The closure of the Russian oil pipeline and export terminal as well as the move to want payment in Roubles, are all likely tactics from Putin to cause more market chaos in an attempt to hit back over sanctions. While Russia likely needs the oil and gas revenues, sending oil higher is likely intended to see whether the West cracks, which seems unlikely. The Rouble payment is also meant to inconvenience the West but at the same time maybe support the Rouble as West Europe needs the gas and will need to buy Roubles to may payments.

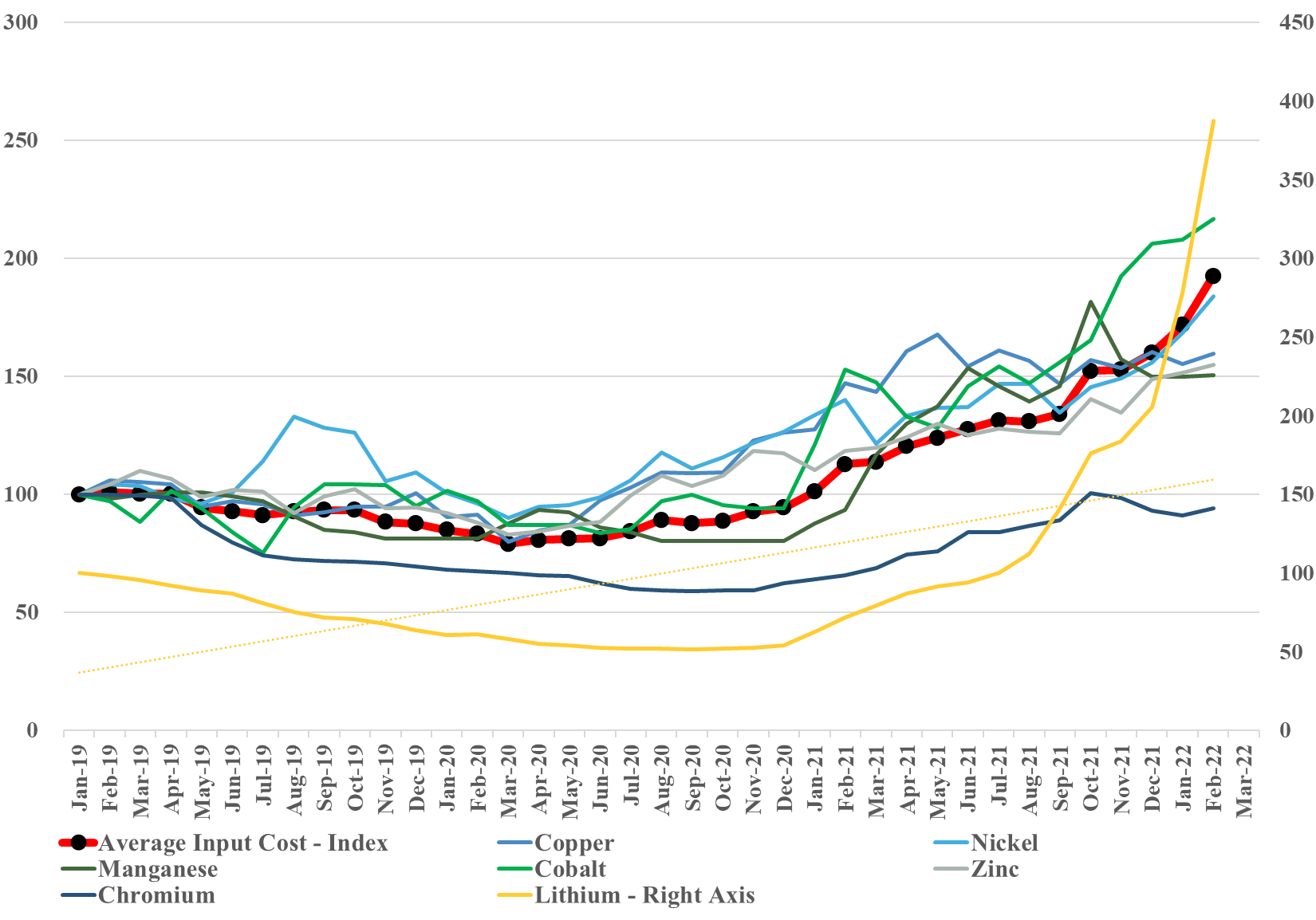

One of the key messages from the World Petrochemical Conference is that it is not an oil shortage, it is a commodity shortage, and we show our key metals index (updated through February) again in the chart below. We will update this again at the end of March (when consistent data is available) and given what has happened to both lithium and nickel prices we would expect a jump in the March index.

