high.

About a year ago we wrote a piece highlighting the longer-term risks to plastics supply and demand because of oil company interest in chasing a market that they perceived to be growing faster than other oil products markets, and potentially running headlong into a plastic market that was either seeing slower growth because of concerns around plastic waste and sustainability or was declining.

A year of COVID-related uncertainty put some of the projects on hold, but as we move through 2021 we have a couple of factors driving the plastic bet again. First, demand for plastics is very high and pricing is “off the charts”, suggesting that converting oil to plastics could be profitable as well as a home for some of the oil. Second, with the climate agenda now front and center in every economy and more discussions around electric vehicles, hydrogen, and biofuels, the future for oil demand is looking incrementally bleaker. The economics of NOW thesis would support large-scale investment in oil to chemicals – either directly – or through refining to more common feedstocks. But…

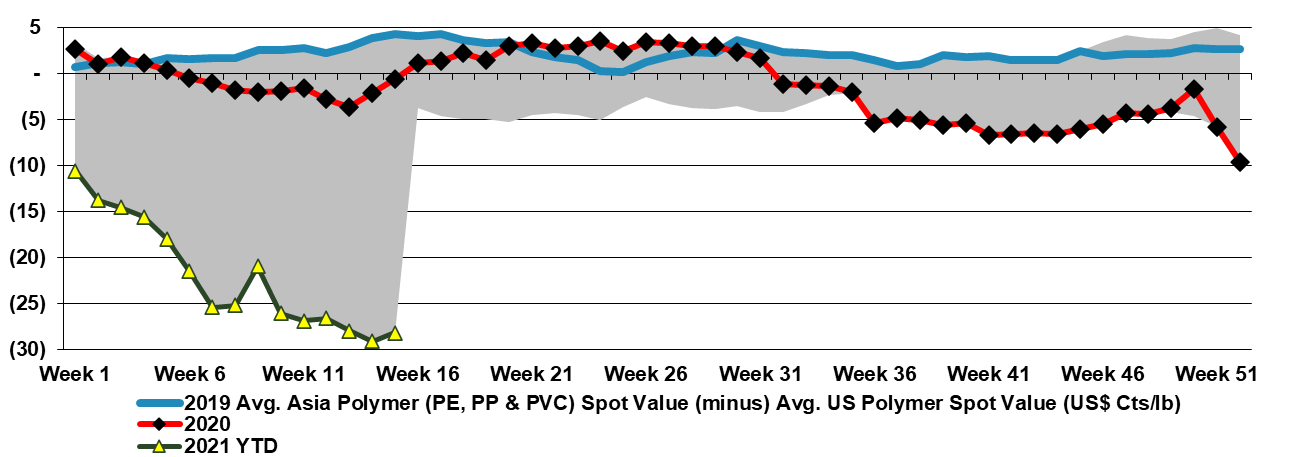

The price dynamic discussed in today's report and shown in the exhibit below looks unusual in a recent historic context and is unlikely to last very long, but it is worth noting that the recent history does not reflect the longer-term history.

