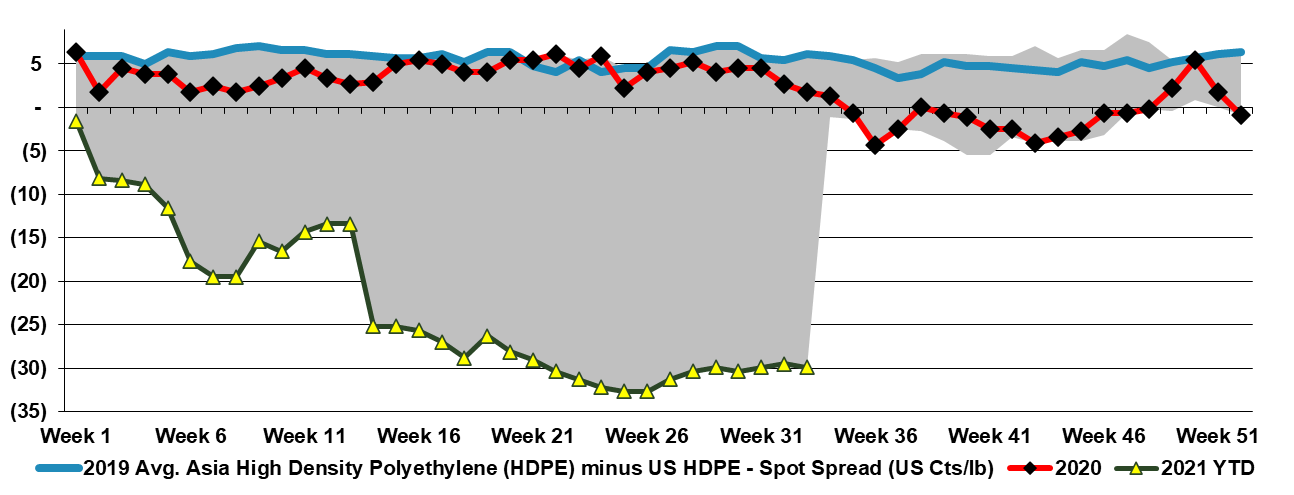

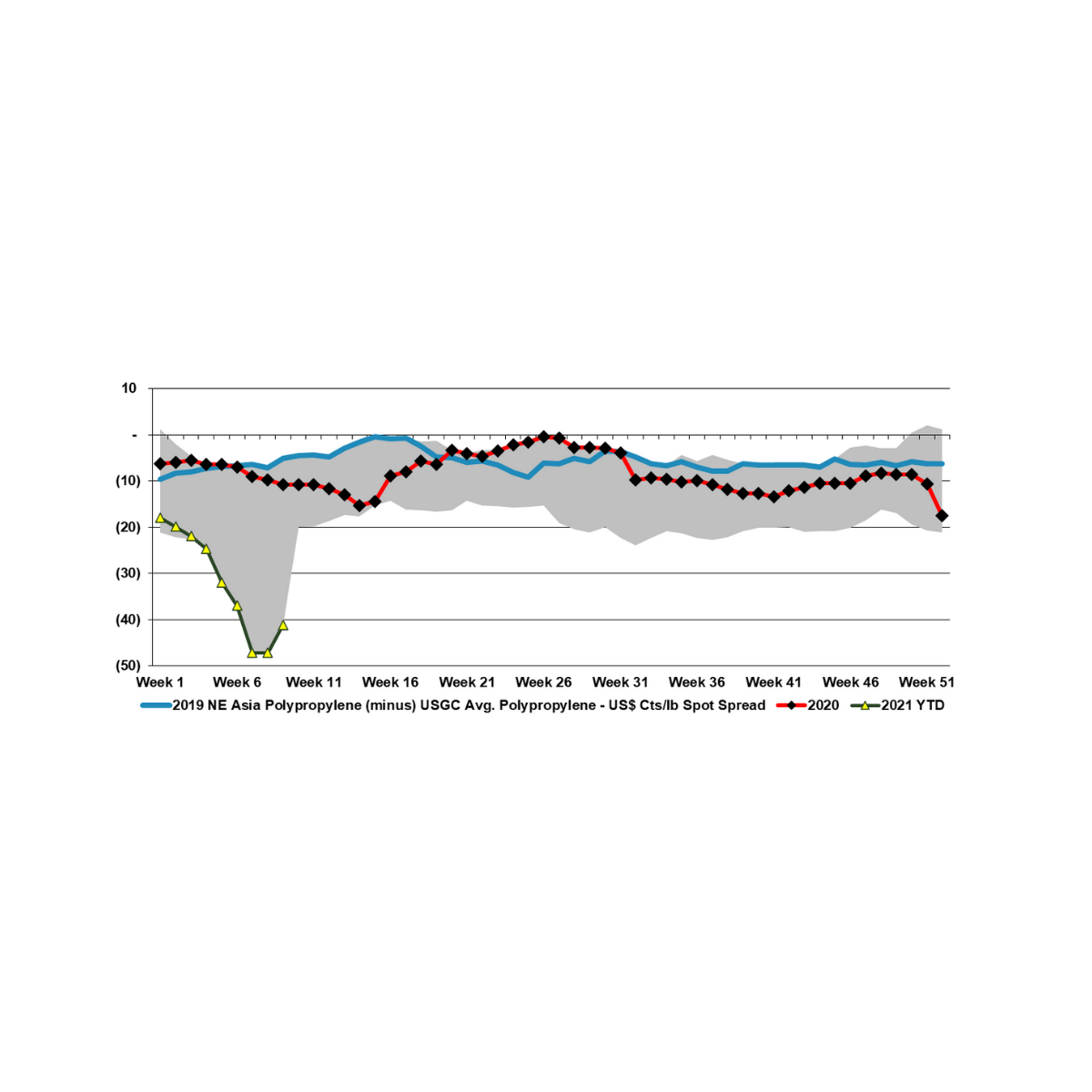

The chasm between US and Asia polyolefins prices remains wide, close to a 5-year high for polyethylene and setting new highs for polypropylene. The polyethylene arbitrage is not large enough to encourage US imports – first Exhibit below – largely because of the very high container rates from China.

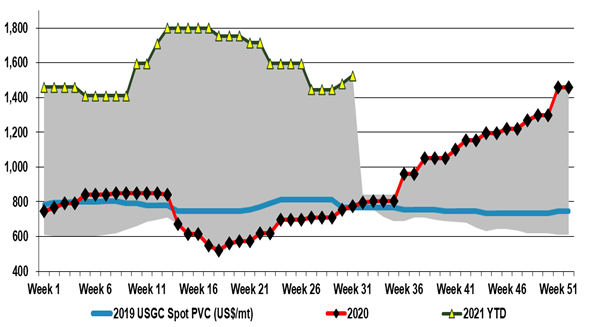

We are seeing some of the same dynamics in PVC that have been prevalent in polyolefins this year with some weakness in Asia – although not as much as we are seeing for polyolefins - while markets in the US and Europe are finding enough support for prices to go back up again. As with other polymers, any possible arbitrage between Asia pricing and the West is quickly consumed by the higher container rates. PVC has seen less capacity added over the last few years compared to other polymers and while it has not seen much of a boost from the change in consumer spending patterns around packaged