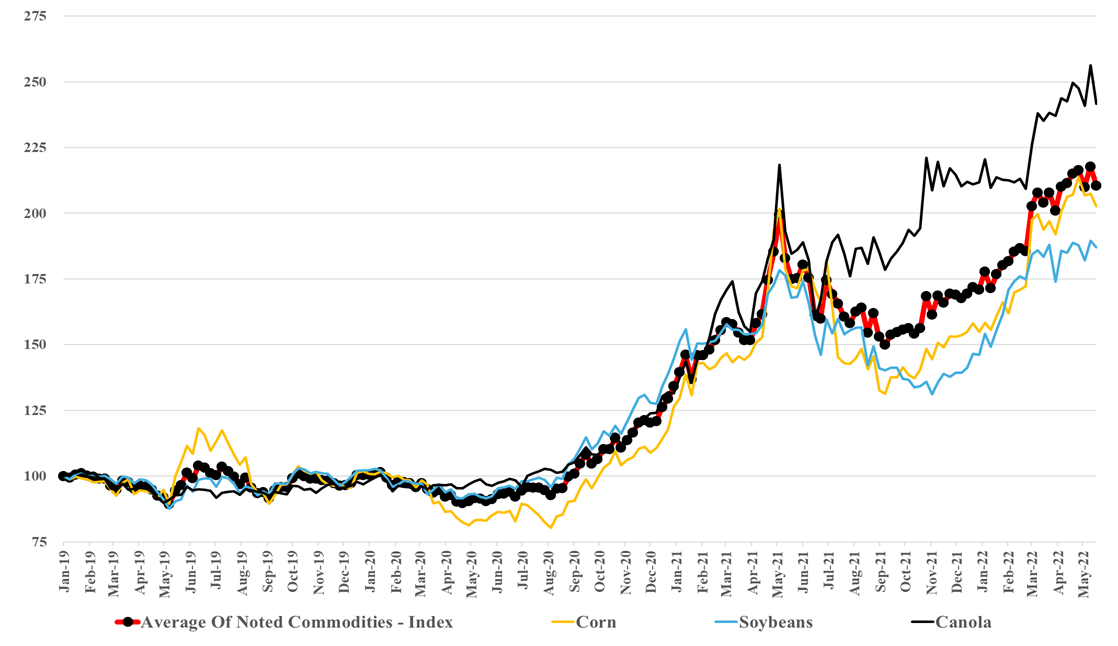

We have focused on agriculture this week with the ongoing announcements of new ammonia projects and the commodity crop prices and the overall index shown below are some of the key drivers of the activity in fertilizers but also are helping Ag equipment demand and we discuss the Deere results in today's daily report. We do not see how the trends in the chart below correct quickly and the profit through the farming, fertilizer, ag chemicals, and equipment chain should remain high in the US, at the expense of the consumer-facing high food prices (second chart below). We would need some coordinated medium-term policy to encourage moving more land in the US into agriculture, and this is especially necessary if we also intend to pursue bio-based fuels and materials. There has been much discussion around energy security over the last couple of months, but we think it is a much broader security discussion than just energy. Governments need to become much more accommodative around many aspects of production, food, energy, materials, etc. This accommodation can come with tighter emissions standards and emissions costs, but the primary objective should be to encourage more local production of many different things.

