What a difference a day makes – over the weekend we discussed how US ethylene pricing was approaching levels relative to Asia that could restart trade and today prices are jumping again in anticipation of possible lost production from the Tropical Storm. The risk from Nicholas is flooding, but it has already passed much of the South Texas capacity and the larger risk is to the capacity east of Houston and into Western Louisiana at this time. As with Ida, it will take several days to get a read on how much of the chemical and related capacity has been impacted and the likely impacts on supply/demand. See today's daily for more.

It will be interesting to see how US propane prices track this winter as we have low inventories in the US and there will likely be a step up in year-on-year export demand because of investments in Asia to consume imported propane. At some prices level, there will be demand destruction as ethylene and propylene economics are close to break-even in Asia and the region looks over-supplied enough for some producers to consider cutting back or even shutting down – if propane is the least attractive feedstock then the propane-based units will close first. Those producers in the US that have propane flexibility are unlikely to be anywhere near the market today as declining propylene prices in the US only make the feedstock less attractive. We wonder whether some of the traditional propane users in the US Gulf are experimenting with light naphtha/condensate as an alternative, but these feedstocks will also become less attractive as propylene prices fall. See more in today's daily report.

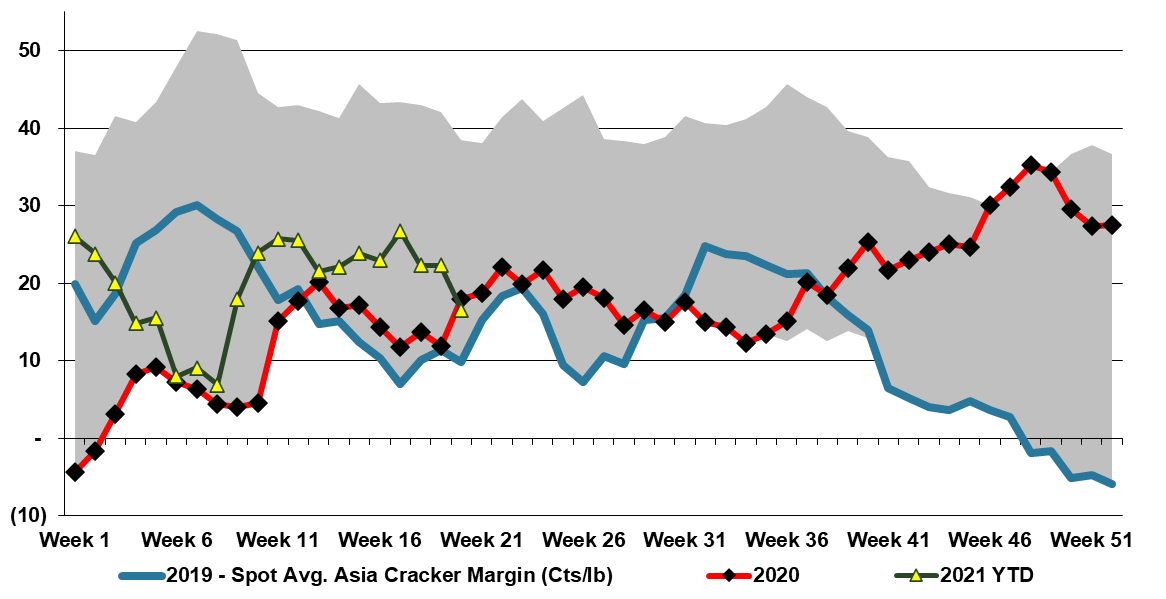

The ethylene price recovery in the US, discussed in today's daily report, is again a function of supply disruptions against a backdrop of robust demand. The net effect is to keep ethylene prices well above costs, at margins that justify investment and it is interesting to see the quick return of the CP Chemical project to the front burner. We could make a case that another ethylene facility in the US is likely a bridge too far at this point, despite the compelling current economics. The deep dependence on the export markets makes the US model very vulnerable to cyclical oversupply, and the current tight market is completely obscuring this risk and lulling producers into what we believe will be a misled sense of security. It is likely that the plants already built will prove to be good investments, not least because of the opportunity profits they are making in their early years of operations, but you would need to have a very bullish longer-term view of oil prices relative to natural gas to invest further, as even with an aggressive on-shoring manufacturing program in the US, the net export nature of the polyethylene businesses in the US is unlikely to change much. New capacity means more ethane demand, against a backdrop of lower E&P investment, and while Chevron has access to equity ethane from its US E&P operations, which may guarantee supply, it does not guarantee the price. Separately, while we believe that recycling targets in the US and the rest of the Wold will disappoint, they will still eat into virgin polymer demand. More chemical recycling will mean more “recycled” polyethylene available from heavy crackers – not ethane-based crackers.

