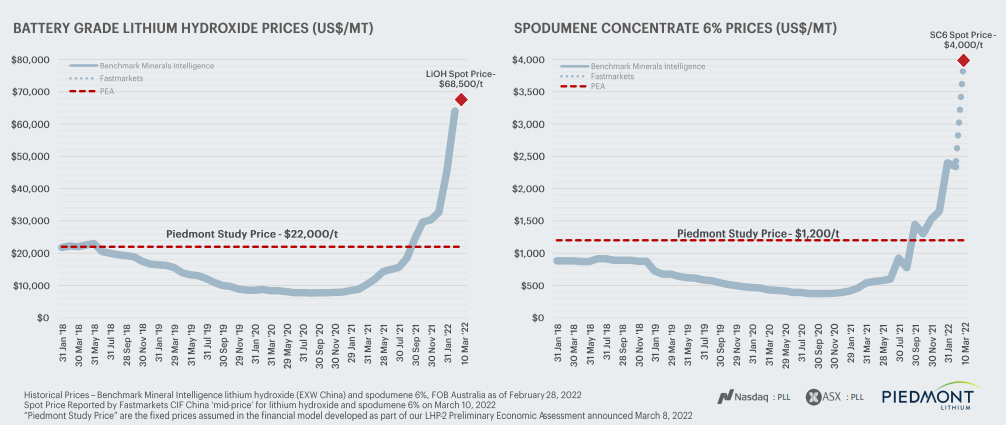

Could what we are seeing in metals happen in chemicals and polymers? Over the last few weeks, we have seen already high metals pricing spike even further, both because of production shortfalls and because of expectation of higher demand, especially in the renewables space, as conventional energy prices have spiked. We show a lithium example below, but note that after chaotic nickel trading last week and a halt to trading, the market has made some attempts to reopen this morning with renewed problems.

The very strong Wacker results and bullish outlook make sense for a company very exposed to the solar industry. The solar companies themselves may be struggling to make money, but their demand is very high and their thirst for raw materials equally high. In bp’s annual review of world energy, the company is forecasting a three-fold increase in the rate of annual renewable power investment and all of this will require more materials – setting up polysilicon suppliers like Wacker very well. The negative for Wacker, of course, is the high European footprint and the current increase in energy costs in Europe. Given the strong demand for polysilicon, Wacker should be able to raise prices – adding to the woes of the solar panel makers. See more in today's daily report.

The Huntsman activist defense presentation highlighted below does a very good job of explaining why Starboard is focused on a set of concerns that the company has already addressed and while we would generally not comment on something like this, we agree with Huntsman’s assessment that the proposed Board changes bring nothing to the table. Where the Starboard activity may help is improving Huntsman’s communications, as while the company has done a good job, in our view, of repositioning, it has done a less good job, until now, of communicating what the changes mean. The presentation linked below does a much better job than anything we have seen from the company in the past. To be fairer to Huntsman, the chemical industry has always had trouble communicating strategy shifts and portfolio transformations to stakeholders and there have been several instances of good stories not turning into good businesses – Eastman had some false starts in the past but has not been alone with these problems. It often takes some time for investors to believe in a new business model and this is where good corporate communications strategies can help. This presentation is a good start for Huntsman.