goods and durables (as it has more limited exposure to packaging and durables), it has benefited from strong housing demand and some initial infrastructure spending – with more to come around the globe. The blue sky scenario for PVC would be one in which some of the growing clean water issues that are emerging in many parts of the world move more to the front burner as PVC would be a major beneficiary on investments in desalination for example or simply from water infrastructure upgrades.

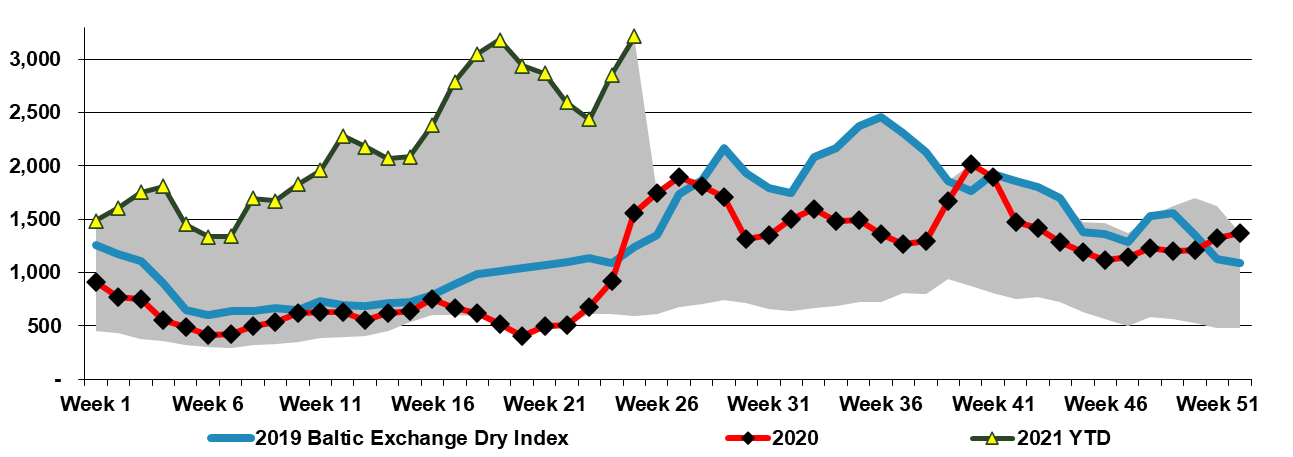

See today's daily for more on this, but while the freight rate moves are more than likely going to correct to a degree at some point, their continual escalation has multiple implications for the chemical and plastic industry as they are most impactful on cheap imports from Asia targeting low-cost furniture, appliances, toys, and household goods where the base cost of the product is low and the move from $3,000 to $10,000 per container wipes out any advantage of manufacturing offshore.