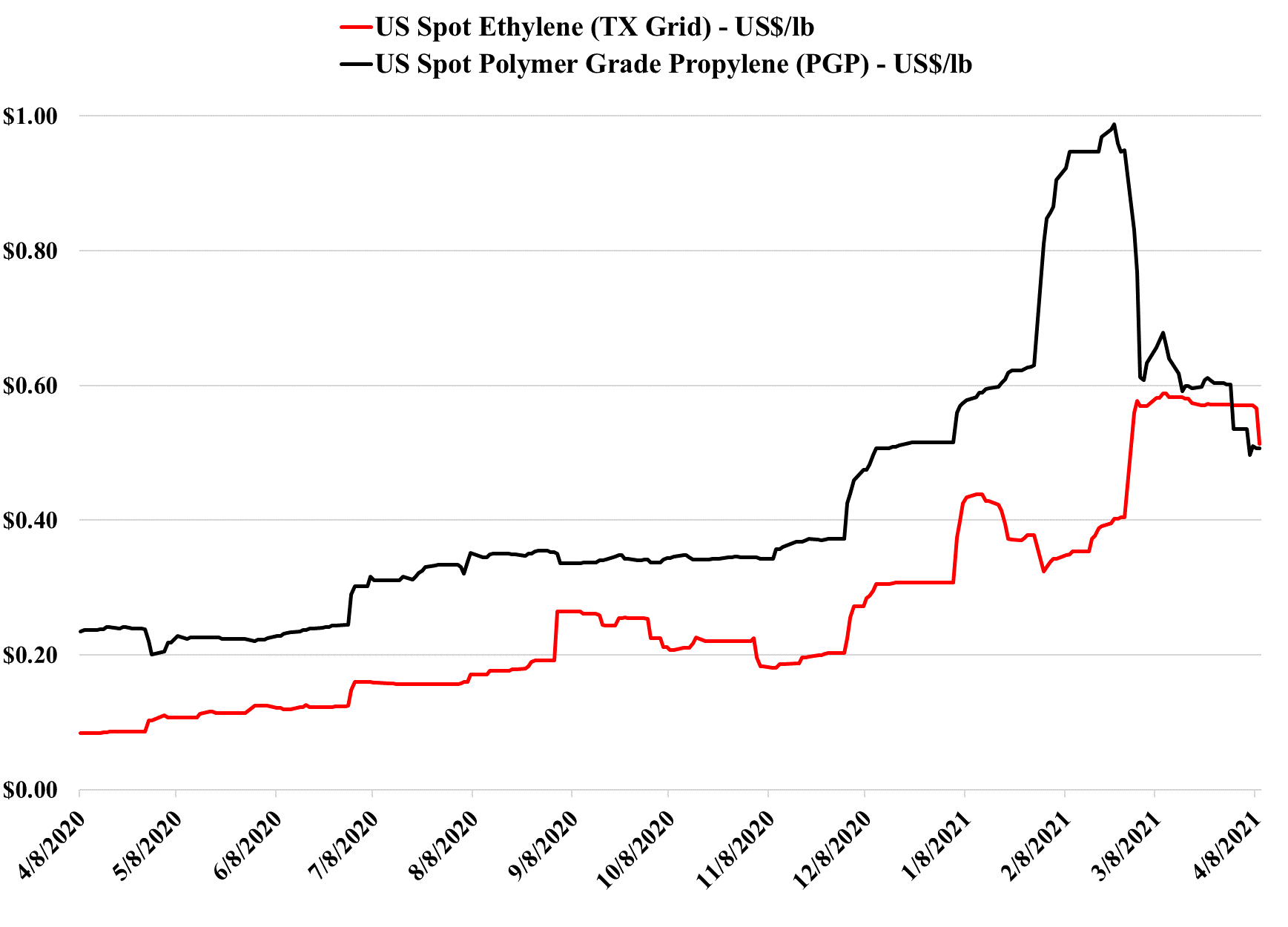

The propylene swing relative to ethylene in the US, as shown in the graph below is extraordinary. As we discussed yesterday it is a typical, albeit, tightly compacted commodity cycle, with the desperate shortage finding the incremental buyer who was more concerned about volume than price and the rapid supply and demand response that followed the peak in propylene pricing to correct the imbalance. The current price relative to ethylene does not look stable either and we would expect a reversal quite quickly – incremental propylene production from PDH is based on a higher cost feedstock than ethylene today – propane prices are higher than ethane prices, and while the volatility may remain in the relative price, we would expect to see propylene pricing rise back above ethylene again, fairly quickly. If polypropylene prices follow propylene and start to reflect a discount to polyethylene, that could also drive some polymer switching at the margin, which would help propylene relative to ethylene.