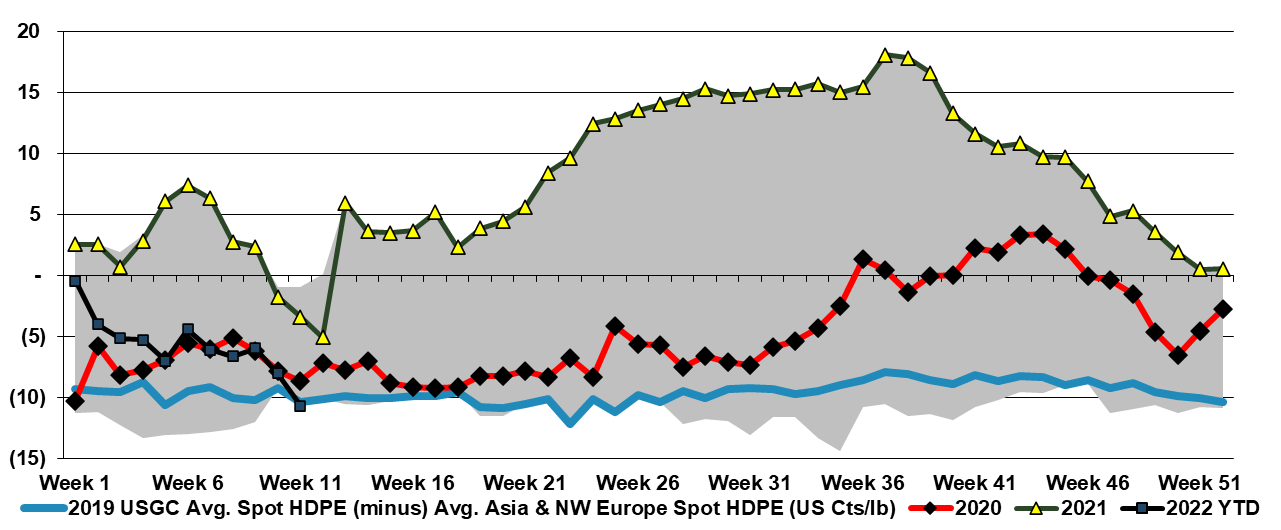

With the rapid jump in international natural gas and oil prices, we would see very concerted efforts to raise basic chemicals and polymer prices in Europe and Asia and will have a positive knock-on effect for the US. In our weekly catalyst report on Monday, we showed that ethylene producers outside the US were all losing money, especially in Europe and Asia. Some European demand will already be lower, because of curtailed product exports to Russia and Ukraine, but producers will want to cover costs at a very minimum and consequently, will be trying to match price increases with cost increases and if possible do a bit better than that. All of this will create a greater margin umbrella for the US, and US exporters selling directly into international markets will see export margins step up and may see incremental opportunities to export more, assuming that the freight rates are not too onerous for incremental containers.