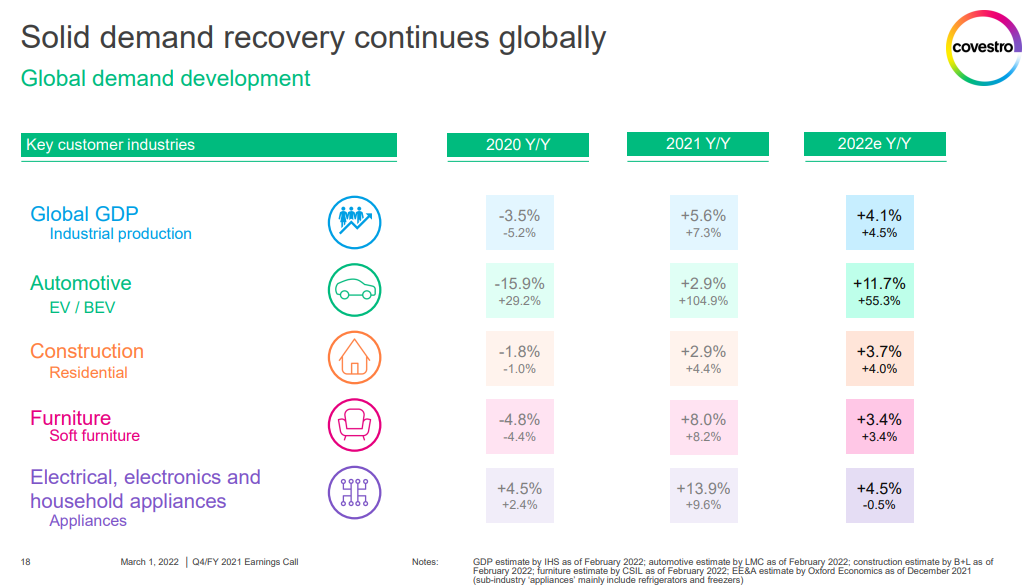

More confirmation from Covestro that global demand growth is strong, supporting reports that we have seen from most companies over the last few weeks. Some have struggled with raw material cost squeezes and either late attempts to raise prices or pricing lags in contract agreements, but almost all have pointed to very strong demand outside of auto OEM. We have questioned how much of this strong demand is inflation-driven, but it is very hard to tell as the last time we had significant inflation we did not have such an interwoven global supply chain as we have today, and consequently, it is harder to assess how much pre-buying may be going on, not because of fear of higher prices but because of fear of supply. Note that we have at least two European automakers (VW and Renault) shutting down facilities this week because they cannot key parts from Ukraine. This adds to the already problematic path for parts from China as well as the semiconductor shortage. If everyone is looking for a little bit more it would explain the very high 1Q 2022 demand that all are talking about and it likely means that inflationary pressures will continue as chemical and polymer makers try to make more, against a backdrop of higher raw materials and find it easier to increase their prices because their customers are as concerned about availability as they are prices.

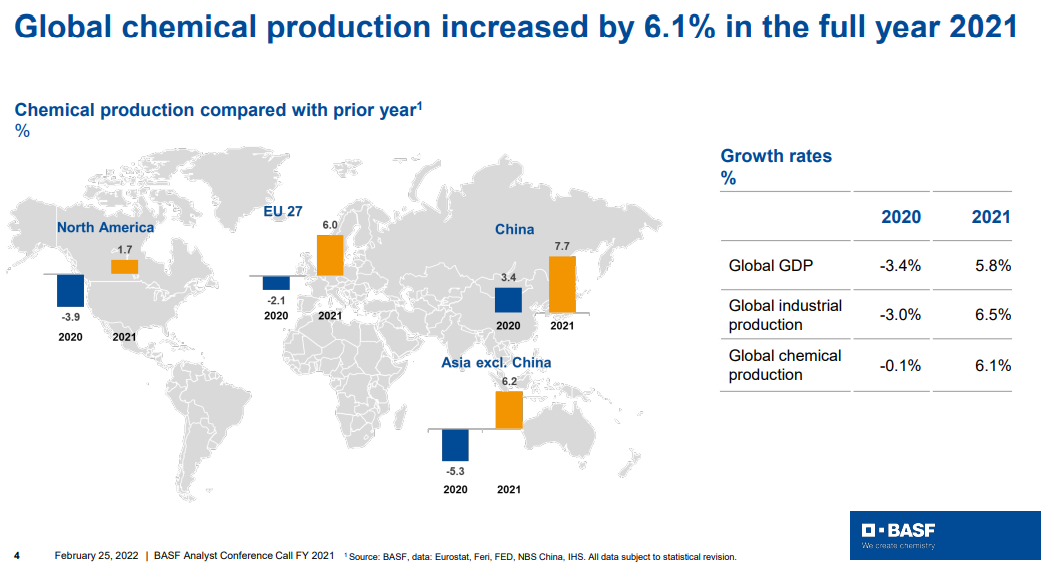

Fear of shortages is the one factor that is most supportive in terms of helping to push through pricing and the events in Europe and their associated impact on energy prices should be all the support that the chemical and polymer industry needs to push pricing through that will cover cost inflation. Buyers of raw materials and intermediate products will naturally look to buy a little more than they need in the near term, both to ensure that they get something ad to try to build a bigger inventory cushion. This will have the effect of pushing apparent demand higher, making the pricing initiatives easier. Few will push back on pricing if their primary concern is availability. Looking at the BASF results summarized in the chart below, demand is already very robust and this will lead to higher utilization rates and higher volumes for chemical producers as well as high pricing. The commodity producers are likely more interesting here as they can move prices much more quickly than the specialty companies who might see margins squeezed over the next couple of months. None of this is good for inflation. See more in today's daily report.