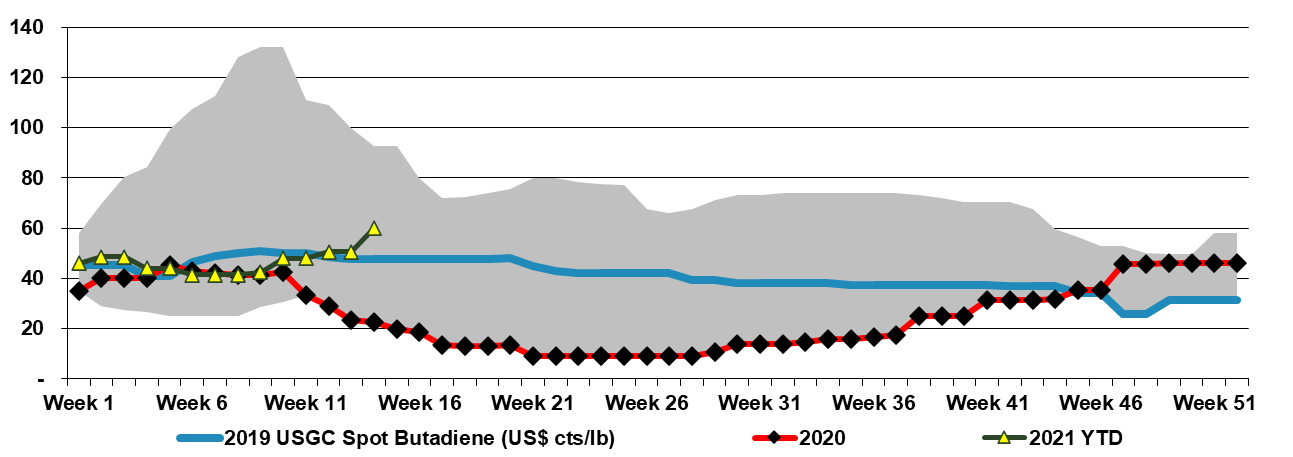

Last week we talked about the robustness of the US propane market and the China PDH headline is another example of offshore propane demand that we believe will keep US propane prices high, and probably high relative to ethane. This will mean that ethane stays favored as an ethylene feedstock but it will keep US PDH costs higher than they have been over the last 5 years. With propane and naphtha staying out of US ethylene plants we are seeing strength in butadiene, as domestic demand picks up and production remains constrained. Butadiene could see price support for some time as the ethylene economics are unlikely to change, especially if we see more Permian output in 2Q and into 2H 2021 as this will keep ethane supplies high.

