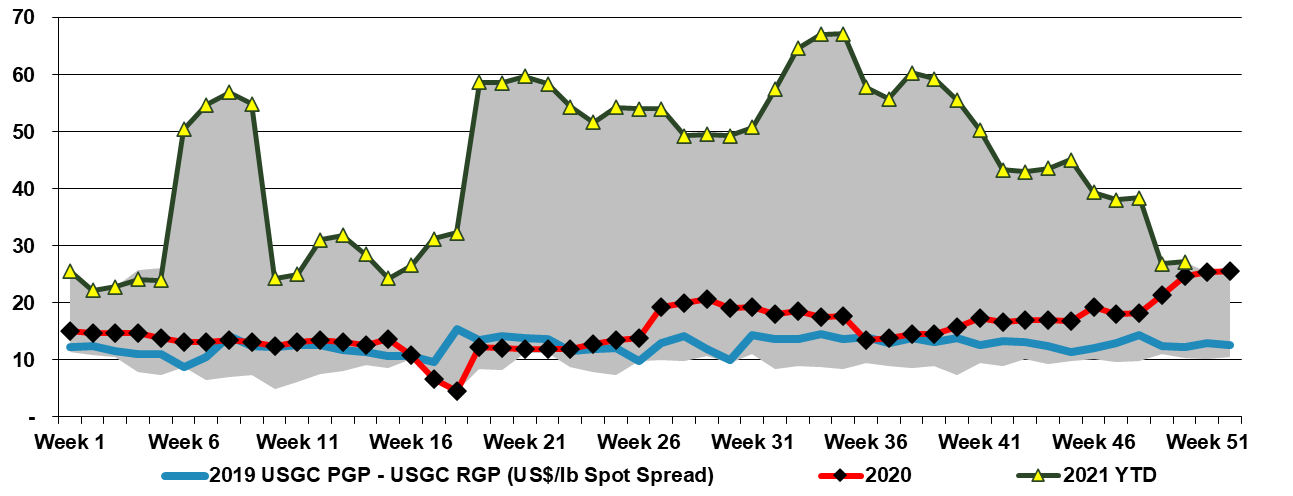

The CP Chem propylene splitter announcement linked suggests that CP Chem expects surplus refinery propylene to be around for the long-term, and likely has supply lined up from the parent companies. However, this is still a bit of a gamble unless both parents see a scenario where they would change catalysts on FCC units longer-term and run at higher severity for more propylene and more hydrogen. This project looked a lot better only a few weeks ago than it does today – based on the spread in the Exhibit below, but propylene demand continues to grow faster than ethylene demand in the US and with all incremental ethylene capacity based on ethane, propylene consumers either have to choose the path from refineries or invest in on purpose PDH. PDH is an energy-intensive process with a large carbon footprint, and splitting refinery propylene likely looks far less problematic from an emissions perspective, especially if there is surplus process heat on-site. In our ESG report today we talk about polymer recycling into new end markets, but polypropylene may see more direct substitution, especially if we see consumables related polypropylene recycled into durable polypropylene markets. This might dent demand growth for polypropylene going forward, but probably not meaningfully.

The ethylene price recovery in the US, discussed in today's daily report, is again a function of supply disruptions against a backdrop of robust demand. The net effect is to keep ethylene prices well above costs, at margins that justify investment and it is interesting to see the quick return of the CP Chemical project to the front burner. We could make a case that another ethylene facility in the US is likely a bridge too far at this point, despite the compelling current economics. The deep dependence on the export markets makes the US model very vulnerable to cyclical oversupply, and the current tight market is completely obscuring this risk and lulling producers into what we believe will be a misled sense of security. It is likely that the plants already built will prove to be good investments, not least because of the opportunity profits they are making in their early years of operations, but you would need to have a very bullish longer-term view of oil prices relative to natural gas to invest further, as even with an aggressive on-shoring manufacturing program in the US, the net export nature of the polyethylene businesses in the US is unlikely to change much. New capacity means more ethane demand, against a backdrop of lower E&P investment, and while Chevron has access to equity ethane from its US E&P operations, which may guarantee supply, it does not guarantee the price. Separately, while we believe that recycling targets in the US and the rest of the Wold will disappoint, they will still eat into virgin polymer demand. More chemical recycling will mean more “recycled” polyethylene available from heavy crackers – not ethane-based crackers.