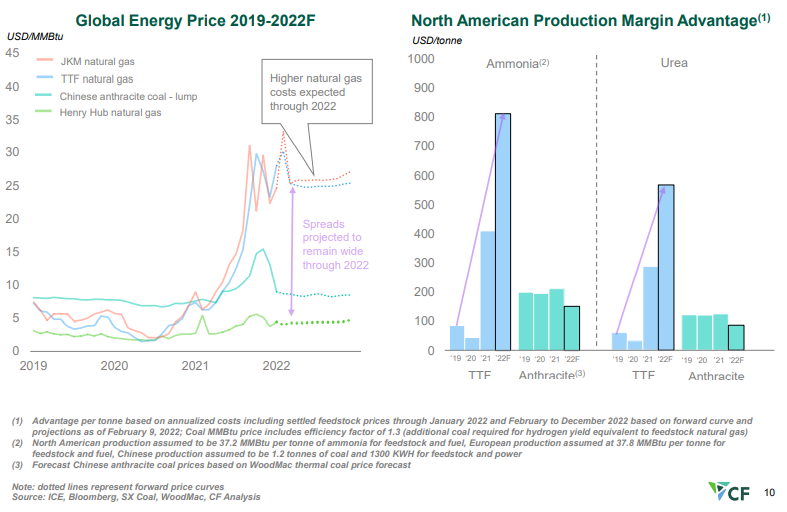

The CF slide below shows very clearly the US competitive edge when it comes to making anything that has a natural gas base, and while we tend to talk mostly about ethylene, ammonia, urea, other ammonia derivatives, and methanol are all seeing significant cost advantages. The Chinese coal-based costs are better than those in Europe and Asia based on natural gas but margins remain well below those in the US. The challenge with the coal-based chemistry in China is that it has substantial CO2 emissions, and the facilities were not designed for carbon capture. As China develops a carbon cap and trade market and as these facilities get included, costs will rise significantly.

