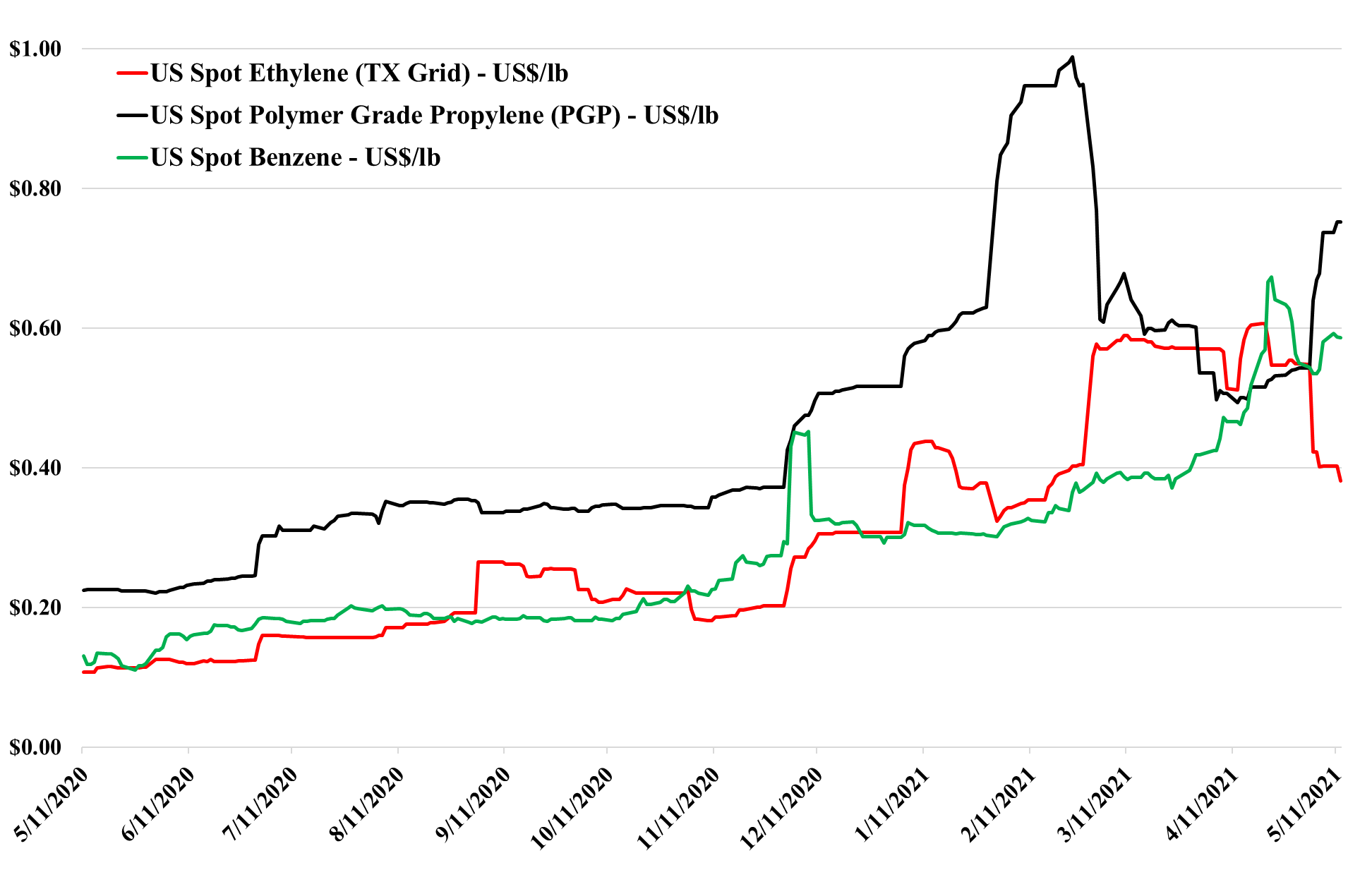

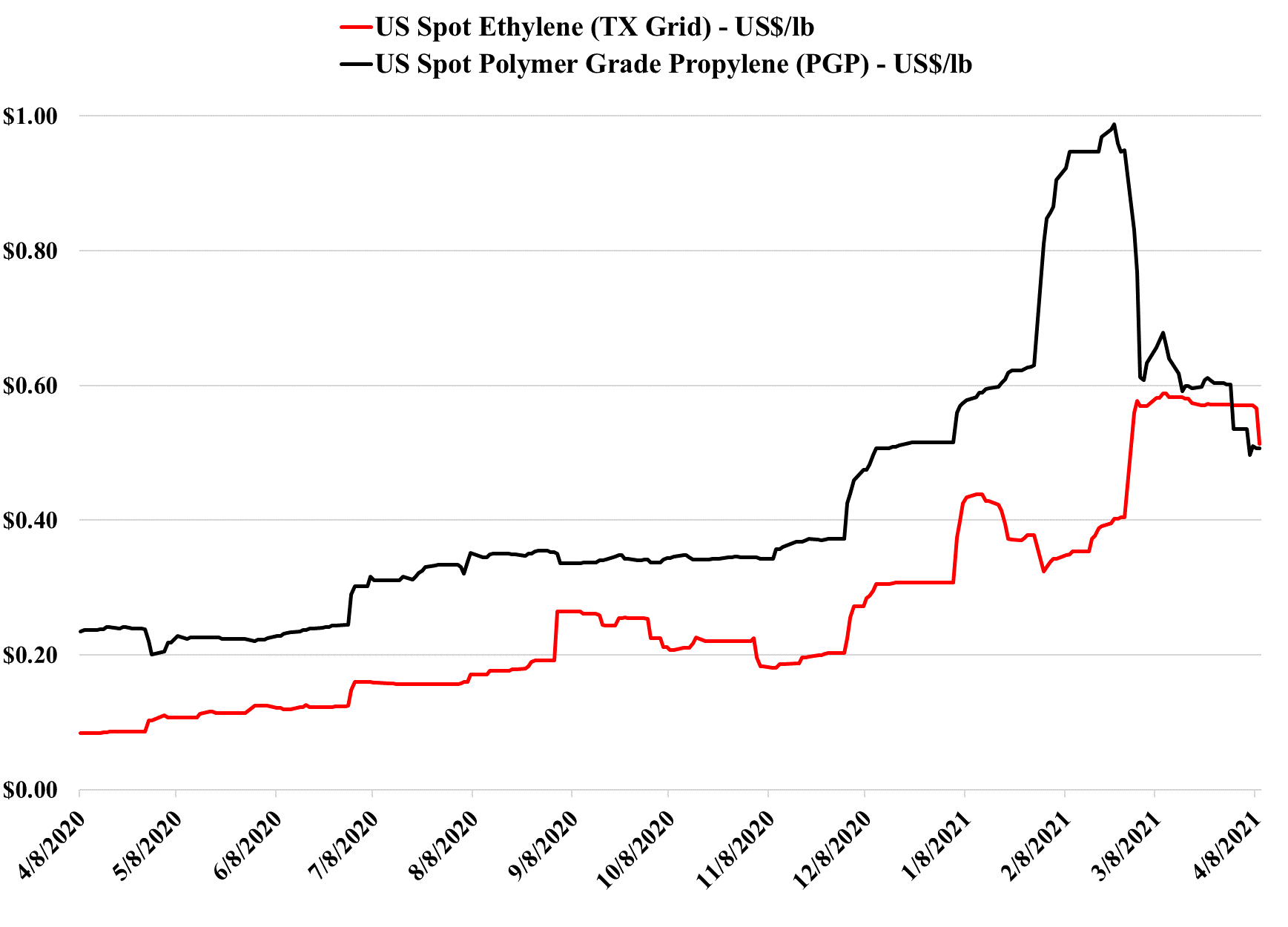

As we highlighted in yesterday's report, ethylene continues to weaken (see chart below) in the US and it is the one product with a true supply/demand-driven problem today – there is simply more capacity to produce ethylene in the US than there is the capacity to consume it. This is a recent phenomenon and has been clouded by the various storm-related outages, the delay in the Sasol start-up. We began to see the length in the ethylene market lats last year and physical export volumes jumped dramatically – fully loading the terminal in Houston for loadings from November through January. This was based on pricing from October through December that created a significant arbitrage to ship to Asia – partly because a few of the China integrated projects had ethylene derivative projects complete before ethylene units were complete. The risk for US ethylene is that it could go much lower – barring outages – as there is no one left in the US who can take a marginal ton, most likely, and China seems well supplied. For more details please see today's daily.

