The ExxonMobil board headline linked has come up a couple of times since the Engine No.1 victory at the board meeting. There is no doubt that capital spending plans will be reviewed with the changes at the top, and we expect more management changes, which could also drive spending priorities. Over the last couple of years, several more macro studies have been done talking about oil demand in a climate change-centric world and all have highlighted chemicals as one of the likely longer-term growth avenues for fossil fuels. We would expect ExxonMobil and other oil majors to look at investments in chemicals as a route to more captive consumption of hydrocarbons and believe that this could ultimately keep basic chemical and polymer markets oversupplied through the balance of this decade – we have been writing about this risk consistently since early 2020. ExxonMobil is already building ethylene capacity in the US in a JV with SABIC, but more oil company investments could come in the US. The caveat is that, as Dow covered in its MDI press release yesterday, any new investment is likely to need a carbon plan to get stakeholder and regulatory approval.

There is an interesting difference between the base chemicals markets and some of the other broad commodities and intermediates, and we have economic growth that is testing the capacity limits for many commodities and downstream products, but the overbuild in basic chemicals, most recently in China, is putting significant downward pressure on pricing, as we highlighted in yesterday’s Weekly Report. Capacity shortages in intermediates and some specialties, which are driving the investments we highlighted in today's daily report and which are a steady flow of news this year, are leading to some expanding margins over base chemicals in select areas where capacity has not kept pace with demand.

