The closure of the Russian oil pipeline and export terminal as well as the move to want payment in Roubles, are all likely tactics from Putin to cause more market chaos in an attempt to hit back over sanctions. While Russia likely needs the oil and gas revenues, sending oil higher is likely intended to see whether the West cracks, which seems unlikely. The Rouble payment is also meant to inconvenience the West but at the same time maybe support the Rouble as West Europe needs the gas and will need to buy Roubles to may payments.

The Lanxess guidance below is likely the right way to go for now. The medium-term effects of the Russia/Ukraine crisis are unknowable today and all companies can monitor is the immediate impact on their businesses. Most had entered 2022 seeing very strong demand growth and the promise of a much better year as COVID restrictions were lifted and economic activity picked up generally. Now all bets are off, as it is not just the primary impacts that matter – such as a companies’ direct exposure to Russia or Ukraine – note McDonald's is suggesting that pulling out of Russia will cost the company $50 million a month, for example – but also the secondary impacts of what the conflict is doing for supply-chains and pricing. Higher hydrocarbon pricing in Europe, for example, will impact the economics of all production, not just the products sold to Russia or Ukraine. There will also be some demand adjustments directly related to the conflict – disaster relief for example – more PPE – more spending on defense and defense-related materials – DuPont’s kevlar business should be seeing a benefit for example.

It is likely a difficult day for the European chemical industry as all of the fuel prices that they depend on are rising quickly, which will force many difficult decisions over the coming days. There are a couple of factors to consider – what happens to costs and margins if energy prices remain inflated, and what happens if energy availability becomes an issue and plant closures are necessary. In a world that is already reeling from inflationary pressure that we have not seen in four decades, there is at least an acceptance that prices can move higher, but the energy-dependent European industrial and materials companies will need to move prices quickly and meaningfully to absorb their higher costs. If natural gas supplies from Russia are halted, Europe is likely going to need to allocate supplies, as there is no easy fix given an LNG system that is already at capacity. Industry will likely take the hit to ensure power for heating and cooling. This will drive product shortages in Europe, especially for chemicals, which will likely make it easier to get the pricing necessary to cover costs.