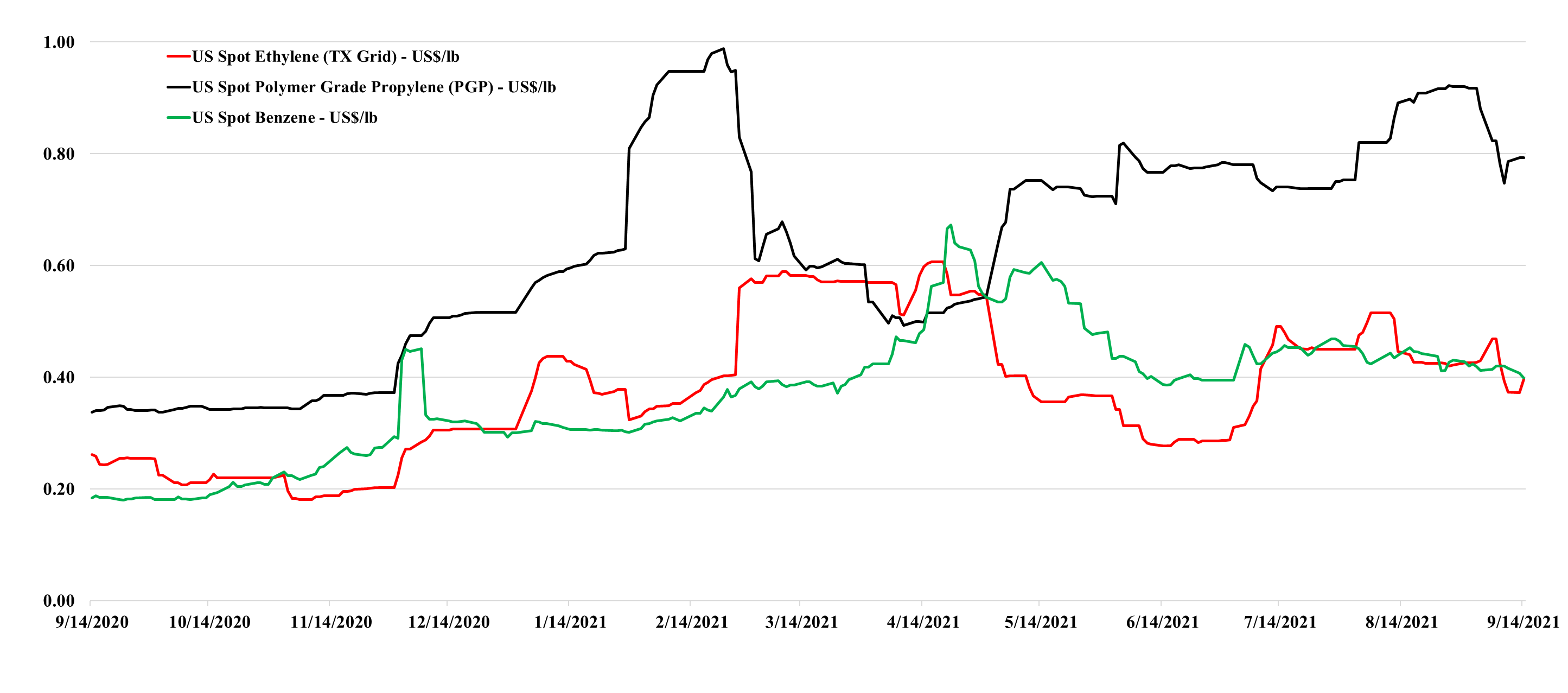

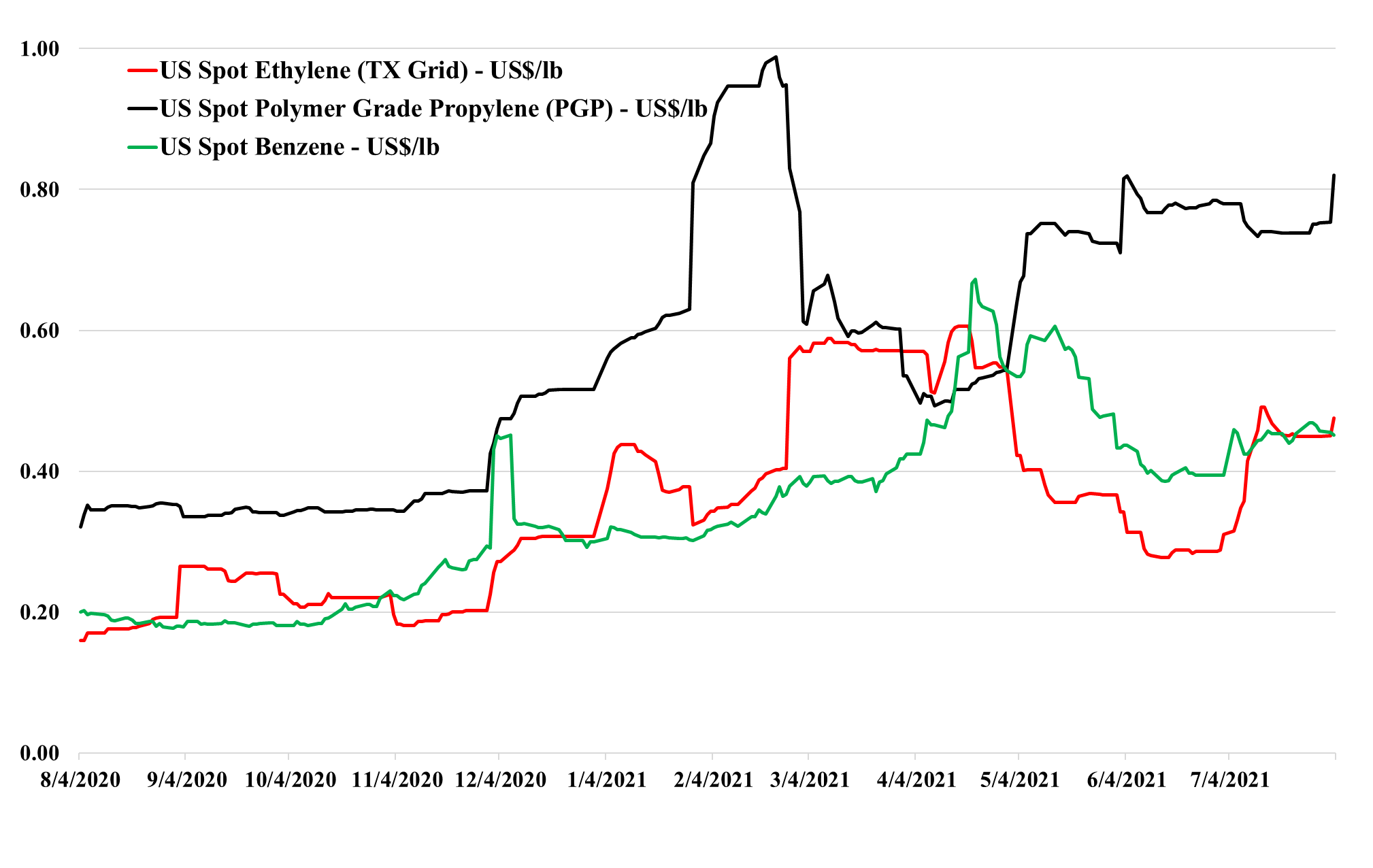

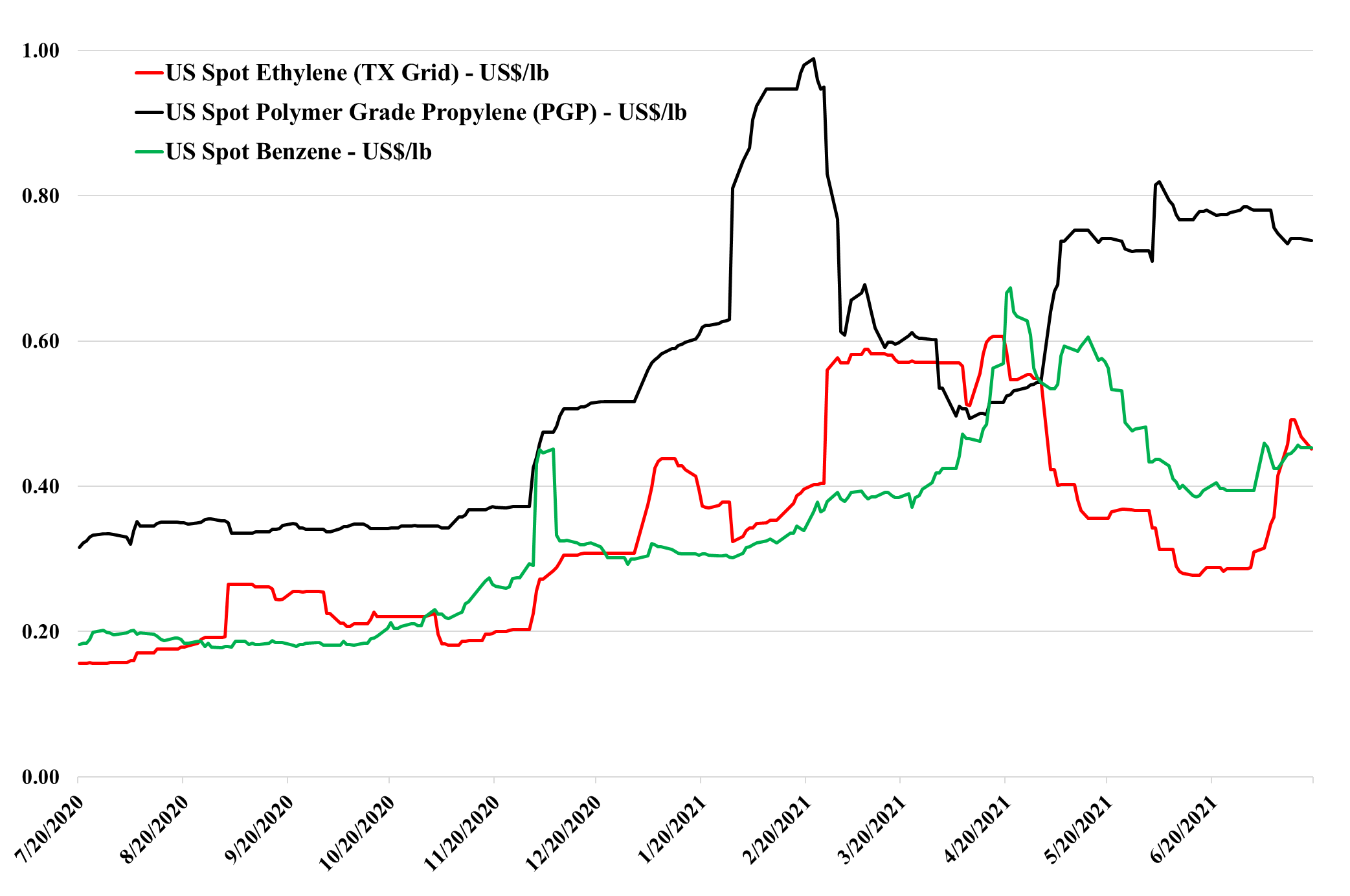

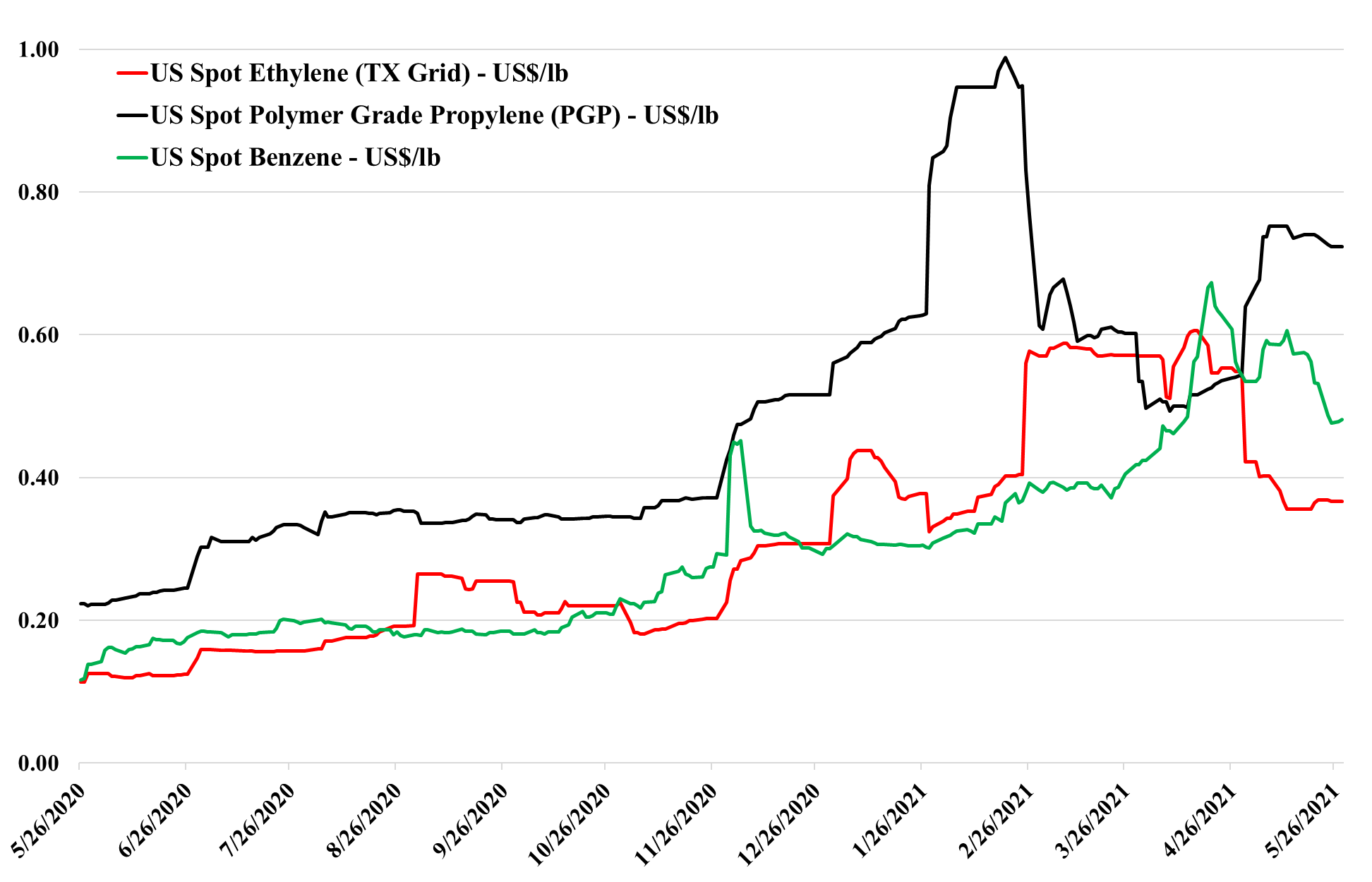

If this commodity cycle has the same drivers as prior cycles, producers like LyondellBasell and others will make comments like “stronger of longer” until prices turn, and if history is any guide, that turn will catch everyone by surprise, and even if it does not, there is no upside for any producer in predicting its end. As with all commodities, markets are tight until they are not, and markets are long until they are not. If you look at the ethylene and propylene price movements in the exhibit below you can see the speed of change that is possible and while the slope may be less severe for polymers in both directions, it can still be abrupt. The worst-case for the US industry would be a step down in demand coincident with the rising natural gas trend. There is no evidence of demand weakness today, but there will not be until it is happening. The extraordinary incremental freight rates shown in Exhibit 1 of today's daily report, make it increasingly unlikely that anyone sitting on surplus polyethylene or polypropylene in Asia can exploit the regional price difference. When demand and sentiment around supply chains turn, we would expect this spot shipping rate to collapse also – but there is no sign of that today.