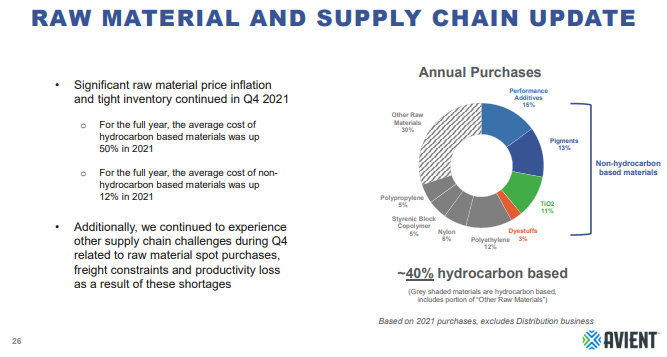

As Avient and the linked paint article remind us, there are sectors of the US chemical industry that rely on imported products – in these cases pigments, and the supply chain challenges and logistic delays have caused production problems in the US and price increases in 2021. The automotive segment of the paint industry has seen lower demand because of the auto OEM production slowdown, and pigment shortages and price spikes would likely have been worse if automakers had been running at full rates. There is no sense of impending relief in the logistic issues as we go through 4Q earnings reports and we could continue to see issues for a while. This should be good for US-based pigment suppliers, but while Chemours, Venator, and Tronox all have capacity in the US, they also have capacity outside the US which likely faces some supply chain challenges.

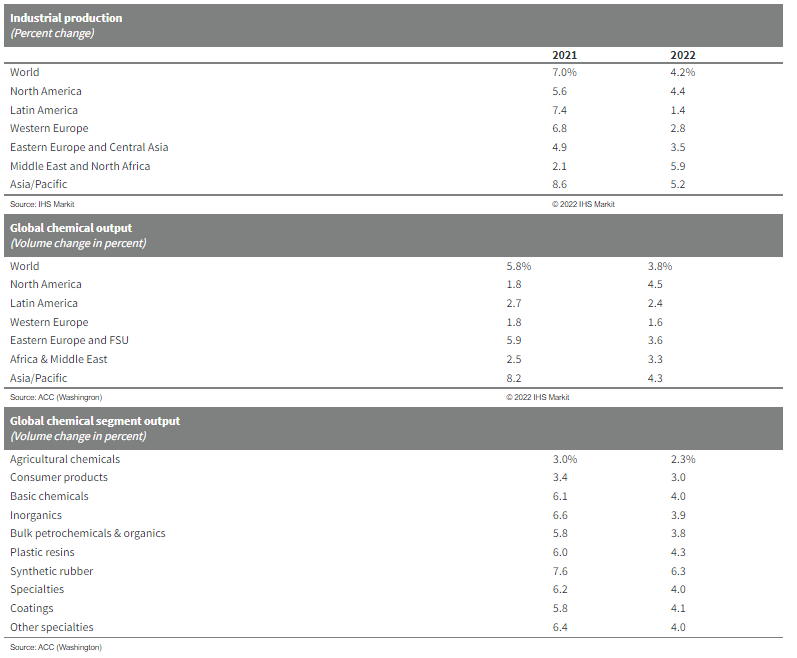

The jump in expected US chemical production in 2022 versus 2021 and the more anemic growth in 2021, is in part due to new capacity in the US but is likely more a function of lost production in the US in 2021 because of the February freeze and the hurricane that hit the New Orleans area. These two weather events, especially the freeze, cause significant production cutbacks, and not only would production have looked better in 2021 without them, but the inventory decline shown in Exhibit 1 in today's daily might have been less severe. IF we assume that climate change is causing more severe weather, then perhaps it would be prudent to build more unplanned downtime into forecasting models and on that basis perhaps the production growth forecast in the exhibit below is too hopeful. However, if you model more unplanned downtime you are inevitably going to end up with a more volatile market as available capacity will swing around the forecast average by a larger amplitude, which would make production and inventory planning more complicated.