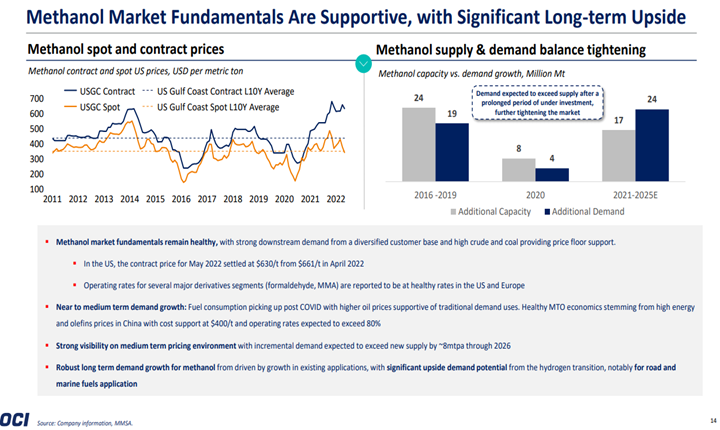

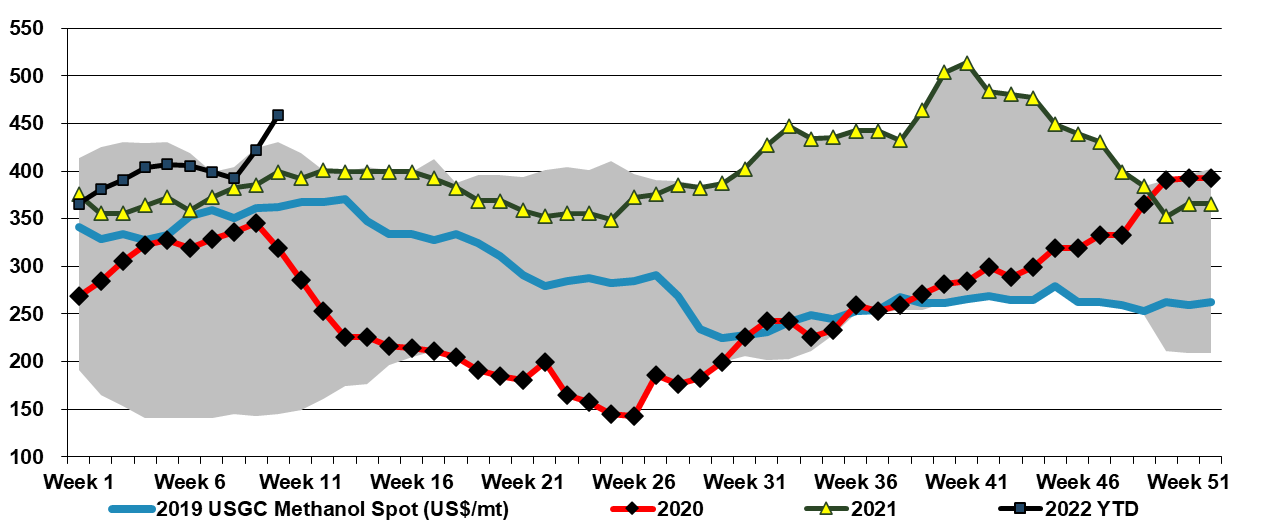

Today's apparent exceptions are in sectors very focused on energy security and transition, as we noted in our most recent Sunday Thematic, and agriculture, where crop shortages are driving up prices and demand for yield-enhancing inputs. In the OCI results below, we see a company doing well, despite having impacted assets in Europe. Still, we also see some potential upside in methanol as we head into the European winter, with the possibility that methanol is used as a fuel, essentially as a carrier for methane, and a workaround for constrained LNG infrastructure. As a fuel, it is not directly substituted for methane in any application, as it is a liquid, but some energy users might be able to adapt, and a $30 per MMBTU natural gas price in Europe can cause you to be quite creative. Of course, the methanol export opportunity for the US will depend on the US natural gas price remaining well below the price in Europe. For more see today's daily report.

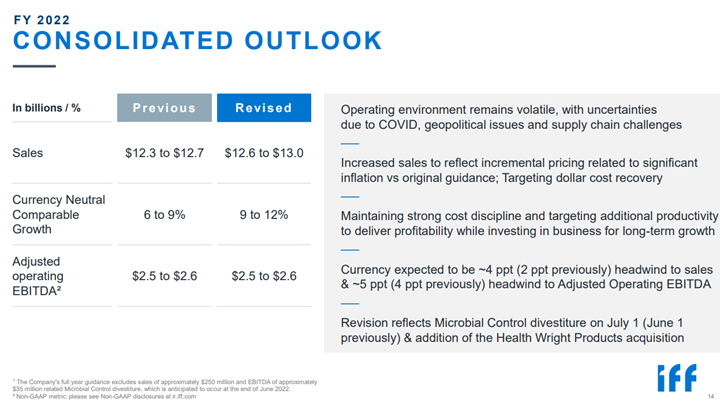

The pricing effect is very evident in the IFF results and projections, highlighted below. The company projected higher revenue expectations for the year but no increase in EBITDA with that higher revenue. We expect this trend to continue through at least the next couple of quarters, even if energy prices do not rise any further, as we believe that there is still some energy-related pass-through to come in many sectors. As the ammonia chart below shows, inputs in the agriculture/food industry keep rising.

Like many of the European producers, DuPont has taken a risk in our view by holding guidance flat in the face of inflation, weakness in China, and a potential further economic slowdown in Europe and the US. We struggle with what an alternative approach should be for DuPont and others, given that it would be challenging to map out a credible downside scenario today. What we would note, however, is that when things turn negative for the materials industries they tend to fall quickly and sharply. For all of the base chemical and specialty chemical companies what might upset things for 2022 are largely outside of their control, and it is hard to second guess cutbacks in customer demand until they happen, especially in an environment where all are looking at volatile costs from energy and consumer spending uncertainty because of inflation. For more see today's daily report.

