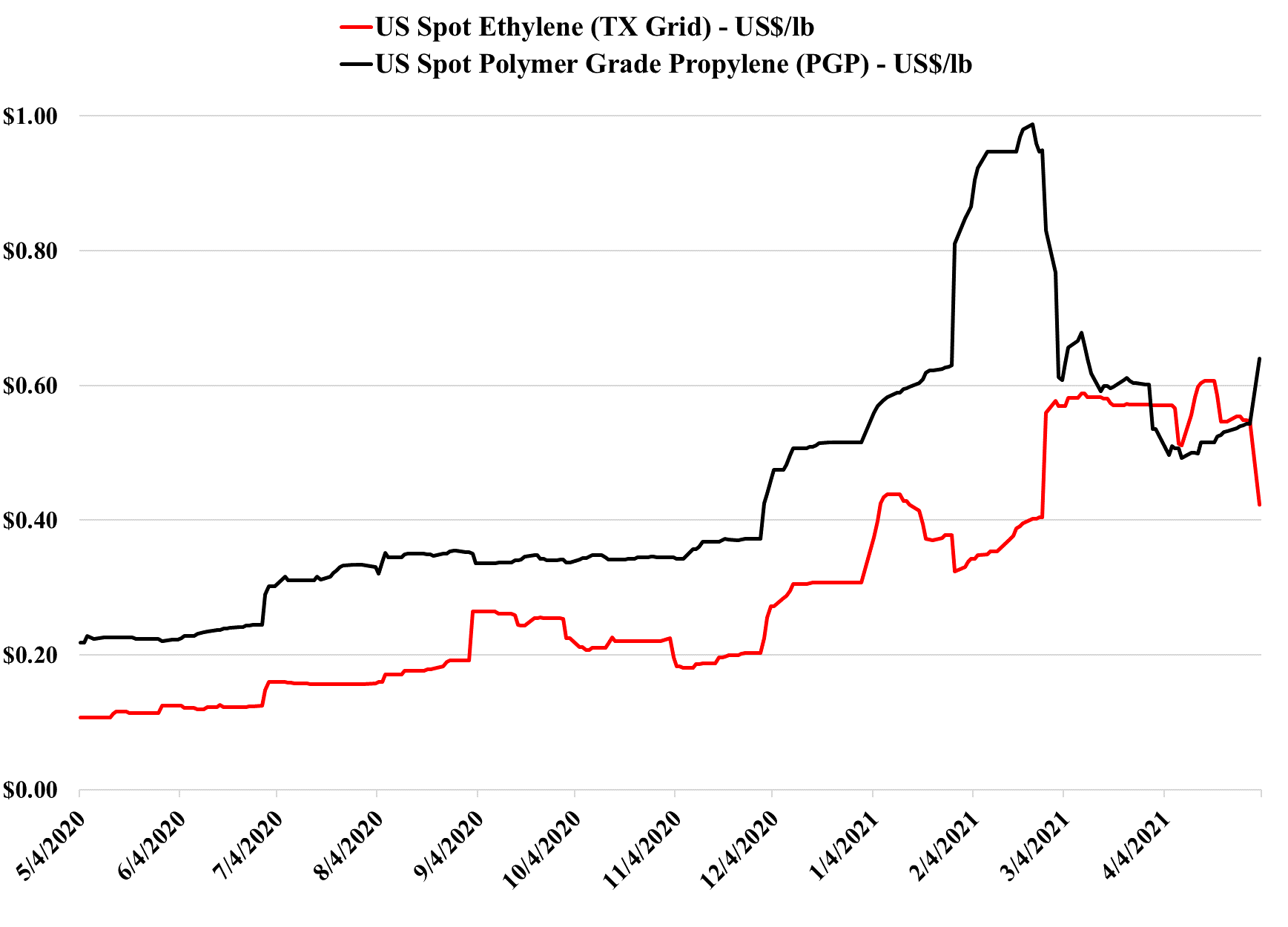

The movement down in ethylene in the exhibit below is significant, as it begins to show the overhang that the US has with ethylene supply. The price has to fall further before ethylene is likely to find any interested spot buyers outside the US (note that the US exported significant volumes of ethylene from November through January). The more important question is whether the weaker ethylene price starts to undermine derivative prices, especially polyethylene. We believe that will happen either late this quarter or early next, but only when US polymer buyers are satisfied that they have adequate inventory to meet what has been surprisingly strong demand. For more on this see our daily report.