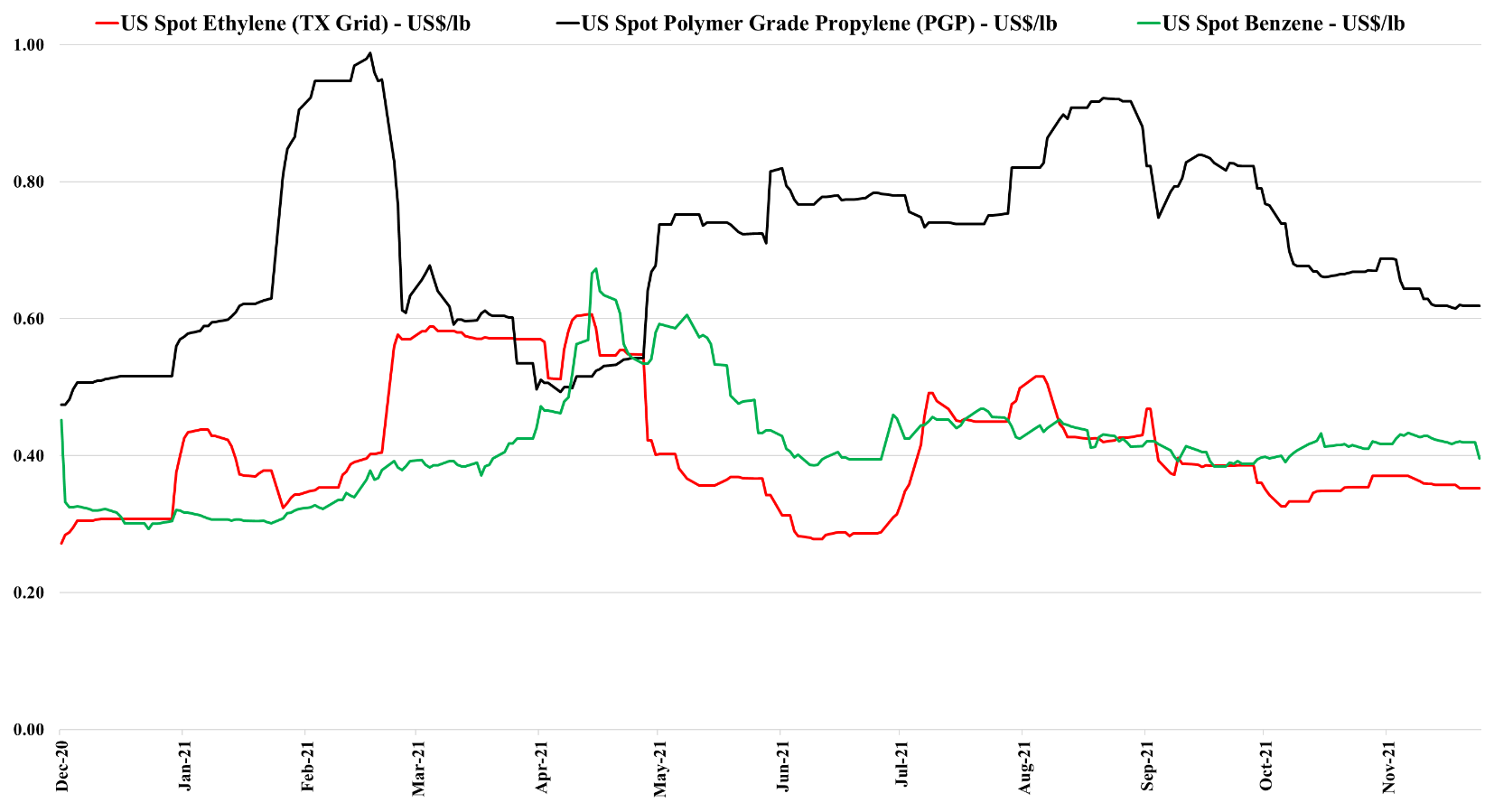

The drop in US benzene pricing is likely a function of lower crude oil pricing and the overall impact this is having on oil product values. As the US has moved to much lighter ethylene feedstocks, the proportion of benzene that is coming from refining is overwhelming and alternative values for benzene or reformate in the gasoline pool are a strong driver of US and international pricing. Lower naphtha pricing for ethylene units outside the US will also hurt benzene values. By contrast, the stronger natural gas market – through the end of last week - supported ethane pricing in the US and we saw a step up in propane pricing – which have provided support for ethylene and propylene – also note that the analysis we published yesterday in the weekly catalyst suggests that the US can export ethylene to Asia at current prices – delivering ethylene into the region below current local costs. This should keep a floor under US ethylene pricing although any further decline in crude oil prices relative to US natural gas and NGLs will close this arbitrage.

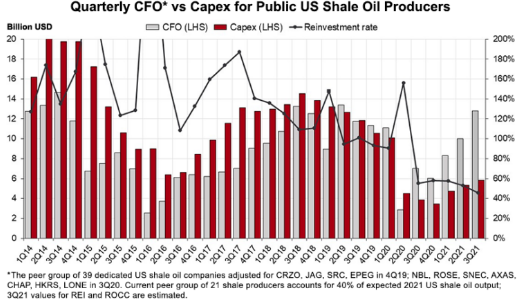

We should probably link the message in the exhibit below with the write-ups in both today's daily report and today's ESG and Climate report. The drop in E&P spending relative to cash flows and the shortage signals that are evident from the current oil and natural gas prices is likely to bump into rising hydrocarbon demand for the next several years, while the rate of renewable investment tires to catch up with energy growth before it can focus on energy substitution as meaningfully as the climate agenda would like. We also cannot look at the chart below and say that it does not matter because oil is less important in energy transition than natural gas. The oil-based investments in the Permian and Eagleford plays, in particular, have significant volumes of associated gas, and much of the natural gas supply growth in the US has come from these oil-centric investments. As they slow down, natural gas supply and NGL supply will be impacted, and while we are seeing increased rig counts in the natural gas biased regions, such as the Marcellus, the potential declines from the other fields will be hard to make up for.