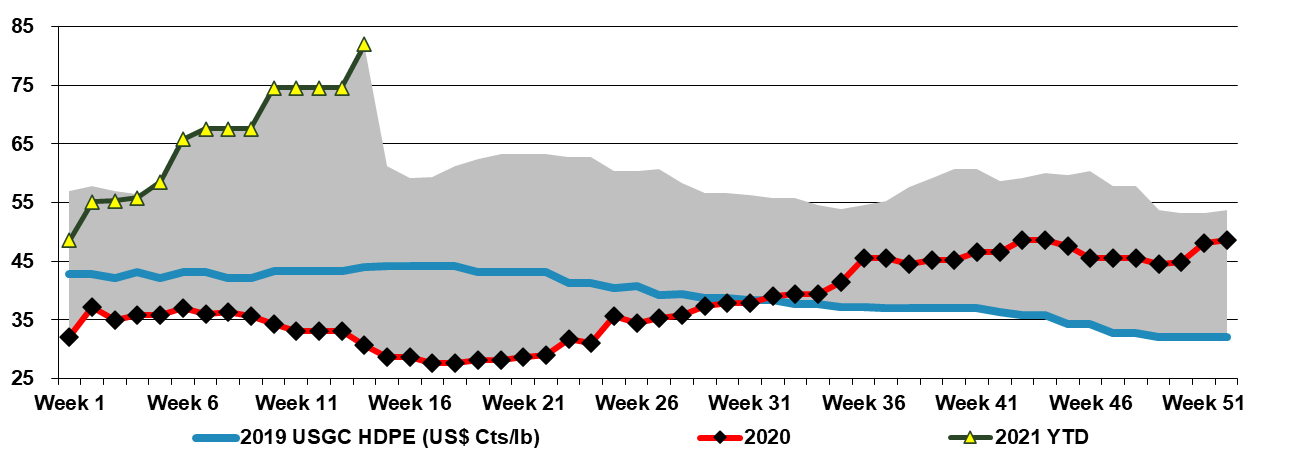

The fall in Chinese imports is not a surprise given the significant capacity additions over the last 6 months. There is an additional wave of investments planned for the next 6 months and we could see imports fall further as the year progresses. Even with strong demand growth in Asia and other parts of the world, this could leave the major exporters – the Middle East and North America with surpluses, although that is not evident today. Prices continue to rise for polyethylene in the US (see chart below) and Europe, partly because of the lingering impacts of the freeze, but also because apparent demand is high. This is going to be a tough year to call as we expect to see the supply chains over-compensate for the problems that have existed since the last quarter of 2020 and chain inventories to build. This could add several hundred basis points of demand in 2021, masking the new capacity in China and the theoretical oversupply that would exist if all global facilities were operating. This could set up 2022 for disappointment, and impact the longer-term supply/demand balance negatively, as the high profits of 2H 2020 and 2021 could encourage more investment such as the ones highlighted by SABIC, and India.

We note the increasing news on more geographically diverse investments in battery manufacture – see the Canada headline below. With the Intel chip investment in the US and battery investments all over the world, it is very clear that the automakers no longer wish to be so dependent on imports from Asia. In our Sunday Recap (Ship to Wreck: And The Supply-Chain Challenges Continue!), we discussed the possibility of a major wave of manufacturing investment in the US, with some but only a little marginal help from the Biden Administration. The consumer and retailer demand is there for more US content and the supply issues over the last few months have only increased the level of interest in having more local production.

Two thoughts that we published on Sunday:

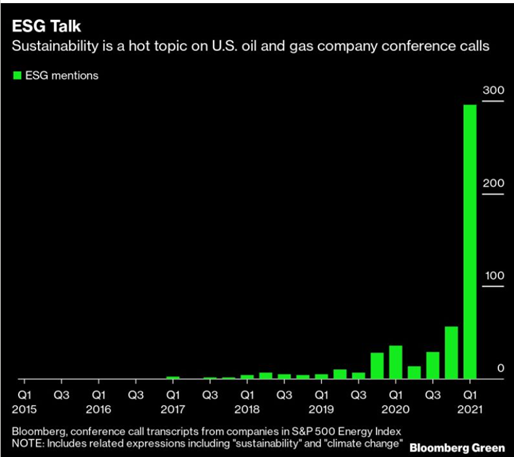

- The buzz acronym of the year is ESG, as clearly shown in the chart – and we believe that it will become increasingly difficult to get any new investment in the US (and Europe) off the ground without a robust climate-friendly plan, focused on energy use, the product life-cycle and emissions and waste disposal.

- We saw NextDecade strike a deal with Occidental last week to capture and use the carbon dioxide associated with its delayed LNG facility in Southeast Texas. The plant has all of its regulatory approvals and we believe the move was to satisfy some of the potential LNG customers for the facility, who are showing concern around the large carbon footprint of natural gas liquefaction. NextDecade’s move may provide regulators with a precedent as they think about new US investments.

- We should also not underestimate the pressure being placed on investment banks by their stakeholders when it comes to lending standards, and any new US project that requires debt financing (so any project of size), will find that their potential lenders are as tough on them if not tougher than regulators when it comes to environmental footprints.

- This could be good for the chemicals and plastic industry in the US and it would most likely increase domestic demand and make the industry less reliant on exports. Chip manufacture requires many chemical inputs from substrates to photoresists to industrial gases. Many of the other manufacturing opportunities would also consume chemicals and plastics:

- Auto parts

- Household goods

- Medicines

- Packaging or all of the above and other products

- The facility constructions would be good for building-related products such as polyurethanes and PVC.