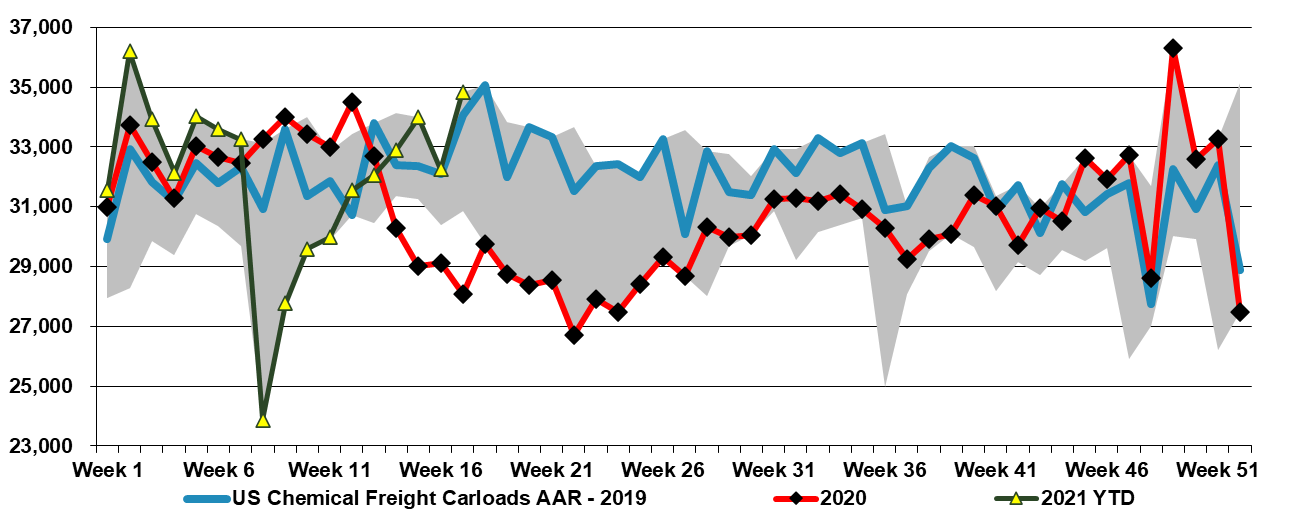

The Dow announcement yesterday speaks to a much larger issue within the investment community in our view, which is that research fees have come down so much over the last ten years that the sell-side gets paid very little for doing any real research. We talked about the upside in 2Q for the commodity polymer producers for months. Still, we know that we cannot get paid for maintaining the models needed to get to the numbers with enough confidence to publish estimates. The buy-side does not have the budget. In the past, as sell-side analysts, we would subscribe and talk to price discovery consultants, such as the predecessor companies of IHS (now in the middle of an acquisition by S&P) and CDI (in the middle of a merger with ICIS). This data and these dialogues would allow us to adjust earnings estimates during the quarter and keep up alongside our other work (e.g. corporate marketing/roadshows, etc.) as analysts. There is enough data in our weekly report – published each Monday to do this for many companies. (See an example in the chart below). Today, IHS has made its service so expensive that it is difficult for sell-side analysts to justify the cost when they are not getting paid by clients for real, fundamental research. The JP Morgan alleged base fee for research for an entire platform would not cover 25% of the IHS subscription cost for olefins and polyolefins data alone, per our estimate. Plus, all the merger activity at the data providers is causing some to question quality. The result is limited mid-quarter analysis from the sell-side and moves like Dow’s so that they can have realistic conversations with investors. In the case of Dow, it was to get the message out ahead of the Bernstein Conference.

While we see some residual strength in several markets, and note the Dow push for higher MDI pricing, the European ethylene price move lower may be a more important red flag. Rail-car data below shows that logistics are getting back to normal in the US. The upward momentum in US polyolefins spot pricing is losing steam and prices in China are weaker. Read more in our

Thursday Daily Report

The focus today should be on the data suggesting that the US is importing both polyethylene and polypropylene, something which the nominal US supply/demand balance for both products should not support. The US has a material surplus of polyethylene capacity (almost 30% of US polyethylene capacity is surplus to US needs – on paper) and the start-up in the Fall of last year of Braskem’s new polypropylene units in Texas should have pushed polypropylene into surplus and the message from Braskem before start-up was that the company expected to export as significant volume. So, what has changed? Anyone reading our daily reports will have seen us highlight the development of a reverse arbitrage for both polymers’ pricing versus “normal” for many months, this is not news. What is news is that there is not enough flexibility in the system to meet US demand at attractive enough prices to avoid opportunistic imports. However, some of the imports likely are from companies with capacity in the US and other countries trying to balance their global portfolios. It is also possible that polymer consumers who are less concerned about specific grade quality – i.e. those that are already bidding up recycled polymer prices are importing opportunistic volume to lower their average purchase prices.