The BASF commentary about the impact of gas cuts in Europe should not be read as specific to BASF, but as we move out of the winter in Europe it is less likely that countries will directly restrict industry in favor of retail customers should gas supplies become limited. While many European countries will try to protect retail customers from hyperinflation in energy costs, their ability to do that for the industry might be more limited as they cannot find the additional gas, and subsidizing everything would be fiscally irresponsible. We expect to see more basic chemicals and derivatives moving from the US and the Middle East to Europe to displace uneconomic local production, but we understand that all shipping capacity is now constrained – liquids, gases, and containers – limiting the volumes that can move. The high end of the cost curve that Europe has occupied for decades in chemicals means that exports from Europe have been very limited and reducing exports is not a balancing act tool that Europe has to play with. We continue to see significant upward pressure on prices in Europe and the jump in inflation in the region, reported today, was dramatic but could accelerate as there are very few corrective levers that Europe can pull right now.

The very strong Wacker results and bullish outlook make sense for a company very exposed to the solar industry. The solar companies themselves may be struggling to make money, but their demand is very high and their thirst for raw materials equally high. In bp’s annual review of world energy, the company is forecasting a three-fold increase in the rate of annual renewable power investment and all of this will require more materials – setting up polysilicon suppliers like Wacker very well. The negative for Wacker, of course, is the high European footprint and the current increase in energy costs in Europe. Given the strong demand for polysilicon, Wacker should be able to raise prices – adding to the woes of the solar panel makers. See more in today's daily report.