We still believe that there is a good chance that 2Q 2021 is the peak for polymer profits in the US and Europe, but it very unclear how severe the downside could be, given the growth potential. Seasonal turnaround will keep markets more balanced in 2Q, and the major uncertainty beyond that will be weather in the US. A series of storms like last year could hold the market up through 3Q and into 4Q, but an absence of any weather events could expose US surpluses quite quickly, especially for ethylene and derivatives. The new builds in China have focused on ethylene and polyethylene (and some glycol), propylene and polypropylene, and PTA and PET, and this is where the potential weakness will emerge. There has been some new styrene capacity and that is also a vulnerable segment in our view. PVC, acetic acid, and large parts of the polyurethane chains look much more balanced to us and we have more faith in the projections being made by companies like Celanese, Olin, and Orbia than we do the major polyethylene producers. See today's daily report for more details.

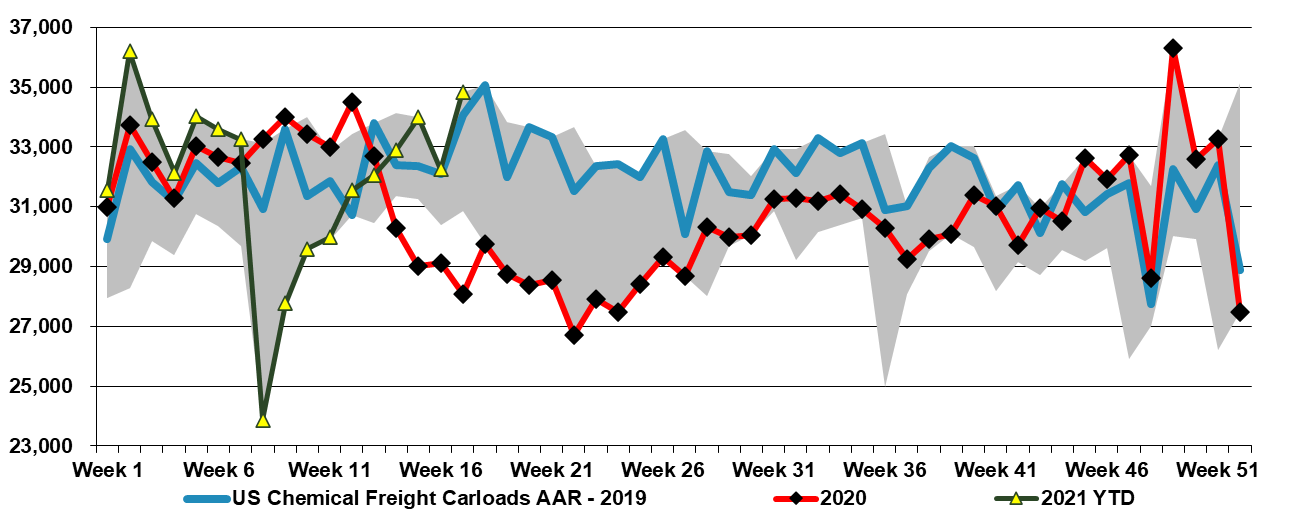

While we see some residual strength in several markets, and note the Dow push for higher MDI pricing, the European ethylene price move lower may be a more important red flag. Rail-car data below shows that logistics are getting back to normal in the US. The upward momentum in US polyolefins spot pricing is losing steam and prices in China are weaker. Read more in our