The relative moves in ethylene and propylene prices are not surprising given the news flow – propylene is likely being influenced by concerns around refinery cutbacks again – this time because of the colonial pipeline issues, while ethylene should continue to see downward pressure as the US oversupply emerges from all of the recent production difficulties. See our Daily Report for more.

The movement down in ethylene in the exhibit below is significant, as it begins to show the overhang that the US has with ethylene supply. The price has to fall further before ethylene is likely to find any interested spot buyers outside the US (note that the US exported significant volumes of ethylene from November through January). The more important question is whether the weaker ethylene price starts to undermine derivative prices, especially polyethylene. We believe that will happen either late this quarter or early next, but only when US polymer buyers are satisfied that they have adequate inventory to meet what has been surprisingly strong demand. For more on this see our daily report.

We still believe that there is a good chance that 2Q 2021 is the peak for polymer profits in the US and Europe, but it very unclear how severe the downside could be, given the growth potential. Seasonal turnaround will keep markets more balanced in 2Q, and the major uncertainty beyond that will be weather in the US. A series of storms like last year could hold the market up through 3Q and into 4Q, but an absence of any weather events could expose US surpluses quite quickly, especially for ethylene and derivatives. The new builds in China have focused on ethylene and polyethylene (and some glycol), propylene and polypropylene, and PTA and PET, and this is where the potential weakness will emerge. There has been some new styrene capacity and that is also a vulnerable segment in our view. PVC, acetic acid, and large parts of the polyurethane chains look much more balanced to us and we have more faith in the projections being made by companies like Celanese, Olin, and Orbia than we do the major polyethylene producers. See today's daily report for more details.