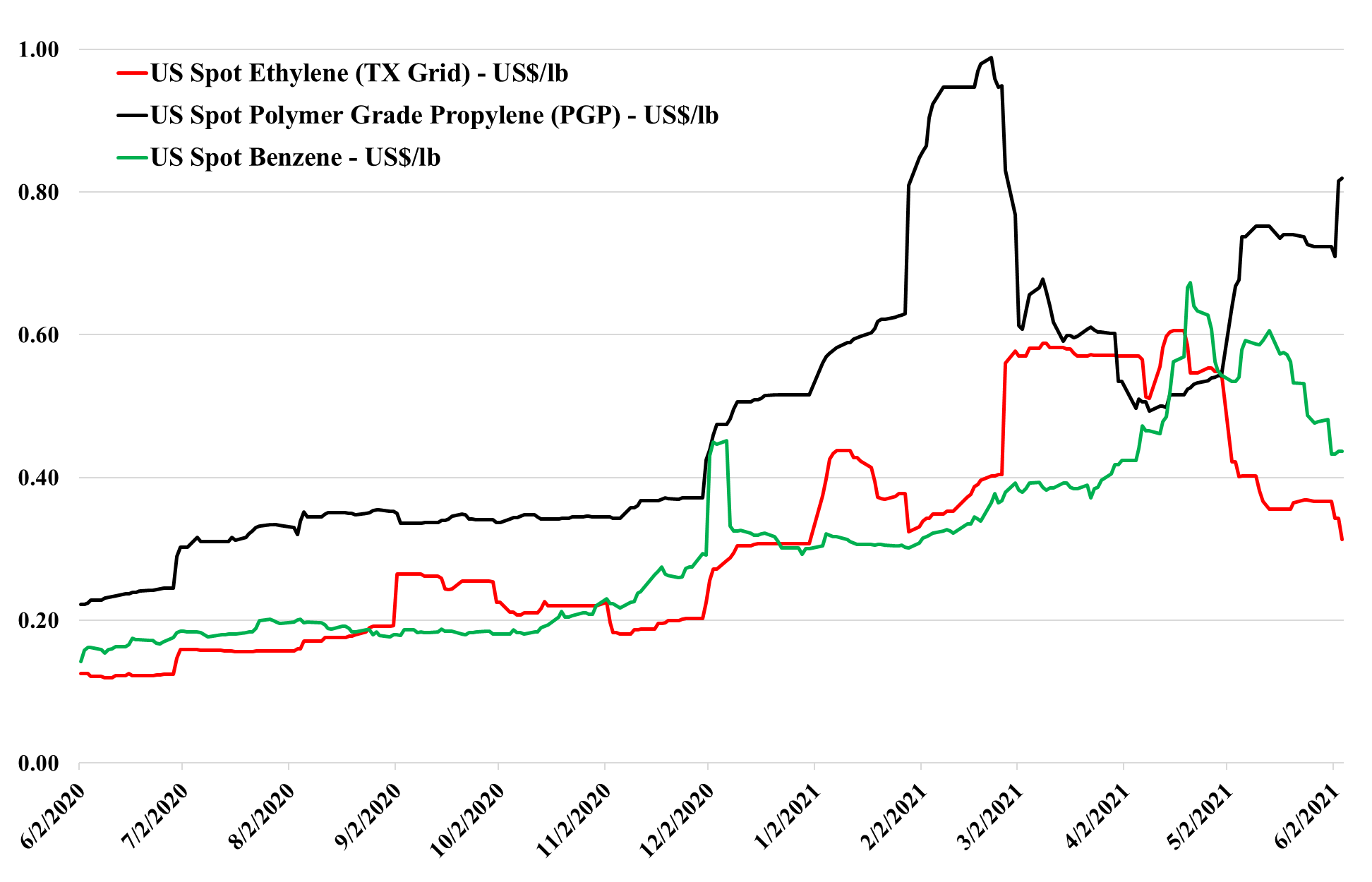

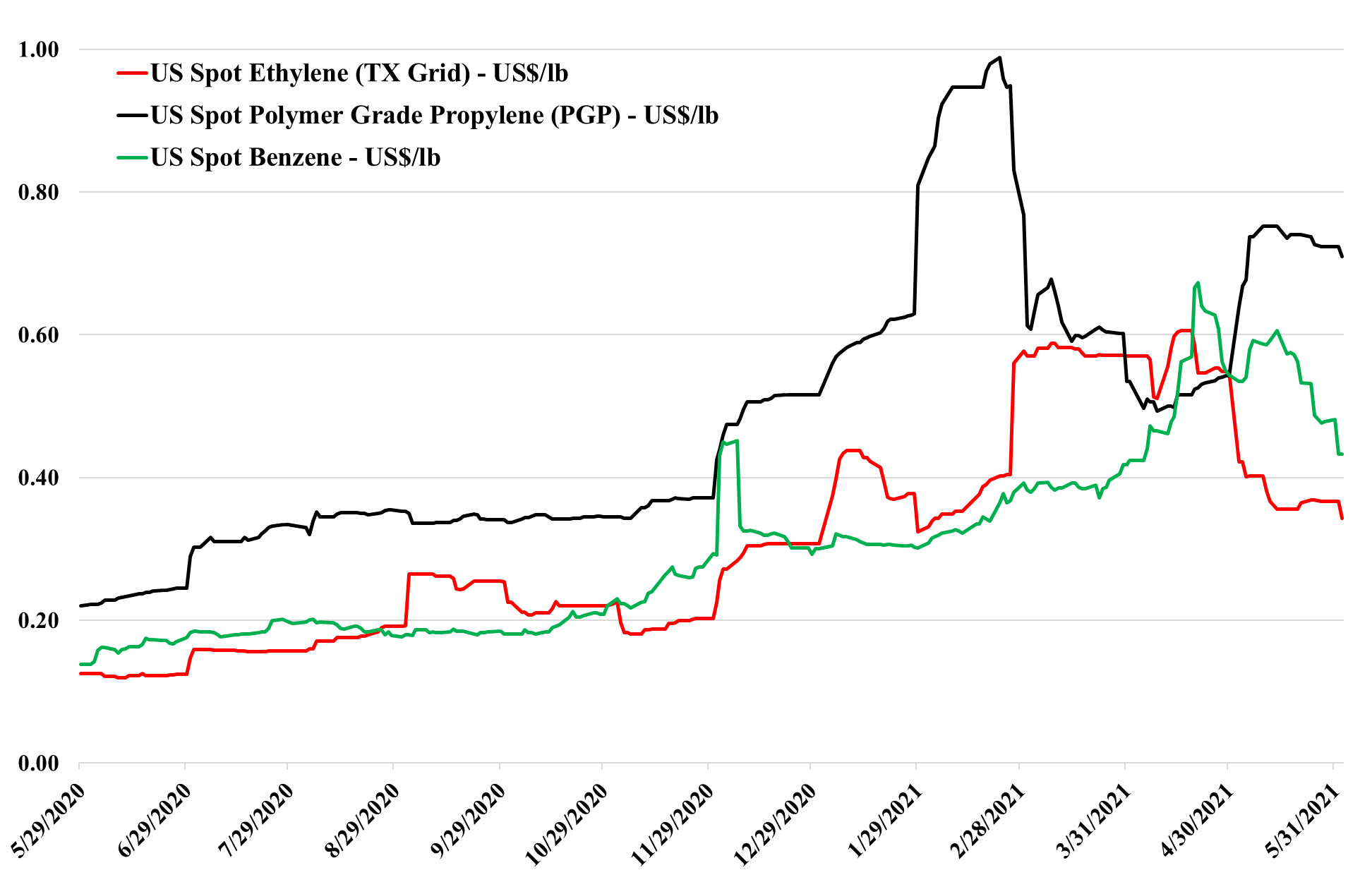

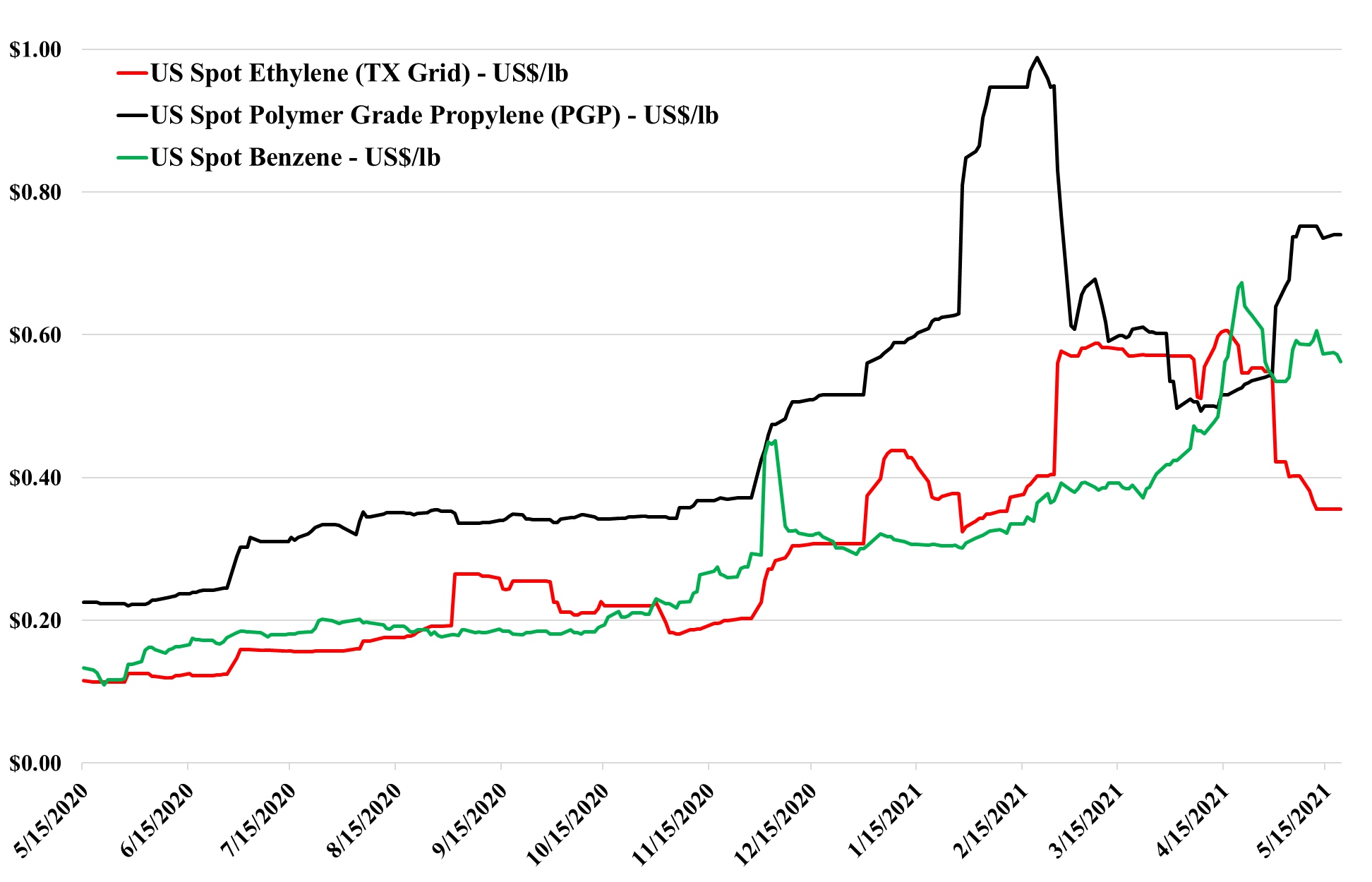

The oversupply in China for many commodities is becoming more evident daily. Our research depicts this as supply-driven, based on the surge of ethylene and propylene and derivative capacity since 3Q 2020. Notwithstanding the Dow commentary (in our daily report today), the weakness in Asia in polyethylene will ultimately impact the US, as the US relies on international demand for at least 25% of its polyethylene production – much less for polypropylene. The gyrations in the ethylene and propylene markets, as shown in the chart below, indicate the US dealing with the differences between the two monomer chains. Far more ethylene and ethylene derivatives move offshore than propylene and propylene derivatives. Despite the ongoing strength in derivatives, the ethylene market is loosening. At the same time, propylene shows extreme volatility because demand remains strong and has seen greater production issues on a relative basis, per our estimate. Supply is barely keeping up, even as refinery rates increase, because of problems with PDH units, pipelines, and splitters, which would not be meaningful in a more normalized market, but make a difference when refinery supply is constrained. High propane prices, which could move even higher, keep upward pressure because of PDH economics and because they keep propane out of ethylene units.

