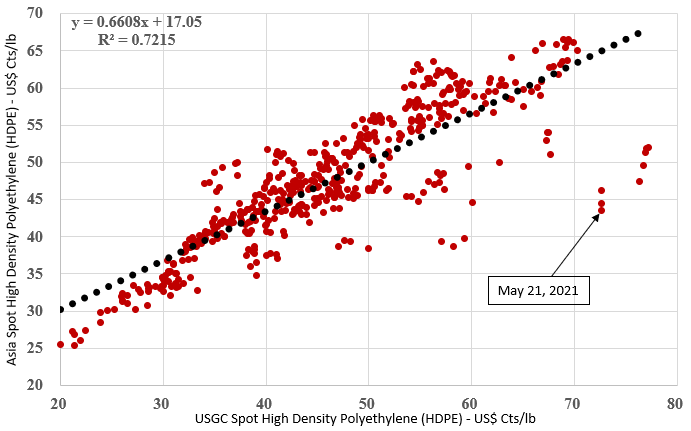

Scatter charts with significant outlying points are always eye-catching and the exhibit below is no exception. The extremes of the chart are interesting as they show that when US polymer prices are low, Asia generally trades at a premium, and when US prices are high Asia trades at a discount. But today’s discount is several standard deviations from the norm, and it is too compelling a trade to ignore. If the US was short polyethylene we would be less focused on this arbitrage but that is not the case. Unilateral decisions from US producers to keep production in line with contract demand could maintain pricing support, but the competitive disadvantage that this places on US consumers – especially in durable applications (where the polymer is a larger part of the finished product cost) is significant. It is also a major cost headwind for the packaging companies in the US, and tough to pass through in most cases on staples and household products, because of the buying power of the major food and drug retailers.

Referring back to our daily report today, can polyethylene hold on? Despite the strength in US polyethylene prices and the aggressive attempts by sellers to hold on through the quarter, there are couple of key factors working against them. Local supply may be tight in the US, but as we discussed yesterday, ethylene is moving towards a global surplus that could push US prices even lower than we are seeing this week and as the chart below shows clearly, how large the gap between Asian ethylene prices and those in the US. Unlike ethylene, polyethylene is harder to trade in to the US, partly because it is an unusual movement and the shipping costs are high, as would be the cost of getting from a US port to a consumer, but partly because US consumers serving the higher end of the market are very grade and quality conscious and would concerned about product quality and the risk of sending something to their customers that does not do the job as well.