Given the much lower margins that US polymer exporters are getting versus selling domestically today, higher levels of domestic demand would be a net positive.

A couple of headlines stand out today but the BASF capital markets day is probably not one of them. This is now becoming the norm; to provide an investor update tailored at focusing on clean energy and sustainability goals, and BASF’s expectations are not much different from others – there is a bold claim about 2050 and some harder targets by 2030. So far we have yet to see one of these presentations where the math is believable, and the investment targets in dollar terms all seem too low to meet a net-zero goal. To be fair, it is hard to know what will happen in 5 years, let alone from 2030 to 2050, and we would doubt that anyone has a good estimate today. BASF and others will likely end up spending multiples of what they currently project, but this may not be a bad thing – much of the spending will be backed by incentives (or encouraged by penalties) and all of the spending will be good for jobs and economic growth.

It remains very interesting to us that despite the apparent major shortages of chemicals and polymers in the US, the industry continues to operate at rates below those of a year ago, according to the ACC. We fully understand the Gulf Coast swing in February and are surprised that it was not worse, given the extent of the shutdowns we have been monitoring – March should be bad also because many of the shutdowns extended into March. While the bulk of the US chemical industry is in the Gulf Coast – as can be seen by the Gulf Coast influence on the “total US” bar, why production remains below 2020 levels in other regions is a little surprising. Granted, February 2020 was not impacted by the Pandemic and the economy was strong and demand for materials high, but with the import issues of the last 4 months and the move by US manufacturers and retailers to source more product from the US, we remain surprised that regional chemical production outside the US Gulf has not at least matched 2020 levels.

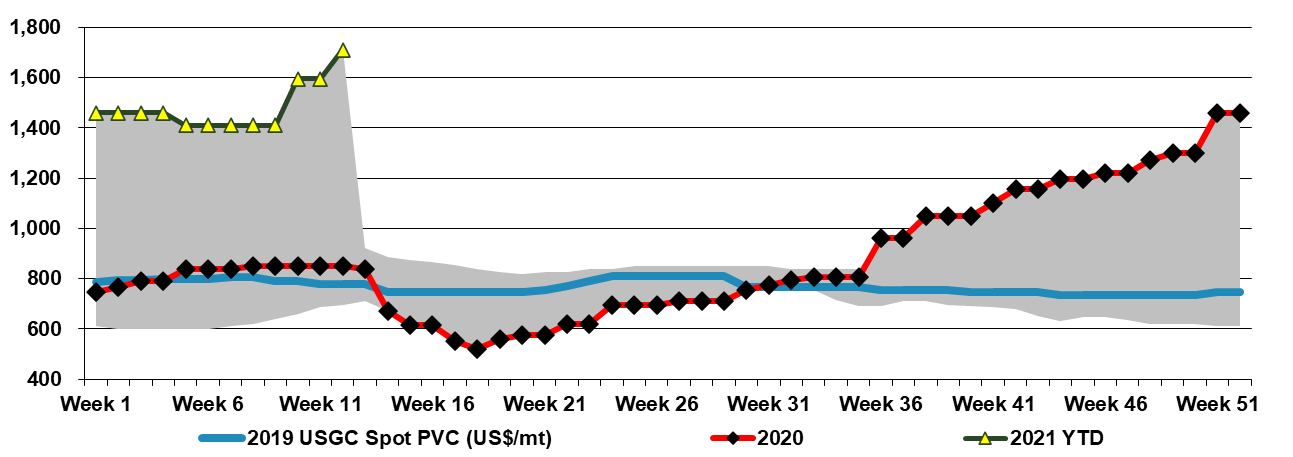

Asia polyvinyl chloride (PVC) prices reflect a five-year low relative to US spot levels, but both price points reflect five-year highs on an absolute basis.