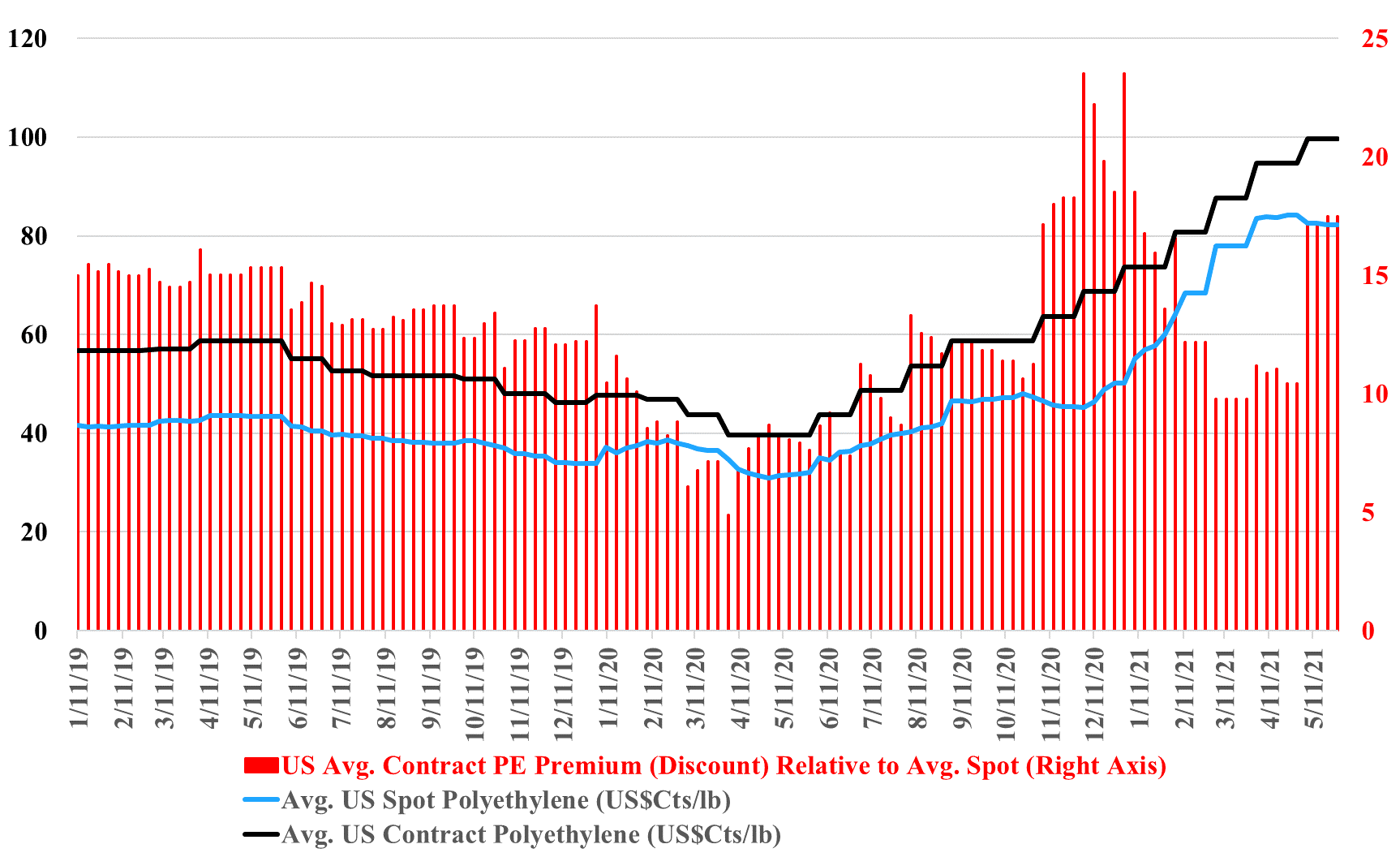

While we continue to see valiant efforts from the polyethylene producers to increase prices further in June, this is what we used to refer to as a “cow in front of a train” strategy. In that throwing a cow in front of a train was not going to stop it, but it might slow it down a bit! Barring weather, it is inevitable that US polyethylene prices shown in the chart below will start to give back some of their premium pricing over the coming months. One factor among several others pointed out on today's Daily Report is that Ethylene is much weaker and the international markets are materially out of line, and if freight rates have peaked, the arbitrage will undermine prices in the US. Producers will do their best to hang on to the high margins for as long as they can, and a few more cows may be sacrificed, but the weather is their only hope.