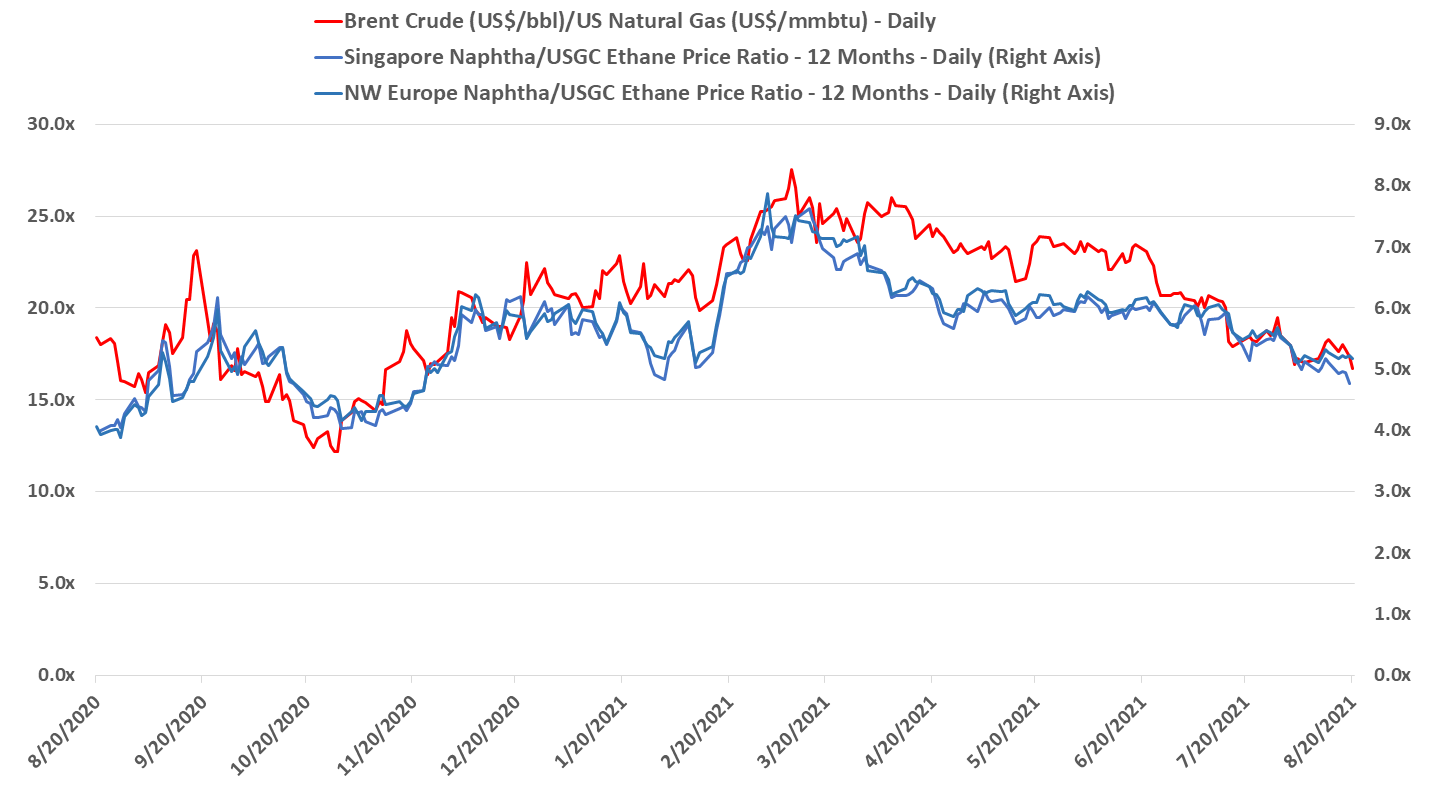

The slow decline in the oil/natural gas ratio that has persisted through the year continues – this time oil is falling faster than natural gas as both are reacting to slower demand or expectations of slower demand. We are unconvinced that the price declines will continue, but it is much less clear which direction the ratio will move. OPEC+ has far more chance of keeping cash flows high by trimming volume to balance the oil market and the overwhelming strategic logic of such a move means that it is a likely path – there is no 10-20% boost to demand to be found by lowering prices. US natural gas is still on a medium-term demand march higher in our view and more limited E&P spending should keep the market balance quite tight. There are no near-term large increments of new LNG capacity on the horizon and consequently, inventory and pricing will likely bounce around on weather changes for a while. See more in today's daily report.