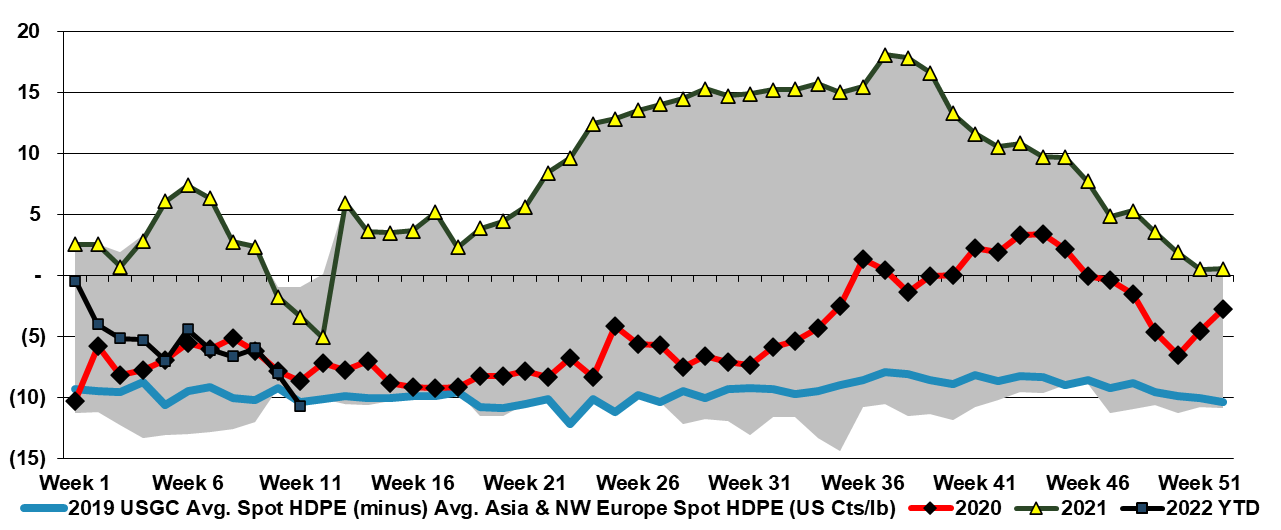

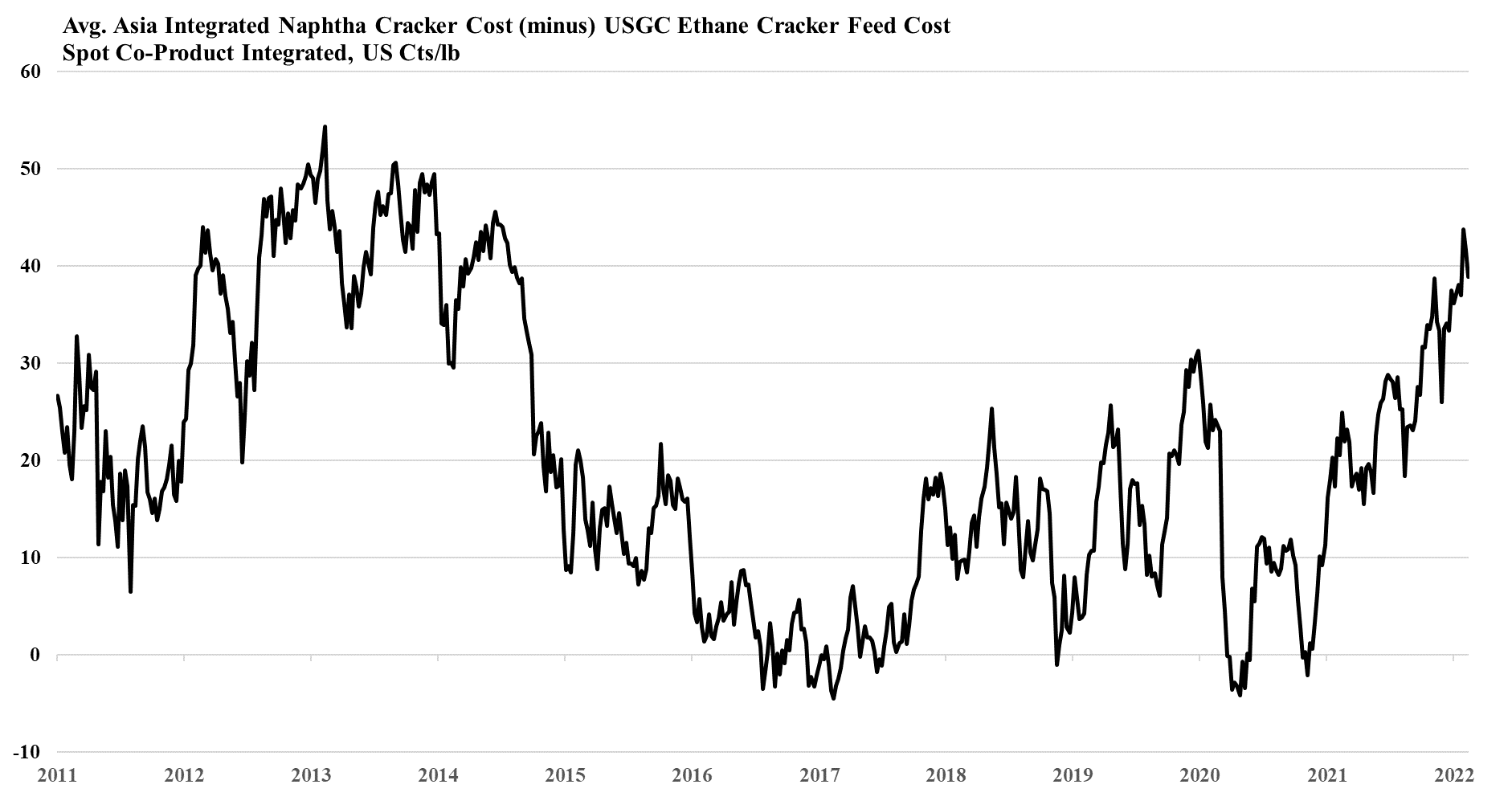

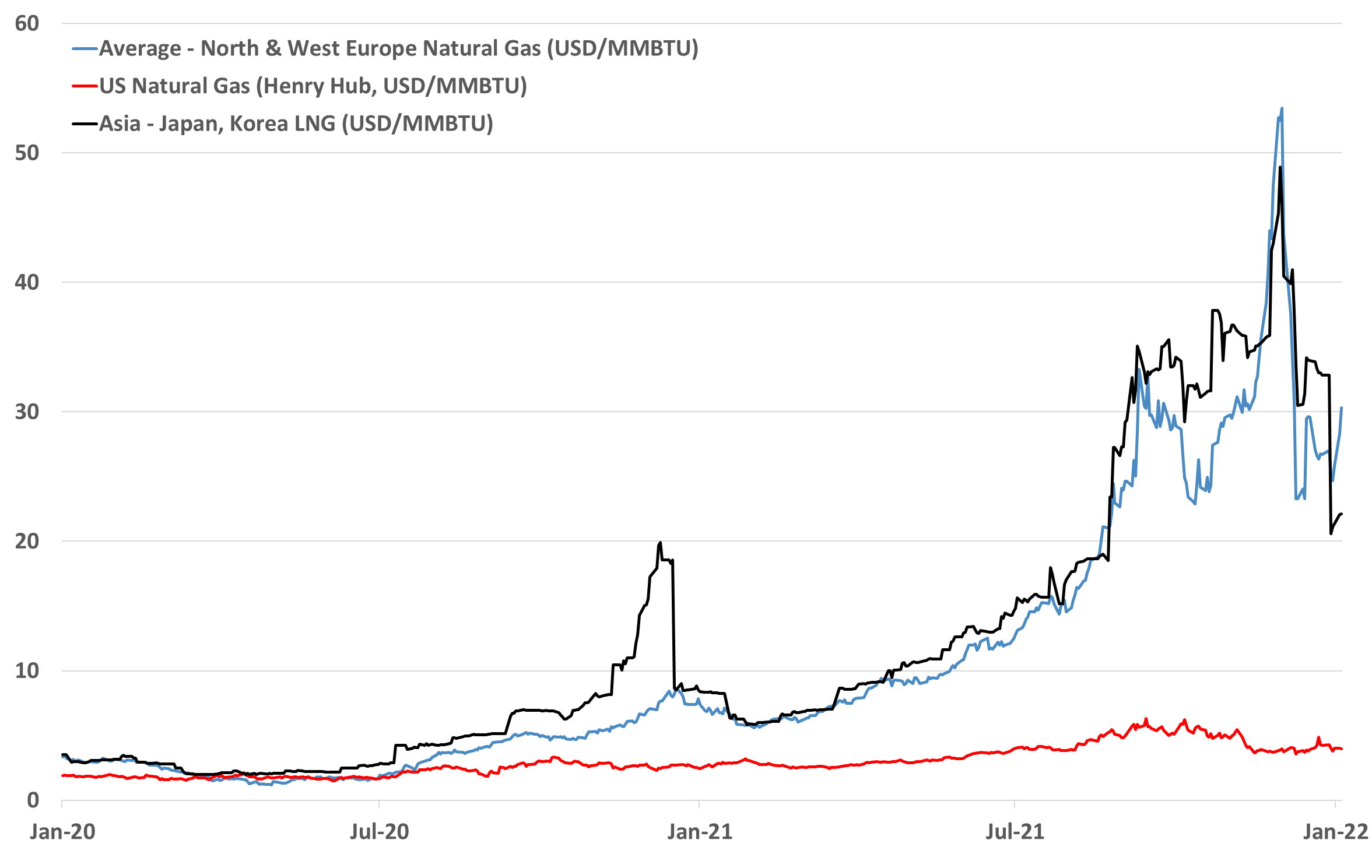

There are a couple of related topics in the charts below from today's daily report, as any conflict with Russia would almost inevitably impact European energy supply, raising prices for natural gas and pulling on as much LNG as possible. That said, we suspect that part of the recent run-up in prices has likely been to build a cushion of inventory, as much as that is possible with limited storage relative to demand.