The CP Chem propylene splitter announcement linked suggests that CP Chem expects surplus refinery propylene to be around for the long-term, and likely has supply lined up from the parent companies. However, this is still a bit of a gamble unless both parents see a scenario where they would change catalysts on FCC units longer-term and run at higher severity for more propylene and more hydrogen. This project looked a lot better only a few weeks ago than it does today – based on the spread in the Exhibit below, but propylene demand continues to grow faster than ethylene demand in the US and with all incremental ethylene capacity based on ethane, propylene consumers either have to choose the path from refineries or invest in on purpose PDH. PDH is an energy-intensive process with a large carbon footprint, and splitting refinery propylene likely looks far less problematic from an emissions perspective, especially if there is surplus process heat on-site. In our ESG report today we talk about polymer recycling into new end markets, but polypropylene may see more direct substitution, especially if we see consumables related polypropylene recycled into durable polypropylene markets. This might dent demand growth for polypropylene going forward, but probably not meaningfully.

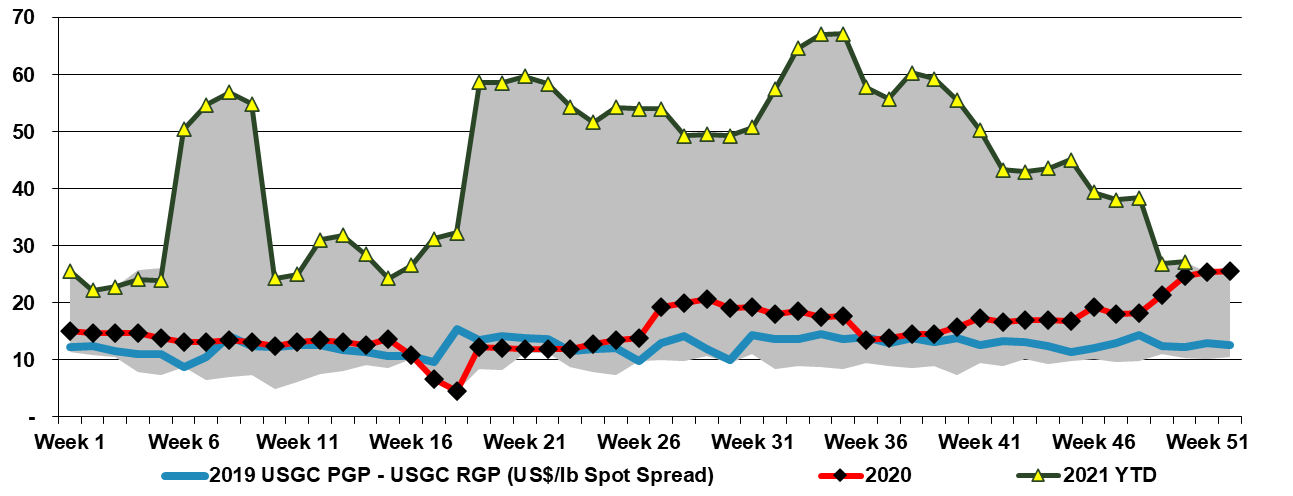

The polypropylene chart below, shows just how much of an impact the polymer has on the “average” in Exhibit 1 from today's daily report. Polypropylene is the only large volume polymer that can afford the freight rates to move surpluses from Asia to the US today and while some material is moving, volumes remain limited by the high cost of shipping and some of the additional logistic hurdles getting truck-based materials to US consumers that generally take the product by rail. The very high polypropylene margin in the US is a function not only of very strong demand but also demand that is likely growing faster than expected, giving buyers little negotiating room to get materially lower pricing. A year-end inventory correction from polymer buyers might send prices lower more quickly, but we have yet to see much evidence. We remain surprised by the apparent demand for polypropylene in the US given the lower automotive throughputs in 2021.