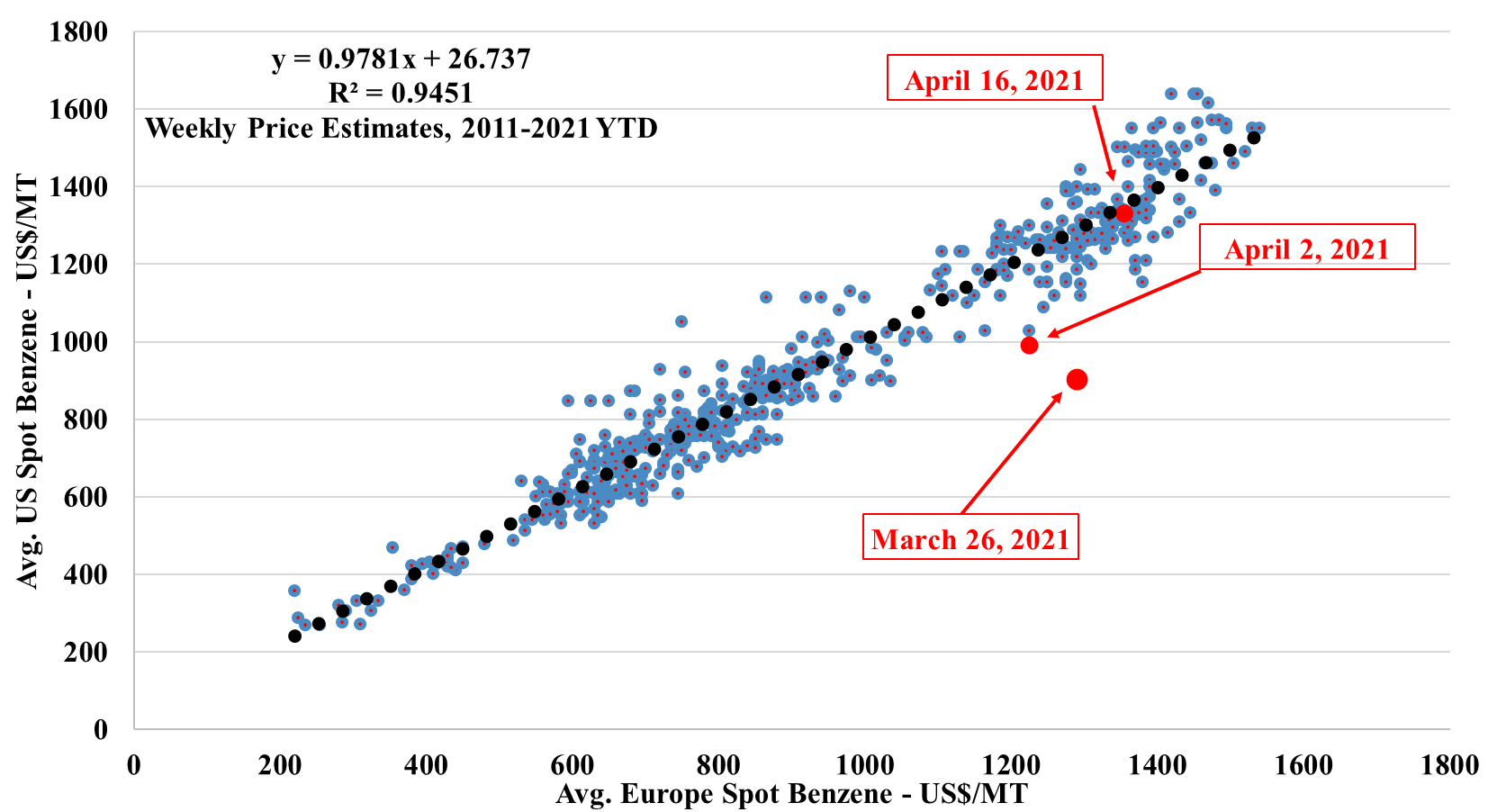

So, if you had been able to play the obvious arbitrage in the exhibit below when we published it first in March, you would have done quite well. You would have done better if you had just bought benzene on both continents, but you would have taken more risk. We like these scatter charts and we will use them more often when there are obvious regional arbitrages or just product arbitrages within a region. The overall benzene tightness has been caused by production outages in the US, shipping issues to Europe, and very strong demand for benzene derivatives. The start-up of the Shell POSM unit in the Netherlands has likely added to the imbalance as the facility is a major ethylbenzene consumer.

