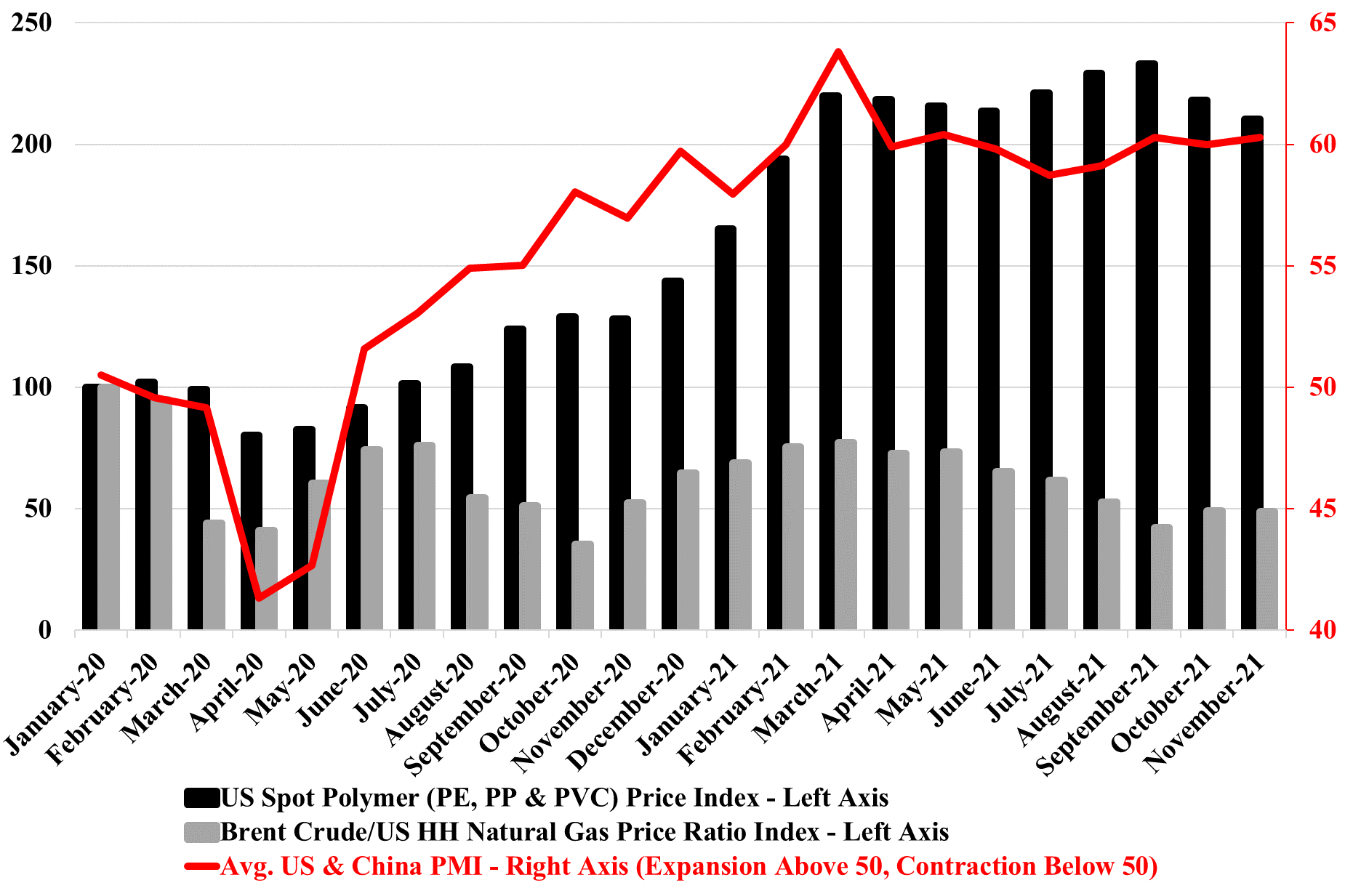

We have been asked a couple of times in the last week how US polymer (polyethylene in particular) pricing can remain so robust in a market where there is an inventory build going on. The PMI numbers are part of the answer. While we may be in the seasonally weaker part of the year, customers are still looking for more material than a year ago, and this makes the “we need a lower price” argument much harder, especially when the memory of 1H 2021 acute shortages is still fresh in the memory and when, more than likely, they are getting signals from their customers of a further step up in demand in 2022. We have done some traveling recently and the incremental demand for packaging polymers is very evident in the travel and leisure business, even if the number of travelers is still down. There is more packaging on airline and airport food and hotels are offering pre-packaged food for breakfast that would previously have not been individually packed. The reasons are obvious – safety and hygiene from the consumers' end and costs from the providers' end, as prepackaged food, can be bought in bulk and more cost-effectively and they likely have a longer shelf life.

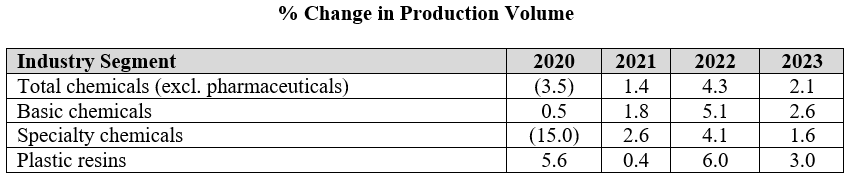

The ACC forecasts below leave us a little confused as the implication for specialty chemicals is that production declines in the US by an average of 2.0% per annum from 2019 to 2023. Given the demand that we are seeing for US manufacturing, as covered in our most recent Sunday Report, we would expect demand for all inputs to rise and it is unlikely that the gap would be filled by a swing in net imports. The lower demand from the Auto industry in 2020 and 2021 and broader manufacturing shutdowns in 2020 explains the 2020 and 2021 numbers to a degree, but it is not clear why there would not be a rebound as auto rates increase. We would also expect to see a stronger rebound in polymer production in 2022, assuming weather events are less impactful than in 2021, given substantial new capacity for polyethylene from ExxonMobil/SABIC, BayStar, and Shell.