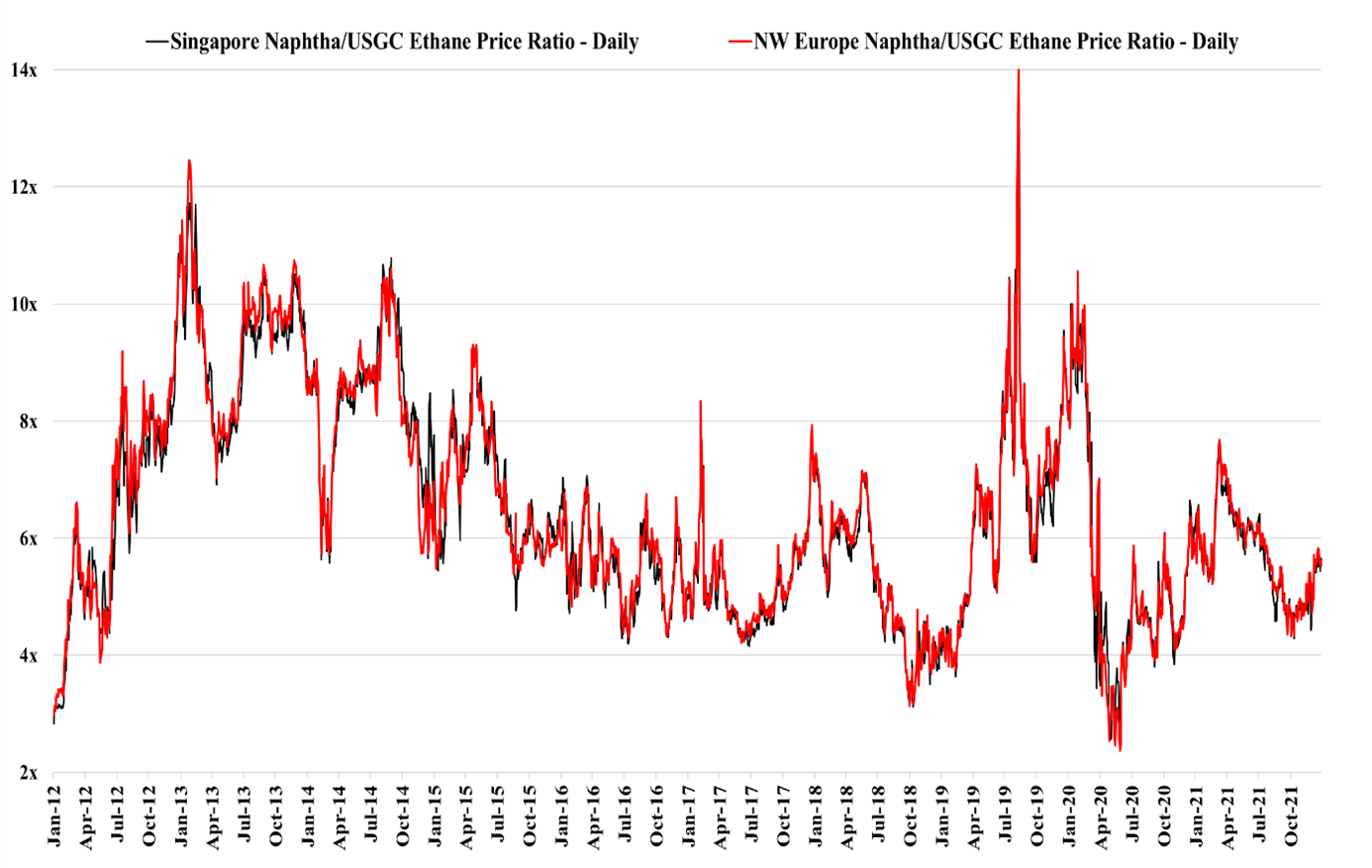

Looking at the exhibit below, it is clear that planning for consumers of hydrocarbon feedstocks is a challenge, and this is especially true for anyone looking at new projects, adding to our view that new project announcements will slow in basic chemicals, setting up for a major upcycle after 2023. The volatility in relative feedstock prices over the last ten years likely means that you would need to be able to demonstrate profitability under a wide range of possible feedstock price scenarios, while at the same time assuming that prices are set by marginal costs. Today global prices are set by marginal costs as parts of Asia are operating at break-even economics, with the much more profitable US and Europe impacted by feedstock advantages in the US and higher freight costs for polymers trying to enter the US and European markets. The US trade balance discussed in today's Daily is partly influenced by rising prices on some imported goods because of higher freight costs. While we continue to see some basic chemical expansion announcements, there have been periods of relative feedstock costs over the last 10 years where any project would have looked unprofitable. The volatility in the chart confirms that any producer will have better and worse times throughout a facility’s operating life, and consequently, start-up timing can be everything. Losing money for the first few years of any project’s life can destroy any ROI goals.

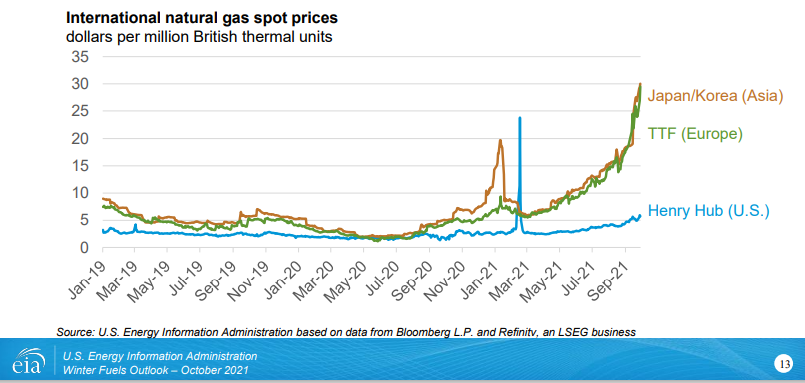

There are lots of discussions around the durability of higher energy prices and energy inflation is a central topic on some earnings conference calls and in many of our discussions with clients, especially those at chemical companies with the unfortunate task of having to prepare a 2022 budget, which of course includes a forecast of costs. We see continuing strain on the US and global natural gas system and, behind what will inevitably be some seasonal weather-related price volatility, a stronger market that could endure for years. The rate of addition of renewable power does not seem to be able to keep up with demand growth and replacement needs caused by some fossil fuel-based power plant closures around the World. Natural gas (LNG) is the natural plug-in replacement, and we continue to see underinvestment, relative to natural gas prices, as a consequence of ESG related pressure around capital spending. We would advise all clients to look at a 2022 scenario with natural gas, and oil higher than current levels.