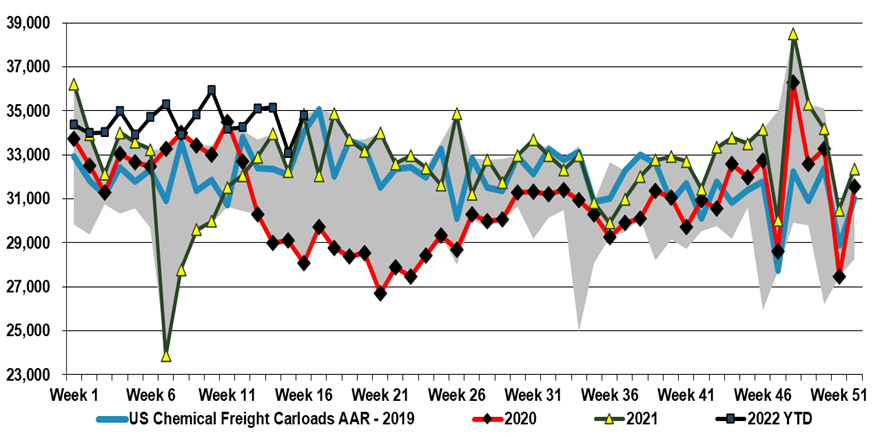

Chemical railcar volumes remain very strong in the US, despite some issues with exporting polymers, which has led to inventory builds on the coast, especially the Gulf Coast, and despite the implied consumer volume purchase decline in 1Q GDP estimates (sales grew but prices rose 500 basis points more than sales growth – suggesting an equivalent decline in volumes). As we noted yesterday, some companies closer to the consumer are indicating demand weakness and are more cautious about 2Q outlooks. If a higher than usual proportion of rail freight is moving into inventory, either at customers or stuck in rail cars – something Union Pacific has signaled – we could see a correction.

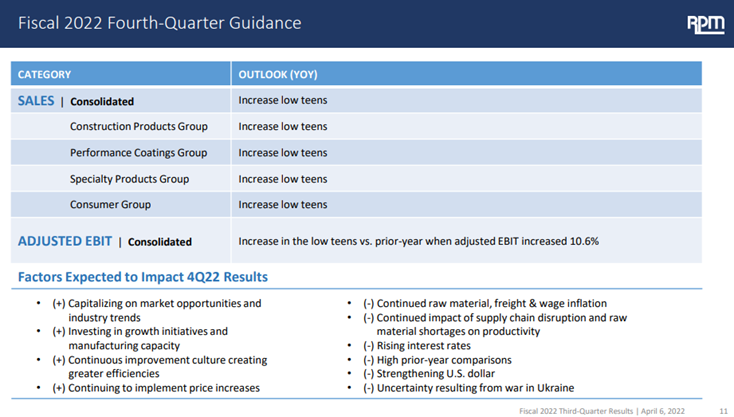

While we remain advocates of “stronger for longer” with respect to chemical demand and pricing in the US, the auto data does suggest that the US consumer may be cooling off a bit in reaction to higher prices and higher borrowing rates. Historically, the chemical industry has a habit of running headlong into a downturn while waving an “everything is great” flag, and the RPM results and outlook have a vague “deja vu” feel to them. We also note some surprise at the robustness of the MDI market in the chart below, and it would be wrong not to admit that our cautionary antennas are rising. The auto exposed products should still see some upside from higher auto production in the second half of the year, but otherwise, a possible consumer pullback to take the wind out of the sector sales, especially if the US is constrained moving out products because of container and shipping issues. The significant cost advantage remains in the US but the ethylene market over the last week is a reminder of what can happen when you struggle to find someone who can take the last pound. Given infrastructure, energy, and clean energy investment, as well as reshoring, many materials could see significant offsets to consumer spending pullbacks and our focus would remain on PVC and building products, as most of the hit would be in consumer durables. Metals demand should remain strong regardless. For more see today's daily report.

A couple of weeks ago we raised the idea that US methanol could be a significant beneficiary of the conflict in Central Europe, not just because it is very economically unattractive to make methanol in Europe, but because it might be possible for Europe to import methanol for its energy value - $40 per MMBTU natural gas can make all sort of alternates look attractive. The impetus behind the methanol spot price increase in the US may be in part rising local natural gas – or the fear of further increases – but export demand is likely the larger driving factor and this could continue or even increase further if potential European importers work out how to convert to use methanol as a fuel.

