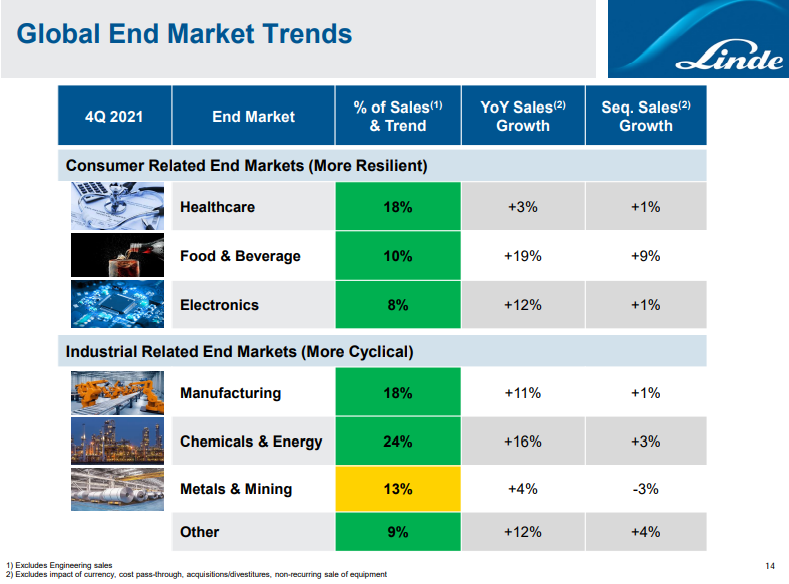

While the Linde results were very strong and surprised to the upside, we also want to focus on what messages they send about the broader economy. As recently as 10 years ago all of the industrial gas companies' results provided a reasonable barometer on the state of the industrial and other parts of the global economy. Industrial gases are an enabling raw material or process gas for so many industries that their direct use is generally a function of operating rates for the industry that they serve. Over the last 10 years, Air Products has deviated from the traditional model, with some very large investments targeting specific projects in Asia and the Middle East and their results are a less useful measure of overall economic activity. While both Air Liquide and Linde continue to reflect the broad economic backdrop well, both could be dragged into large projects around hydrogen over the coming years, and depending on how they choose to report earnings, we could lose the tangential “information” in their reported results. For now, the Linde results are very supportive of the broader industrial-economic strength that is being reflected in earnings and guidance across many industries, including chemicals and refining. The company has added comparisons with 2019 to show how much underlying growth has happened over the two years. While inflation and interest rate increases could slow things down, the Linde numbers confirm that we have a very positive demand backdrop today, and the company’s guidance would suggest that they think it can continue.

The Air Liquide announcement linked is consistent with the widely held view that semiconductor markets desperately need new capacity and shows that existing China-based manufacturers are stepping up. Air Liquide will supply new capacity in Wuhan, where it has been an active producer of high purity gases for the semiconductor industry for decades. While this is likely a sound investment for Air Liquide, backed by strong “take or pay” agreements from customers, the risk to the expansion is that while the world is in dire need of new semiconductor capacity, it is unclear how much of that need is for more China-based production. There is significant semiconductor demand in China and that demand will continue to grow, but consumers in the West are not only looking for more semiconductor supply but also more semiconductor supply security, and with the concentration of production in China and Taiwan, supply from outside the region is more desirable. We see new semiconductor capacity announced for the US and the auto industry, in particular, is calling for more diversity of supply, not just for semi’s but also for other EV components, especially batteries. There is already anecdotal evidence of a preference for non-China-based materials – all the way back to lithium - but how much more US and European producers are willing to pay for this “preference” will dictate the ultimate level of spending. Despite these concerns and absent broader geopolitical risk, this is likely a relatively safe project for Air Liquide and the capital commitment is not going to break the bank.