The Halliburton forecast of an upcycle for oil services likely needs to be put into context, as while activity should rise in the sector with higher oil and gas prices, it is unlikely that we will see a major boom. The uncertainty in the energy market, coupled with ESG pressure and borrowing constraints means that the oil industry will likely focus on its lowest hanging fruit first and may hold off on secondary opportunities completely. The oil service guys will benefit because the more productive shale wells can require longer laterals, deeper wells, and more fracking pressure, but it will likely be quality over volume when it comes to drilling activity, in keeping with what we have seen year to date.

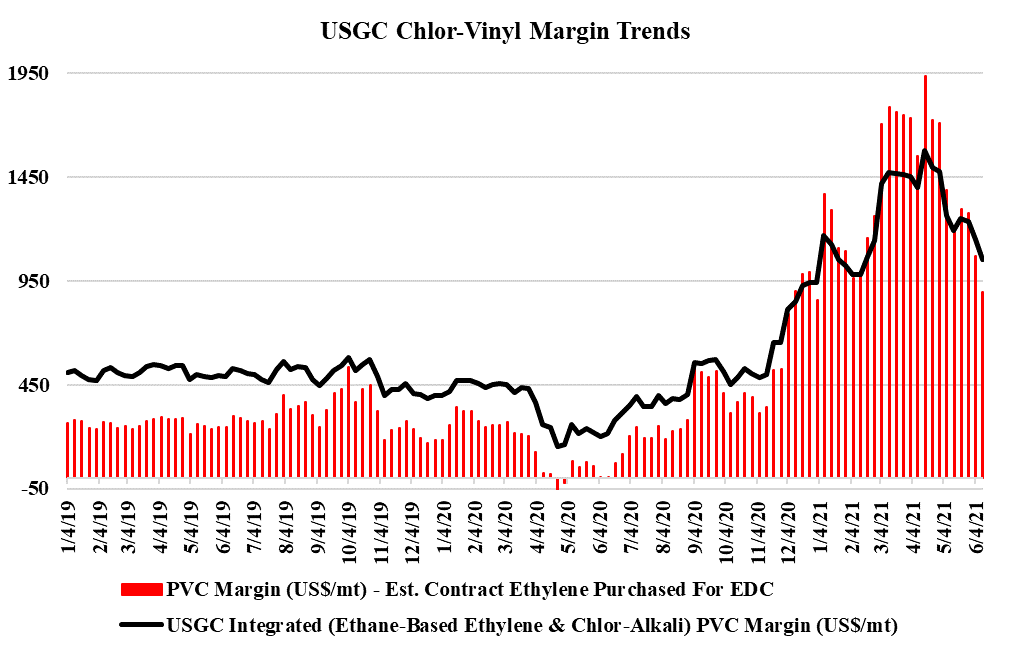

PVC margins are off their highs, as pricing is falling through June. The building product markets remain robust in our view, albeit off their highs, and some of the strength in PVC in April and May was a consequence of production shortages caused by the winter freeze in February. While PVC may be falling faster than polyethylene today, we see support for US PVC at higher prices and margins than for polyethylene in a weaker market unless oil climbs further relative to US ethane. See more on our daily report.