Thursday Daily Report

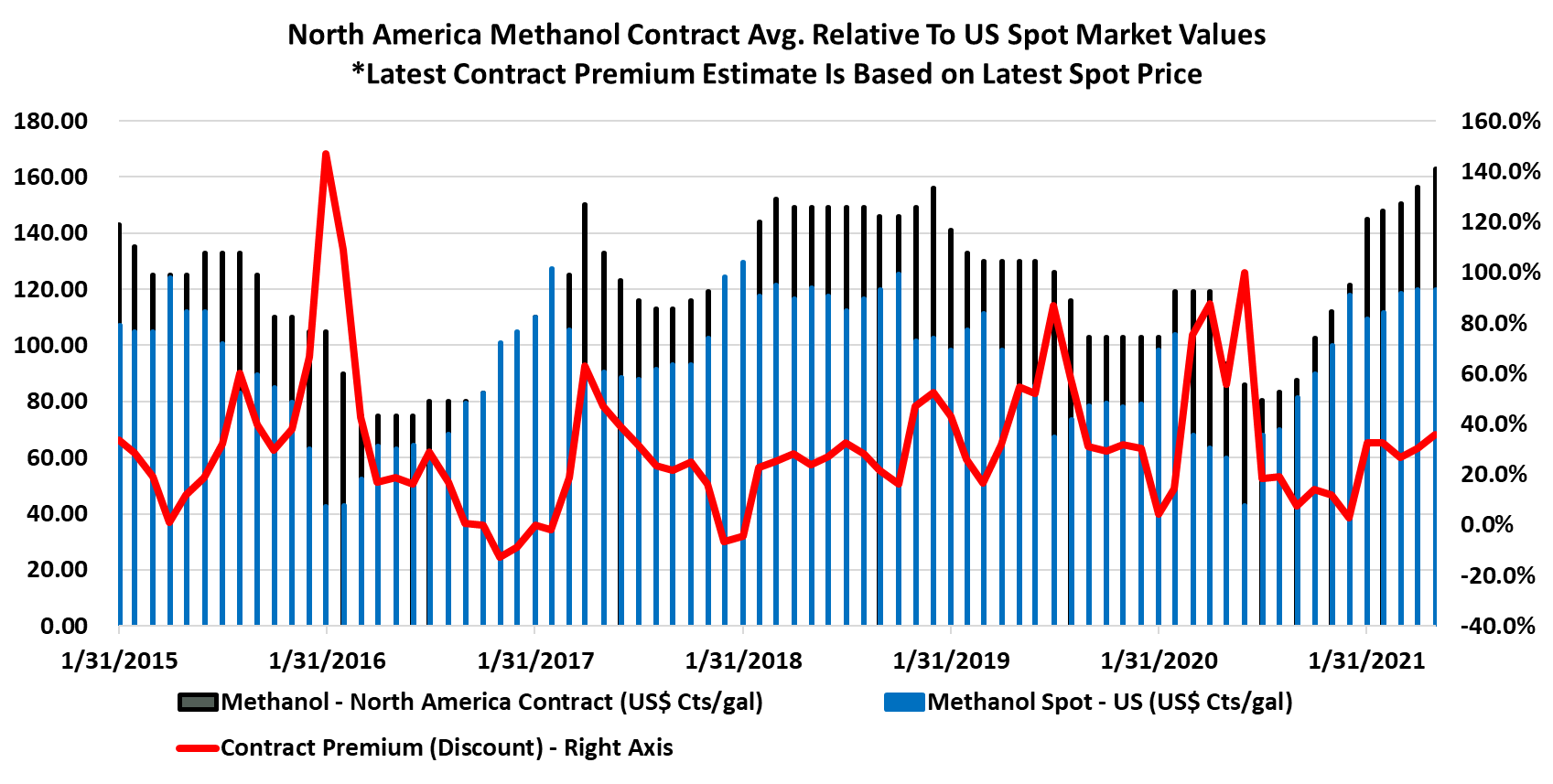

This latest data point in the exhibit below highlights the May contract nomination from Methanex relative to the current spot price and compares it to the history of both and the implied contract premium. Based on a historic look at the contract premium, the May producer push for price hikes does not appear aggressive. For more coverage on methanol and multiple other relevant and timely topics see our daily report.