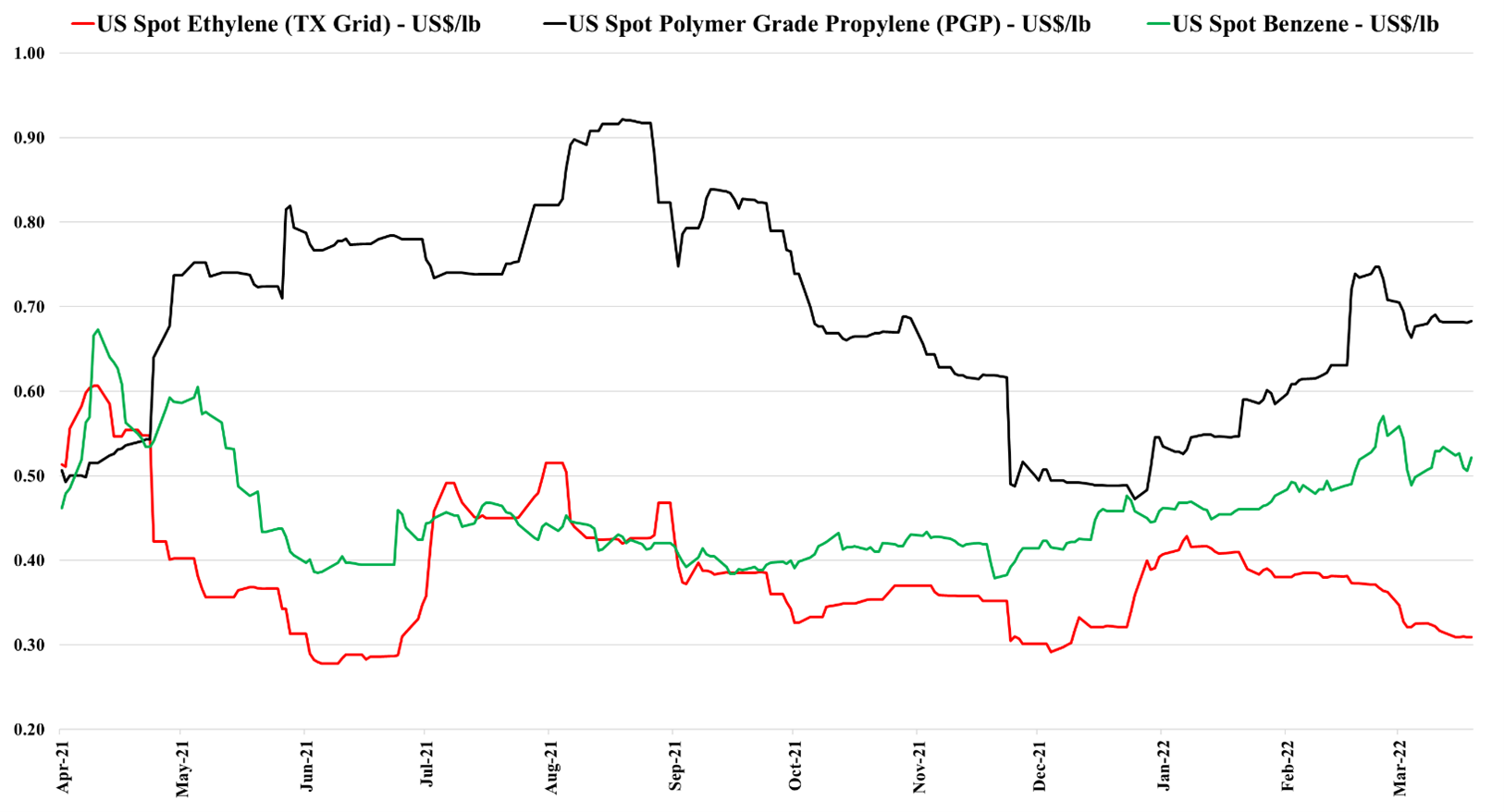

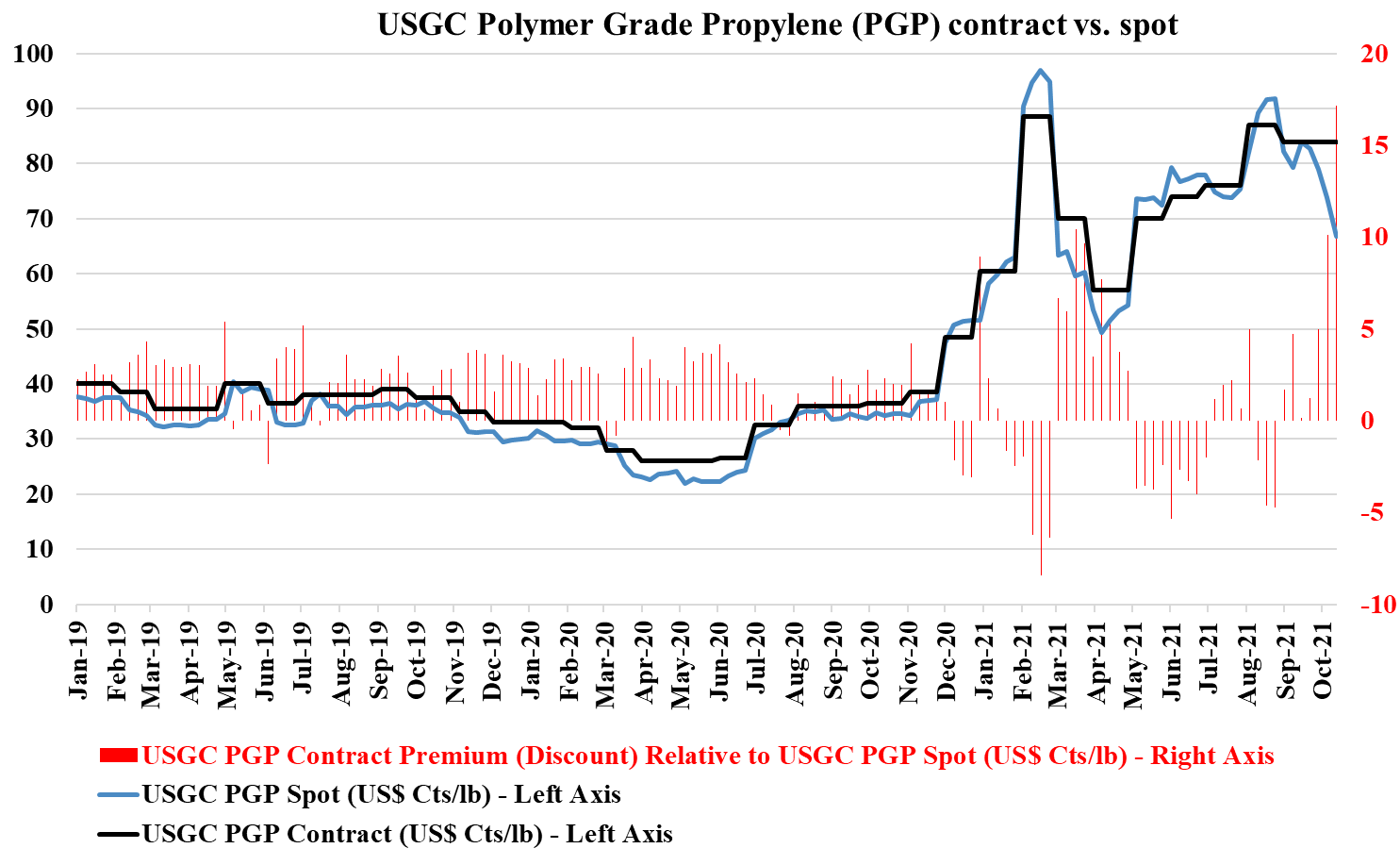

The propylene chart below shows a significant disconnect between spot and contract prices – more than at any point in recent history, and if the US contract price does not fall it will likely be an indicator that either discounts have increased or that more volume is moving against a spot price marker. The pressure is also on to lower ethylene contract prices, but the propylene spread is far more extreme.