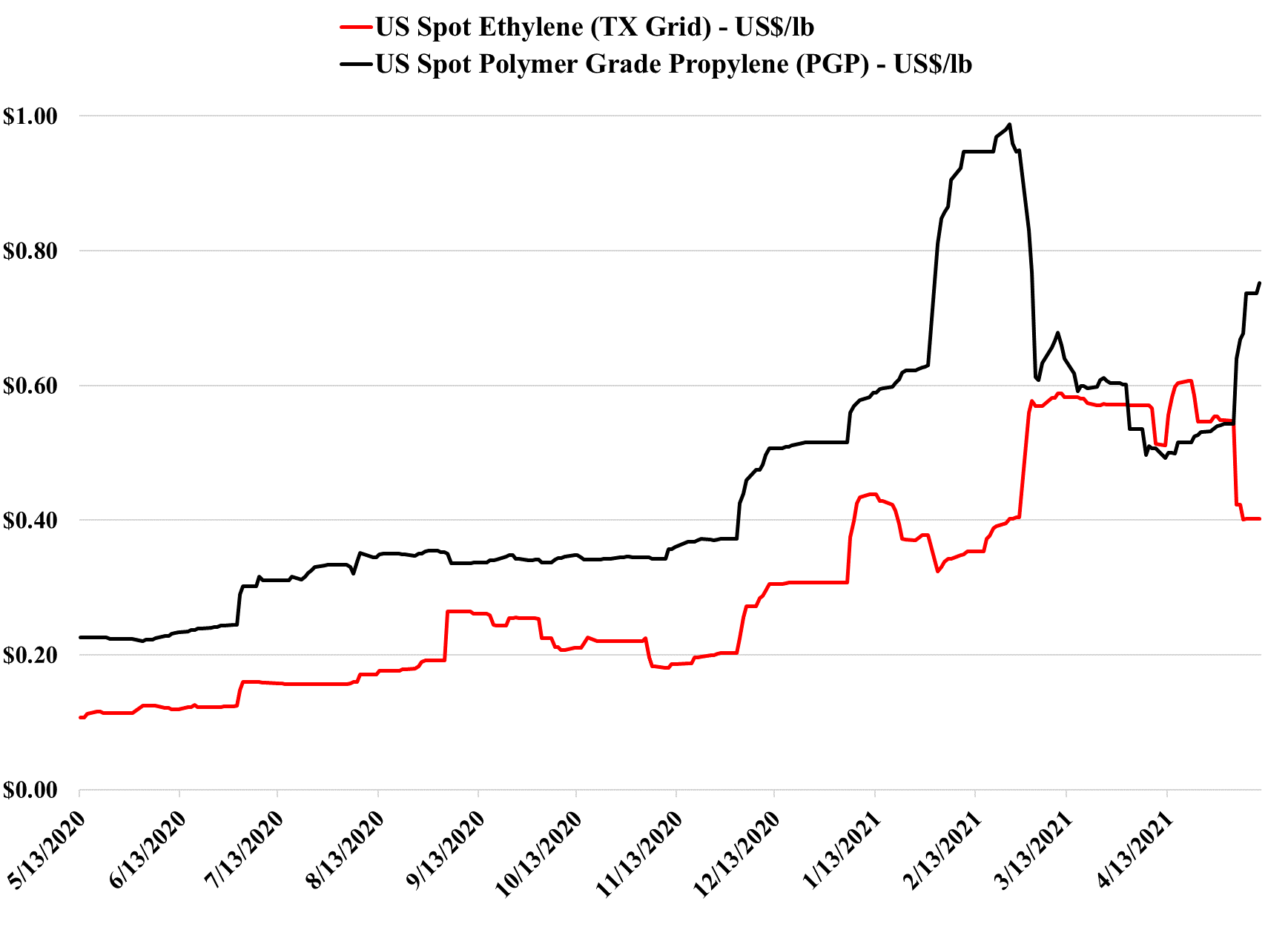

The price dynamic discussed in today's report and shown in the exhibit below looks unusual in a recent historic context and is unlikely to last very long, but it is worth noting that the recent history does not reflect the longer-term history.