We note the volatility in ethylene in the chart below and point out that ethylene sits in a precarious no-mans-land in the US with pricing neither reflecting costs nor incremental value in use. The downside to generating buying interest in Asia is significant – more than 25% - but an incremental buyer in the US could pay much more than the current price – in many cases to meet export obligations, let alone for domestic sales. We would expect the volatility to continue, with a downside from better production rates and upside from more constraints – demand fluctuations are likely immaterial relative to the impact that supply moves could have. See more in today's daily report.

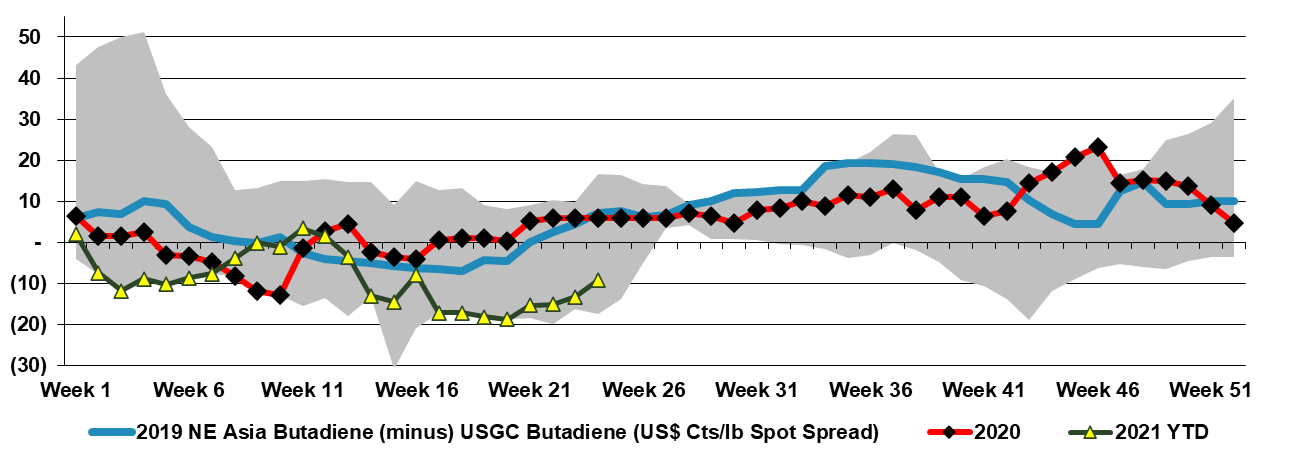

The exhibit below looks at the difference between a strong butadiene market in the US and a much weaker one in Asia. The strength in the US is a function of the stronger US economy and consumer spending as well as logistic issues with products containing butadiene derivatives, but also because there is no incentive to increase heavier cracker feedstock use right now in the US and consequently co-product butadiene supply remains constrained.

The weakness in US monomer pricing has stalled this week, and buyers and sellers may be exploring marginal export or derivative export opportunities at these levels. Further weakness will come if attempts to export only serve to undermine pricing in the markets they are targeting. Underlying demand remains very strong and this is a supply-driven issue as US ethylene plants run back towards full rates and incremental refinery supply impacts the benzene and propylene markets. See today's report which includes detailed commentary on methanol in addition to the products in the chart.

This headline about China creating petrochemical deflation is largely based on the rate of capacity addition within China and that base chemical pricing in China still sits well above costs – but the argument may be flawed on a couple of levels. First, costs may not fall materially, given the increased thirst for imported naphtha and propane, as well as crude to fill new refining capacity. If crude prices fall, China will see lower costs, but then so will others. The margin issue is also in question because the wave of China’s new base chemical capacity is arriving amid a surge in demand growth, and this is why margins in Asia have not fallen closer to costs yet. China remains a meaningful importer of many base chemicals – less than two years ago for many products, but still meaningful, and it is the surpluses in the US and the Middle East that may drive deflation should supply chains stabilize and production rates remain high.

How will global PVC values develop during the next three months? Lower or higher?

See our general PVC market views in our research report today titled, "

Do it to me one more time - China PVC spot prices hit another high; UK Carbon Trade To Start".

We welcome your thoughts regarding the development of PVC values.