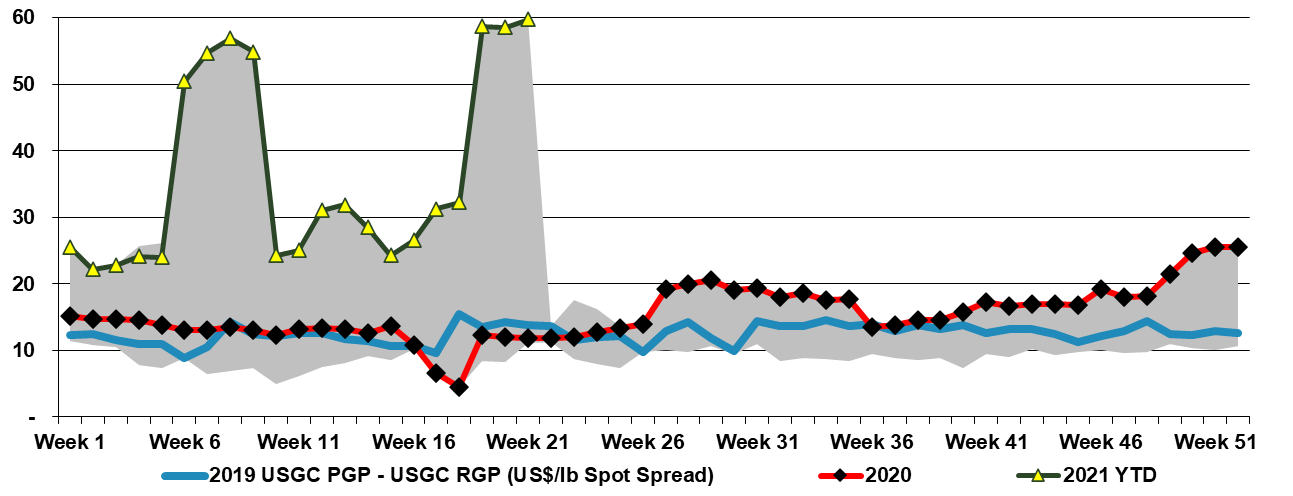

The easing of US base chemical spot pricing continues and has now spread, as expected to polymer grade propylene. Supply now appears to be back to levels that do not reflect weather-related interruptions and despite the very strong downstream demand in the US the inevitable monomer surpluses are appearing. The US is a net importer of benzene and consequently, we see a floor being reached pretty quickly here, and while propylene prices could drop much further, PDH economics will provide support, and with a higher propane price, that support will likely be much higher than the price support for ethylene.

The weakness in US monomer pricing has stalled this week, and buyers and sellers may be exploring marginal export or derivative export opportunities at these levels. Further weakness will come if attempts to export only serve to undermine pricing in the markets they are targeting. Underlying demand remains very strong and this is a supply-driven issue as US ethylene plants run back towards full rates and incremental refinery supply impacts the benzene and propylene markets. See today's report which includes detailed commentary on methanol in addition to the products in the chart.

The chart below and the others in our daily report linked add more weight to our argument that polymer grade propylene prices in the US have some downside and that it could happen relatively quickly, especially if ethylene producers play the current propane feedstock arbitrage to their full extent. Given weaker propylene derivative markets outside the US, propylene derivative pricing would likely come under some negative pressure if propylene prices fell.

Referring back to our daily report today, can polyethylene hold on? Despite the strength in US polyethylene prices and the aggressive attempts by sellers to hold on through the quarter, there are couple of key factors working against them. Local supply may be tight in the US, but as we discussed yesterday, ethylene is moving towards a global surplus that could push US prices even lower than we are seeing this week and as the chart below shows clearly, how large the gap between Asian ethylene prices and those in the US. Unlike ethylene, polyethylene is harder to trade in to the US, partly because it is an unusual movement and the shipping costs are high, as would be the cost of getting from a US port to a consumer, but partly because US consumers serving the higher end of the market are very grade and quality conscious and would concerned about product quality and the risk of sending something to their customers that does not do the job as well.

Pessimism in the Asia ethylene market is a bad sign for ethylene vs. other US monomers. Those in the US with ethylene surpluses may need to fight a bit harder to find homes for the excess product in the US. We have not focused on the cost curve for a while as markets have been tight and global costs have not been an influence in the market for some time. The US has plenty of dry powder, in that export prices can fall significantly before they approach ethane-based costs, and can fall below production costs outside the US – especially in Asia – and still generate a margin for the US sellers. But that would mean more downside for US spot pricing and it may be enough to create some surpluses and some downward pressure on US derivative pricing. The caveat, of course, is that we had the same setup last year, albeit with less new capacity in Asia, and the summer hurricane season quickly wiped away any US surplus. A better understanding of the current cost curve and relative regional pricing can be found in our Weekly from Monday.

This headline about China creating petrochemical deflation is largely based on the rate of capacity addition within China and that base chemical pricing in China still sits well above costs – but the argument may be flawed on a couple of levels. First, costs may not fall materially, given the increased thirst for imported naphtha and propane, as well as crude to fill new refining capacity. If crude prices fall, China will see lower costs, but then so will others. The margin issue is also in question because the wave of China’s new base chemical capacity is arriving amid a surge in demand growth, and this is why margins in Asia have not fallen closer to costs yet. China remains a meaningful importer of many base chemicals – less than two years ago for many products, but still meaningful, and it is the surpluses in the US and the Middle East that may drive deflation should supply chains stabilize and production rates remain high.