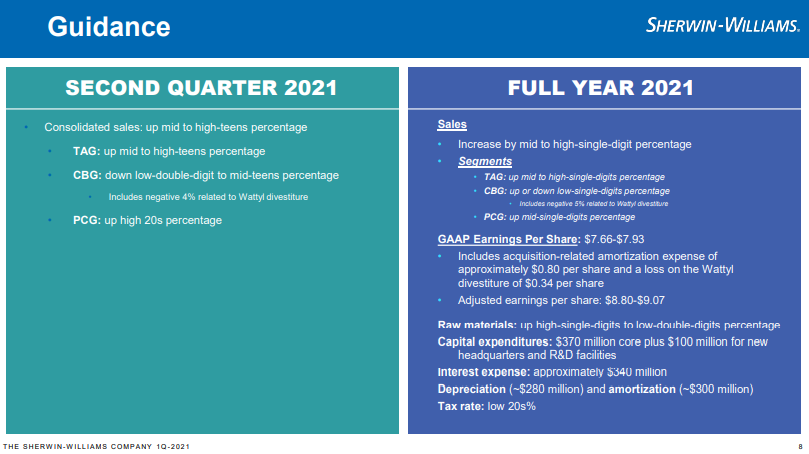

Mixed fortunes for the Paint Companies likely in 2Q 2021 and possibly for the rest of the year. Sherwin Williams is providing conservative guidance (see slide below) based on concerns over raw materials, and Axalta may be underestimating the auto production cuts -

read more in today's C-MACC Daily Report

Earnings beats and guidance raises are likely going to be the prevalent theme of 1Q 2021, and after Dow yesterday we have Air Liquide and Celanese today. Economic activity has picked up meaningfully in those segments of the economy that are suffering supply chain problems and while some of this is likely inflated, and will calm down once we sufficient inventory in the chain, it is worth remembering that large segments of the global economy remain depressed and that there are many growth drivers potentially still to come this year.

The highlight of the day is the very strong results from Dow and the even more positive outlook. While we see risks to the supportive supply/demand balances for some products in the second half of the year, especially the 4th quarter, there is no denying that all of the lights on the road ahead currently look green and we certainly would not criticize Dow for the outlook, even if it must rank as one of the most positive that we have seen (see table below), maybe the most credible positive outlook from any company in our careers (we have seen plenty over the years that have been complete nonsense). Dow is very well placed with its products portfolio to exploit both the current shortages and the expected post-COVID growth and it is important to note that the 1Q results were delivered in a quarter where there were still many COVID-driven demand constraints. We would stick by the advice that we gave earlier in the week, which is to keep the capital powder dry – and Dow seems to be doing this – reducing liabilities and not committing to share buyback beyond preventing dilution.