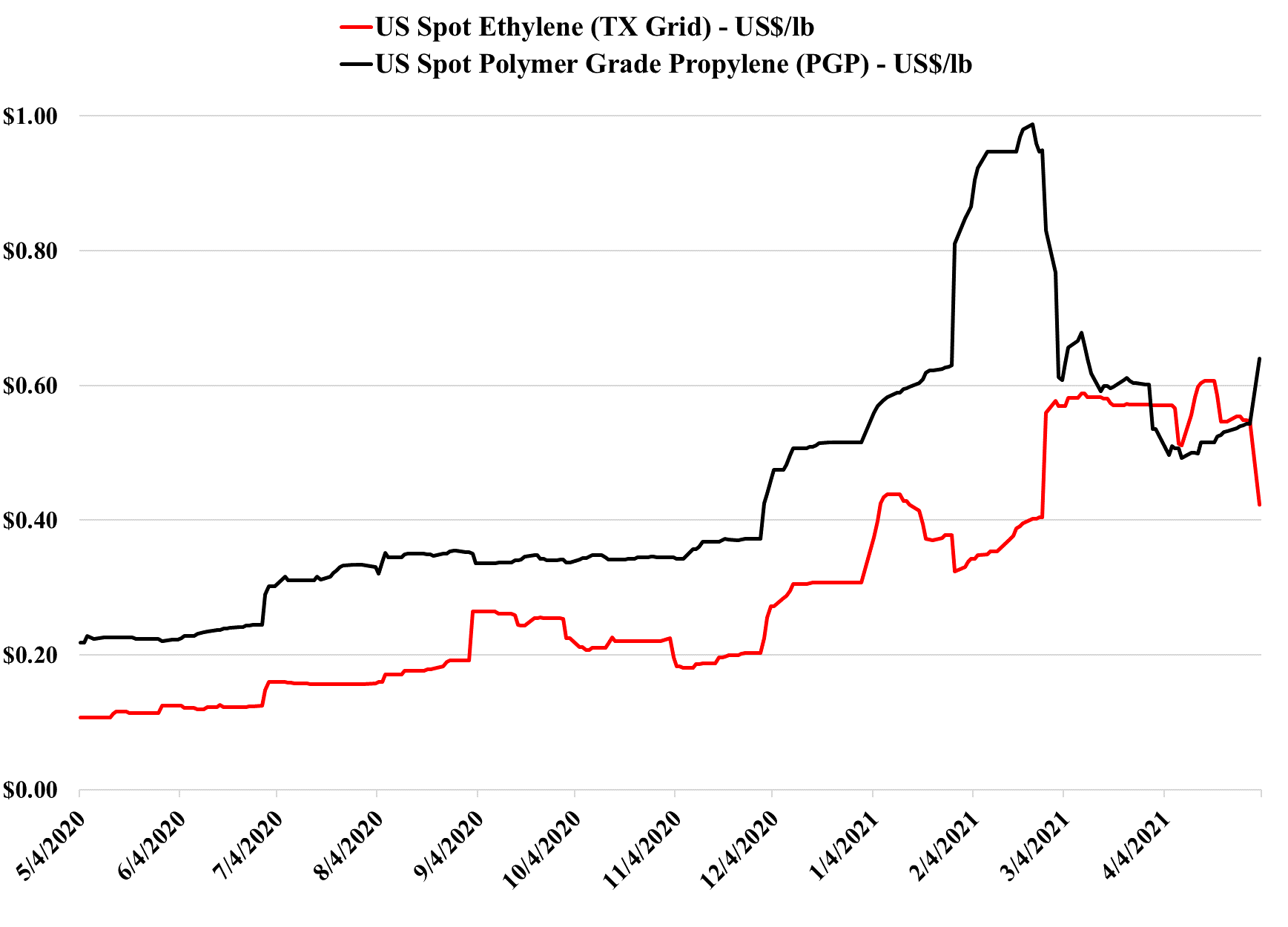

The movement down in ethylene in the exhibit below is significant, as it begins to show the overhang that the US has with ethylene supply. The price has to fall further before ethylene is likely to find any interested spot buyers outside the US (note that the US exported significant volumes of ethylene from November through January). The more important question is whether the weaker ethylene price starts to undermine derivative prices, especially polyethylene. We believe that will happen either late this quarter or early next, but only when US polymer buyers are satisfied that they have adequate inventory to meet what has been surprisingly strong demand. For more on this see our daily report.

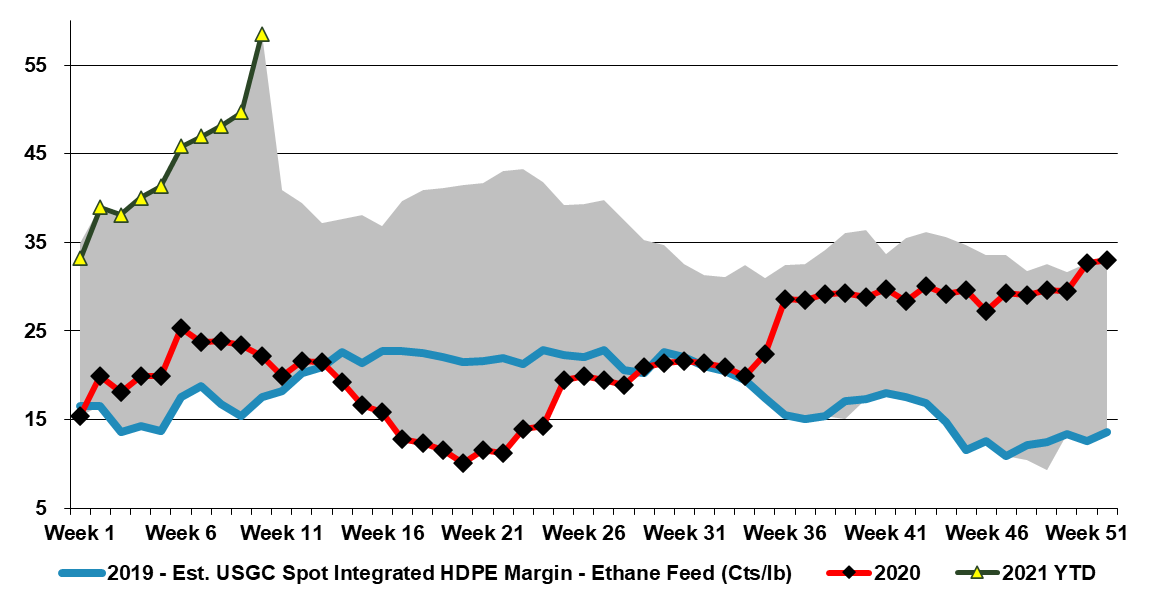

We still believe that there is a good chance that 2Q 2021 is the peak for polymer profits in the US and Europe, but it very unclear how severe the downside could be, given the growth potential. Seasonal turnaround will keep markets more balanced in 2Q, and the major uncertainty beyond that will be weather in the US. A series of storms like last year could hold the market up through 3Q and into 4Q, but an absence of any weather events could expose US surpluses quite quickly, especially for ethylene and derivatives. The new builds in China have focused on ethylene and polyethylene (and some glycol), propylene and polypropylene, and PTA and PET, and this is where the potential weakness will emerge. There has been some new styrene capacity and that is also a vulnerable segment in our view. PVC, acetic acid, and large parts of the polyurethane chains look much more balanced to us and we have more faith in the projections being made by companies like Celanese, Olin, and Orbia than we do the major polyethylene producers. See today's daily report for more details.

We are experiencing a perfect storm for chemical pricing. The supply chain dislocations are causing buyers right down the chain to think about both supply routes and how much inventory they should hold (we would expect a general working capital increase across manufacturing and possibly retailing over the next 6 months – price and volume-driven). The risk of over-buying is high, and, for example, plastic buyers may be pressing all suppliers for contract maximums, in the hope that one or two can deliver. Things will change when four or five deliver in the same week – unlikely before late 2Q 2021 in our view. When you add the supply chain issues to rising oil prices and the US base chemicals and polymer production issues, you have a global tight market that is expressing itself most aggressively in the US and creating some of the extraordinary trends in the charts we highlighted in today's daily.