We are seeing pockets of real demand strength in some areas of chemicals, such as building products, and this is allowing producers to push through price increases to reflect higher costs and most likely add some margin. In other areas where the fundamentals might not be quite as supportive, we are still seeing attempts to pass on higher costs. Sika has supported what we have heard from many over the last few weeks, which is that the building products chain remains tight, as demand is strong, capacity is running hard and logistic issues continue to cause problems in some cases from a raw materials perspective and in others from getting finished products to market. Where there is limited ability to increase supply, those selling into the building products space are likely to make more money as they should have strong pricing power – in the US chemical space, we would favor Westlake as a potential big winner from this trend, but Huntsman should also be on the list.

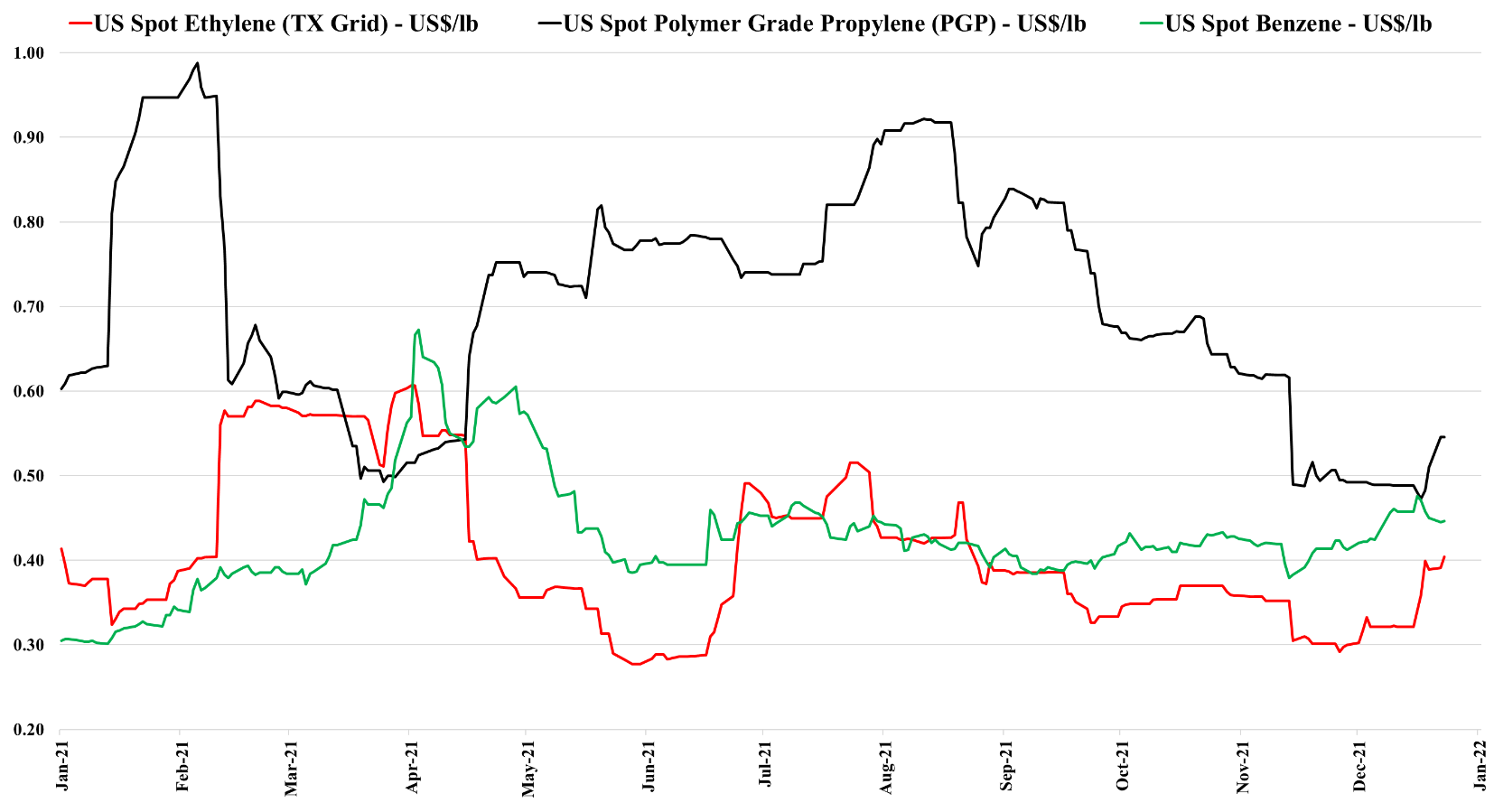

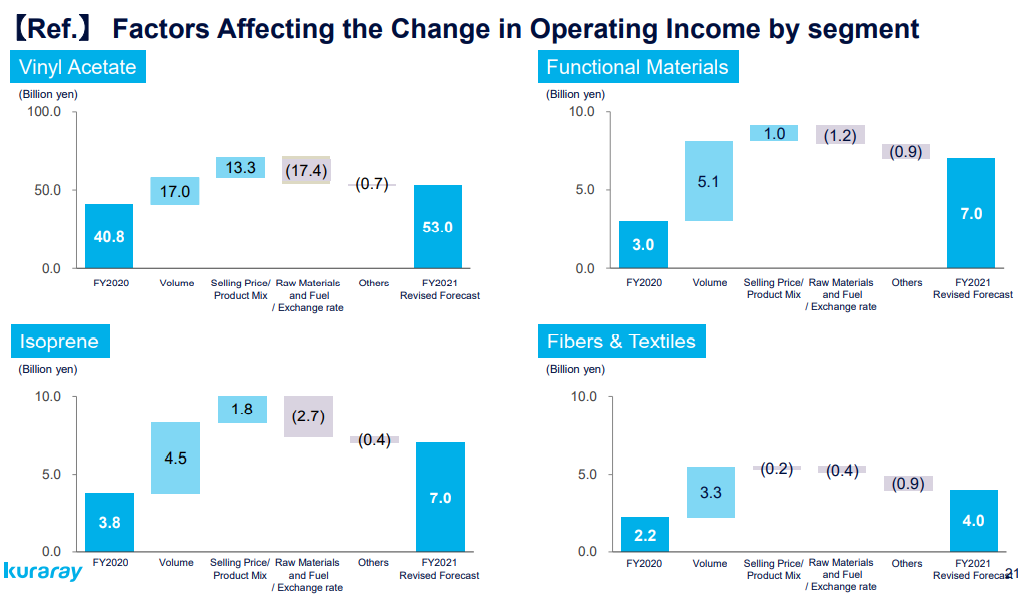

The 2Q volume driver of Kuraray’s earnings recovery was substantial, partly because end-market demand is strong and because this more mid-stream and specialty portfolio has significant operating leverage, much more than you would see from the commodity producers. We find this as a notable downstream sector trend to keep in mind. As seen below, increased selling prices are an important driver of Kuraray full-year profit growth expectations, but the volume piece is the most critical component, in our view. As discussed in our daily report today available in LINK, we continue to see volatile but elevated basic chemical prices.