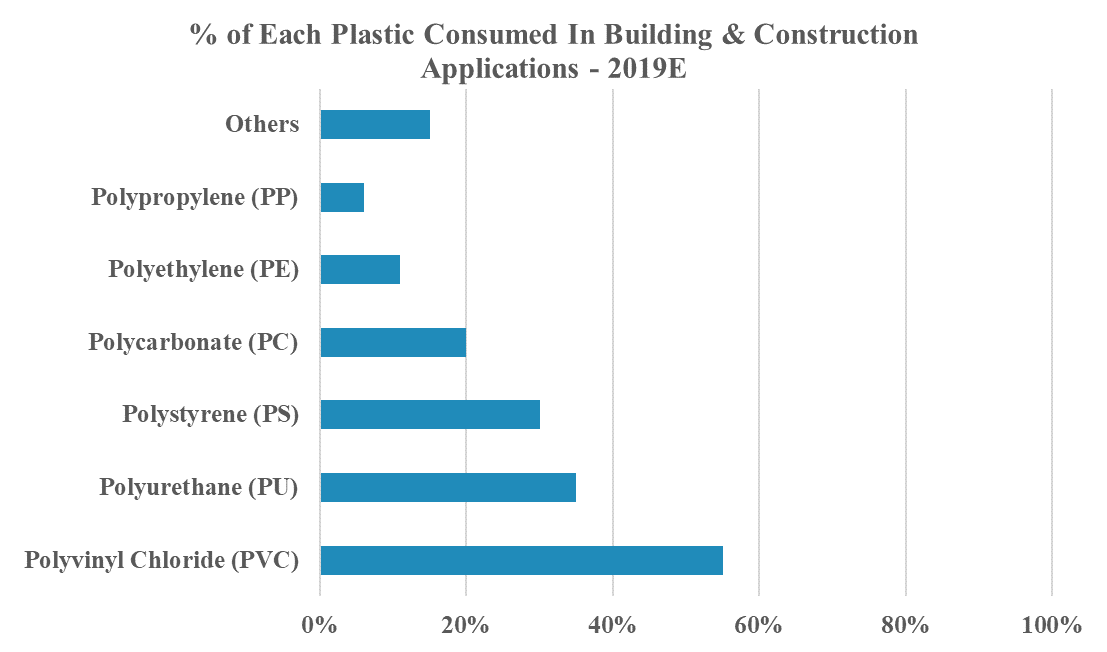

Building products demand remains very strong in the US, but the elevated lumber and PVC prices which appear impressively correlated right now are partly a function of supply chain issues. The housing market remains robust, but the winter storm in the South did damage to plants rather than structures – as opposed to Hurricane Harvey, which had a huge impact on building products. Because the housing market is strong, we are likely seeing speculators accelerate refurbishments to move properties faster, while demand lasts (anecdotally, the speculative renovation pace has picked up dramatically in Houston, where the housing market has bounced back quickly). But supply constraints likely are more of the driver – a random trip to Lowes yesterday found many of the shelves very light or empty in the building materials sections. As the chart below shows, building and construction is more than 50% of PVC demand.

The AkzoNobel comment today on completing its share buyback is a reminder that the chemical industry, in general, is reporting earnings that for the most part include record or near-record profits today and very strong momentum into 2Q 2021. They should all be prepared to answer the question of what they plan to do with the cash. The temptation is to build because prices are high and in some cases, customers are short of product and pleading for more supply. We often talk about the economics of NOW being used to justify spending far more than it should be – not just in Chemicals but also in other industries. In some areas, we are genuinely short of materials and semiconductors are a clear example of where underlying global demand has caught up with supply. Materials suppliers into this space are likely to see new capacity well utilized. For many of the other chemical segments, there is too much near-term noise to say with any certainty what is structural versus an immediate shortage. COVID, weather, a blocked canal, and unusual patterns of consumer spending have all played a part in inflating demand relative to supply, and we could be looking at a very different dynamic in 6 months.