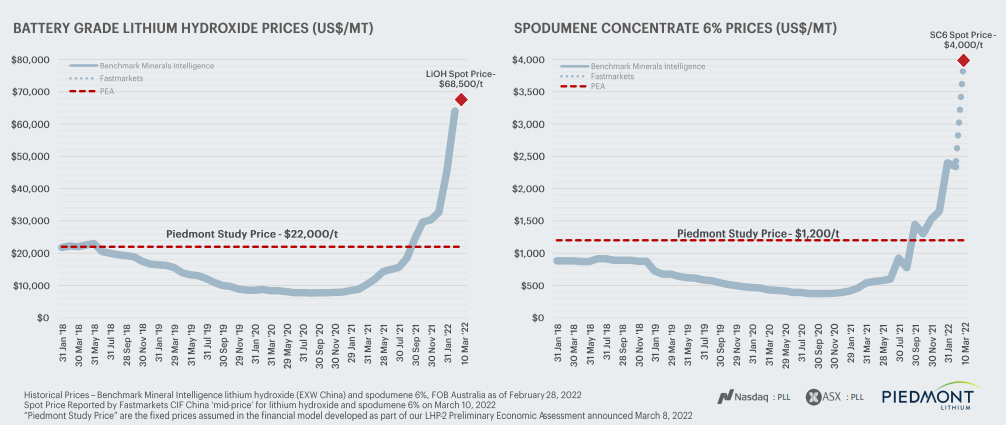

Could what we are seeing in metals happen in chemicals and polymers? Over the last few weeks, we have seen already high metals pricing spike even further, both because of production shortfalls and because of expectation of higher demand, especially in the renewables space, as conventional energy prices have spiked. We show a lithium example below, but note that after chaotic nickel trading last week and a halt to trading, the market has made some attempts to reopen this morning with renewed problems.

The very strong Wacker results and bullish outlook make sense for a company very exposed to the solar industry. The solar companies themselves may be struggling to make money, but their demand is very high and their thirst for raw materials equally high. In bp’s annual review of world energy, the company is forecasting a three-fold increase in the rate of annual renewable power investment and all of this will require more materials – setting up polysilicon suppliers like Wacker very well. The negative for Wacker, of course, is the high European footprint and the current increase in energy costs in Europe. Given the strong demand for polysilicon, Wacker should be able to raise prices – adding to the woes of the solar panel makers. See more in today's daily report.

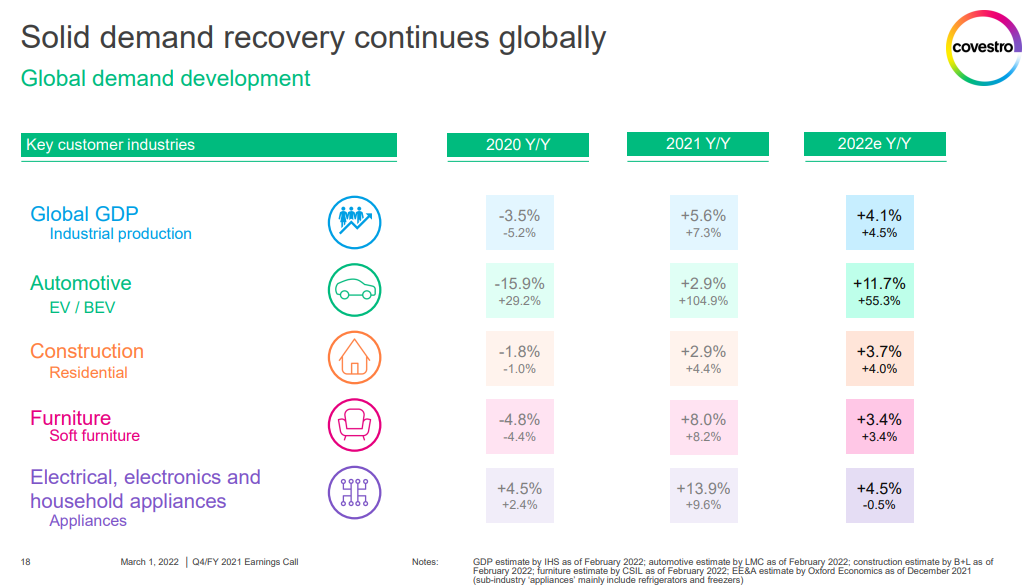

More confirmation from Covestro that global demand growth is strong, supporting reports that we have seen from most companies over the last few weeks. Some have struggled with raw material cost squeezes and either late attempts to raise prices or pricing lags in contract agreements, but almost all have pointed to very strong demand outside of auto OEM. We have questioned how much of this strong demand is inflation-driven, but it is very hard to tell as the last time we had significant inflation we did not have such an interwoven global supply chain as we have today, and consequently, it is harder to assess how much pre-buying may be going on, not because of fear of higher prices but because of fear of supply. Note that we have at least two European automakers (VW and Renault) shutting down facilities this week because they cannot key parts from Ukraine. This adds to the already problematic path for parts from China as well as the semiconductor shortage. If everyone is looking for a little bit more it would explain the very high 1Q 2022 demand that all are talking about and it likely means that inflationary pressures will continue as chemical and polymer makers try to make more, against a backdrop of higher raw materials and find it easier to increase their prices because their customers are as concerned about availability as they are prices.