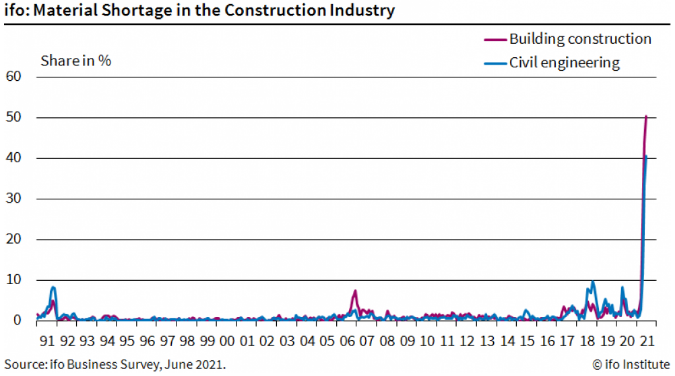

The German materials shortage chart below is certainly eye-catching. There is nothing even remotely close in 30 years of history. We see this as further confirmation that we should continue to expect high shipping rates and congested ports until surveys like this show significantly better results and it is also further supportive of inflation. While it is extremely difficult to forecast from here, we would use the pendulum or spring metaphor – the further you pull either in one direction, the further they swing or spring back. The current dislocation is so extreme that everyone in the chain is likely acting instinctively and working to find greater supply and greater supply security. At some point, both end-demand and demand to fill inventories will normalize – either back to trend or back to a higher trend, but the inventory build piece will end and we will either get a gradual retreat in the scary data – such as the spike in the chart below – or we will see an equally quick collapse, at which point pricing will likely take a hit down the chain, with basic chemicals particularly vulnerable because the world has been adding substantial new capacity over the last several years in the US and China. More investment may be needed to keep up with higher trend demand in many intermediate or end-products that consume base chemicals and this could keep pricing supported, but basic chemicals and polymers look especially vulnerable to a reversal in the supply chain build we have seen for the last 9 months. For more see today's daily report.