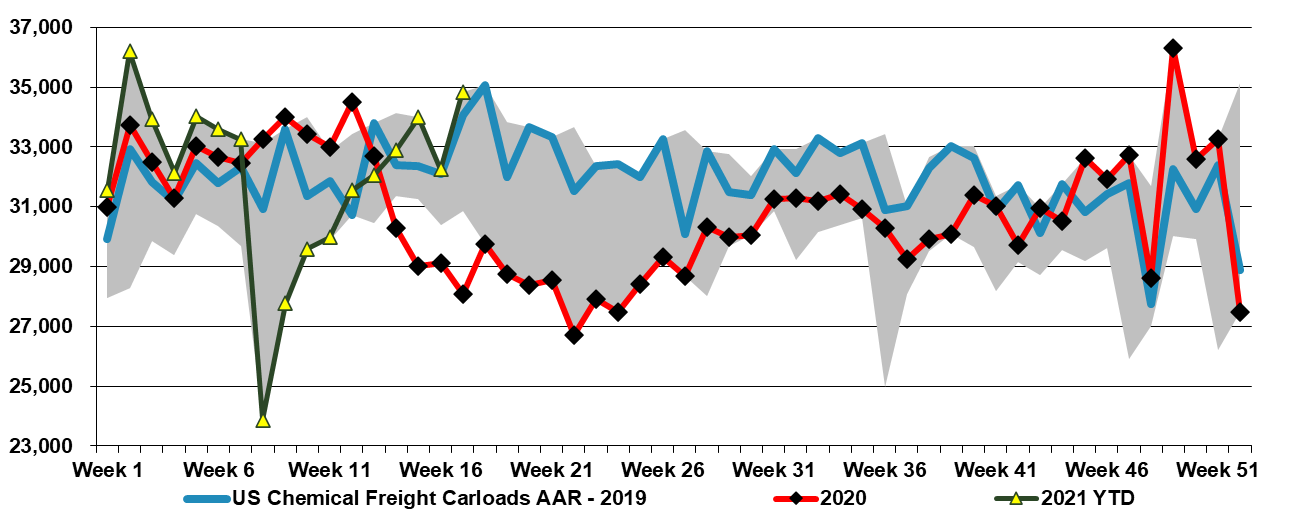

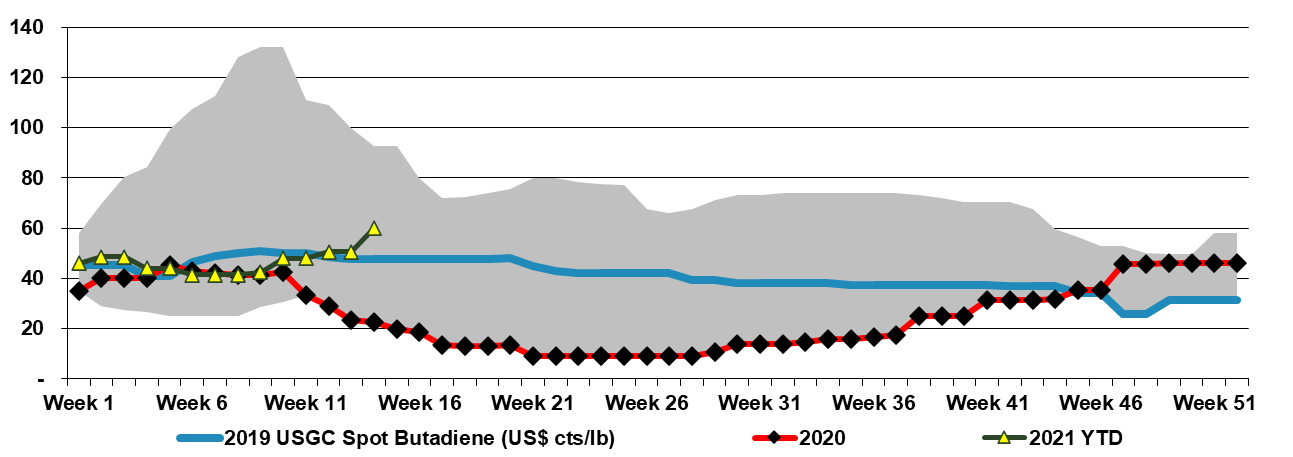

Last week we talked about the robustness of the US propane market and the China PDH headline is another example of offshore propane demand that we believe will keep US propane prices high, and probably high relative to ethane. This will mean that ethane stays favored as an ethylene feedstock but it will keep US PDH costs higher than they have been over the last 5 years. With propane and naphtha staying out of US ethylene plants we are seeing strength in butadiene, as domestic demand picks up and production remains constrained. Butadiene could see price support for some time as the ethylene economics are unlikely to change, especially if we see more Permian output in 2Q and into 2H 2021 as this will keep ethane supplies high.