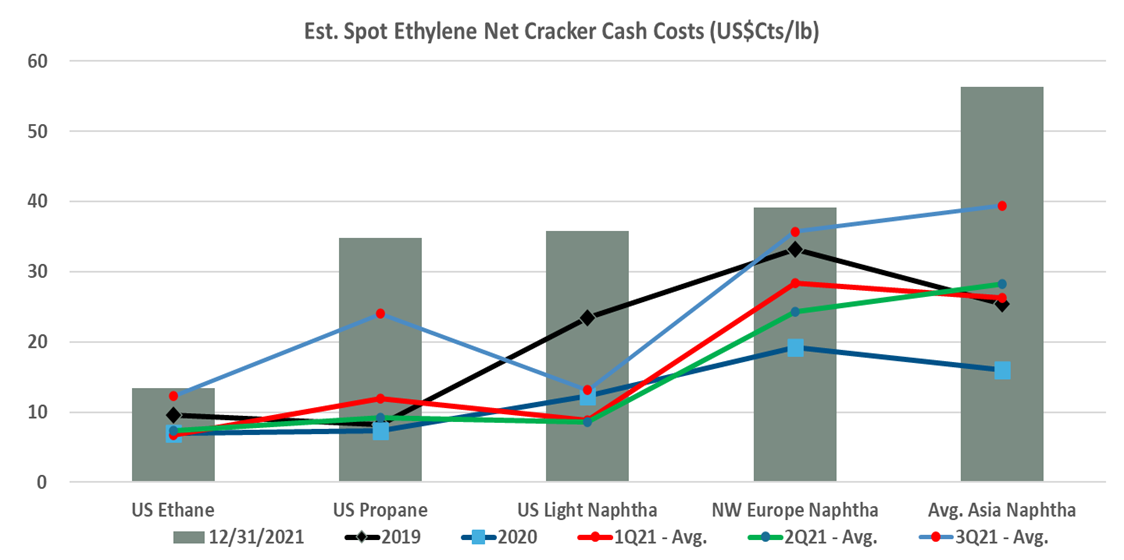

Given the higher prices of natural gas in the US, the shape of the current cost curve for ethylene in the exhibit below goes very much against traditional thinking and anyone looking at a historic crude oil to natural gas ratio as a proxy for the US competitive edge would be underestimating the advantage today. The major factor driving the change is the oversupply of ethylene co-products and their derivatives in Asia following a wave of new capacity in China and relatively lackluster growth locally during the Pandemic. As China and the region swung from net-short propylene and butadiene derivative markets to net-long, the price of derivatives declined and the price of the underlying monomers also fell – note that in our Daily Report today we show very positive margins for ethane based ethylene in the US and naphtha based margins in Europe, but negative margins in Asia and on top of that positive polyethylene margins in the US versus more break-even in Europe and negative in Asia. The exception in Asia is low-density polyethylene where there is extremely strong growth for solar panels, both for domestic markets and also for export.