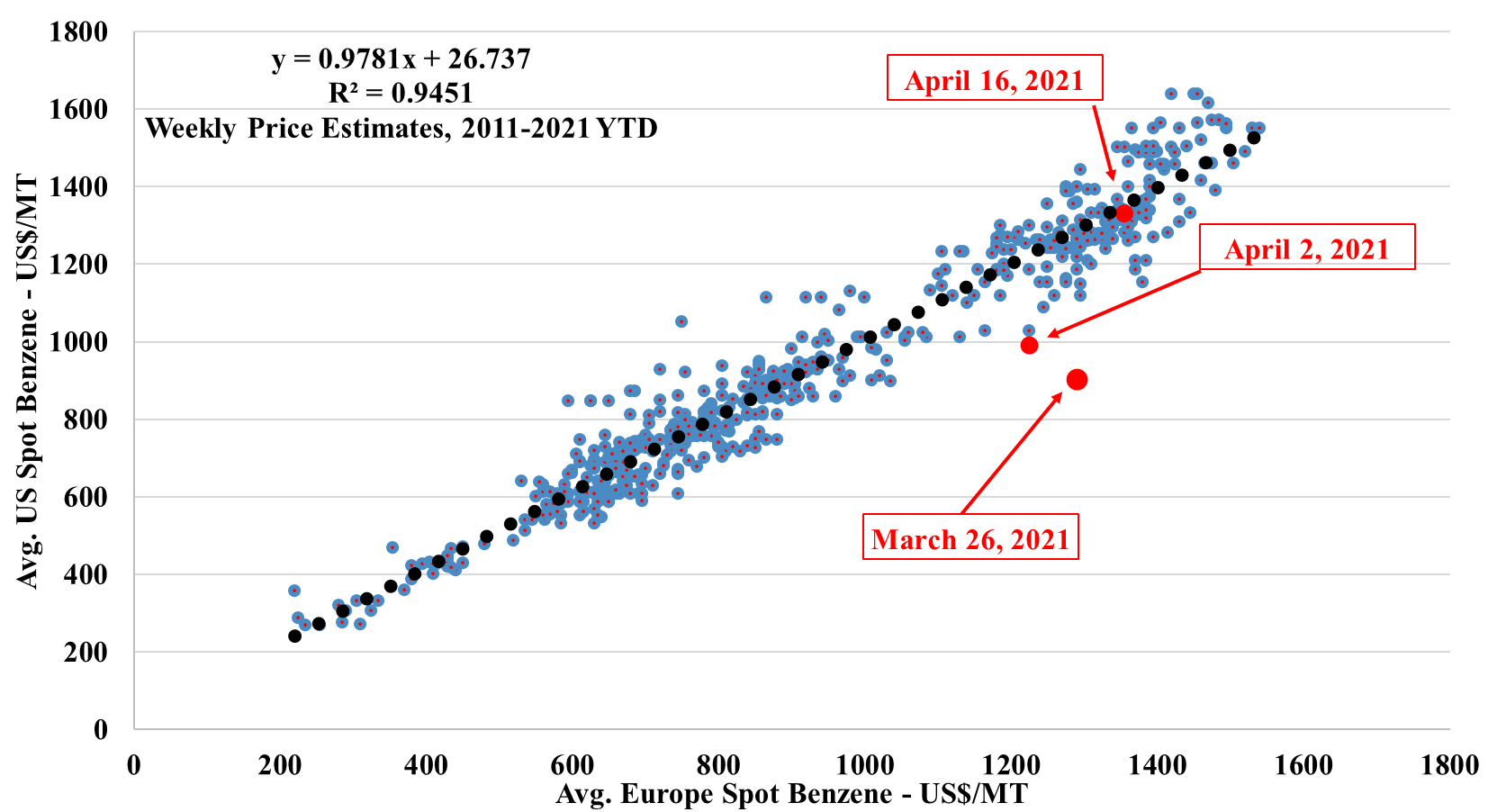

So, if you had been able to play the obvious arbitrage in the exhibit below when we published it first in March, you would have done quite well. You would have done better if you had just bought benzene on both continents, but you would have taken more risk. We like these scatter charts and we will use them more often when there are obvious regional arbitrages or just product arbitrages within a region. The overall benzene tightness has been caused by production outages in the US, shipping issues to Europe, and very strong demand for benzene derivatives. The start-up of the Shell POSM unit in the Netherlands has likely added to the imbalance as the facility is a major ethylbenzene consumer.