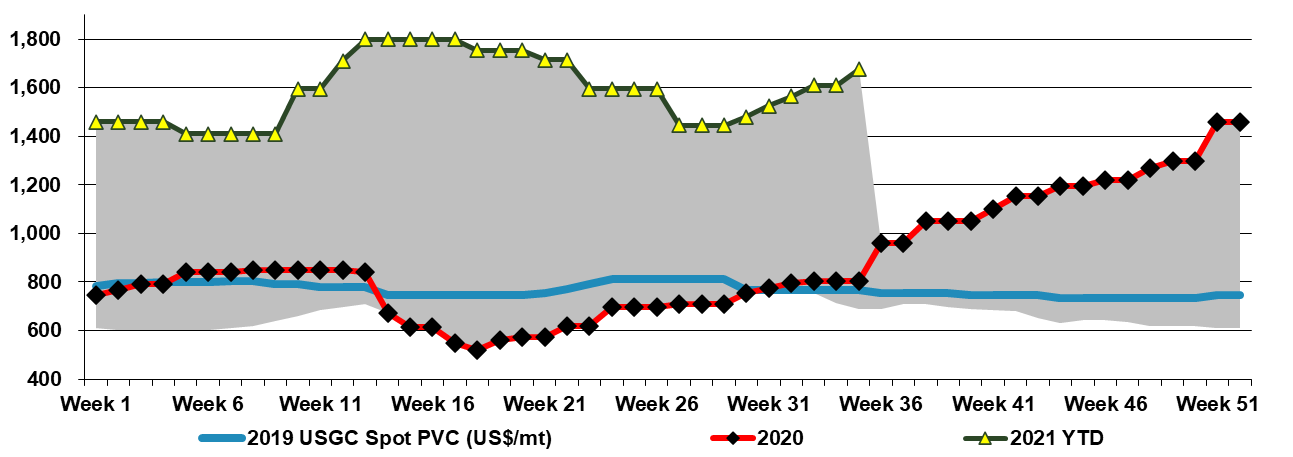

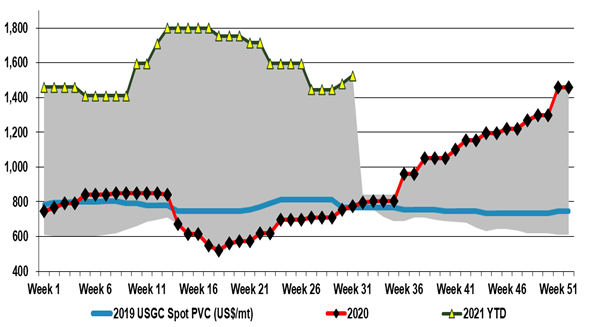

It is increasingly likely that Hurricane Ida will add another leg of strength to US chemical pricing more broadly, with a host of prolonged production outage news and force majeure notices, giving momentum to some price increase announcements for September, some of which looked very speculative at the time they were made. Buyers will have an eye on continued pockets of supply chain disruption, strong demand in general, particularly for those levered to holiday spending, and the not insignificant fact that we still have almost three months of hurricane season to go! Note that two of the more disruptive storms of 2020 hit in October. We talk specifically about PVC in today's daily - See price chart below.

China trade data for chemicals and polymers points to a dramatic swing in net imports, partly due to the new capacity added over the last 12 months. Imports are down, and exports are up. Despite the logistic challenges of moving the products and the powerful pull on consumer durables from China driven by US and European demand – much of which consume significant volumes of polymers and chemicals locally. The trade swings talk to the significant capacity additions and the relatively sluggish consumer within China, where spending patterns remain subdued because of the Pandemic. Even with a recovery in domestic spending, China has probably added 2 to 3 years of demand growth in current capacity adds – most notably for polyolefins and PET, but also for styrene, where we believe demand growth could be slowing. If logistics improve and container rates come down, the surpluses in China will have a severe negative impact on international prices. This development will likely be seen in either polymer quantities flowing faster/more freely around the globe or because the export rate of consumer durables will pick up even further at the expense of durable producers in the US and Europe.

Is this the beginning of the end? The linked report that US traders are struggling to find export homes for incremental HDPE should not be a surprise given the significant price difference between the US domestic price and prices in other markets – Exhibit 1 in today's daily report. HDPE is the more fungible polyethylene, with both LLDPE and LDPE much more grade and application-specific. It is often the first polyethylene grade to spike in a shortage and fall when there is a surplus.

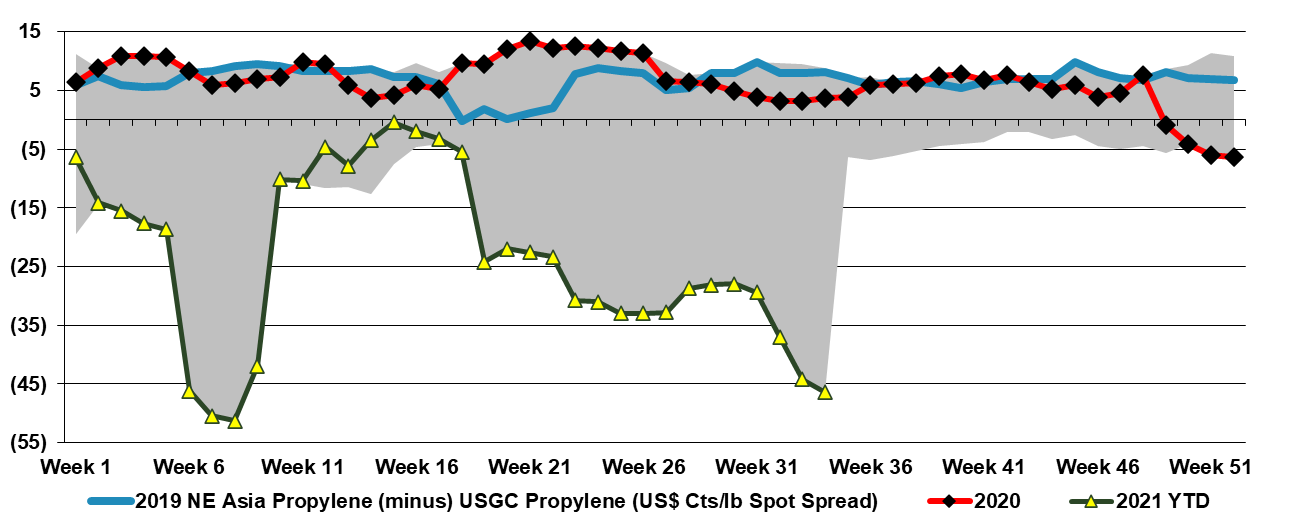

The regional polymer price chart below shows the extreme divergence of prices between the US and Asia, and it has hit a level that has never been reached before. It is in part a function of the wave of new capacity that hit China in 2H 2020 and 1H 2021, which spurred oversupply in some chains, and the dysfunctional global trade backdrop that has kept global supply chains out of balance. As we noted earlier this week, the container costs alone to move polymers from Asia to the US are, best case, 34 cents per pound today, and this is estimate does not include the cost of moving the product to a port in China or from one in the US and also does not include a working capital charge for the time in transit. There would need to be an arbitrage of 10-15 cents a pound above this to make product movements between these regions worthwhile, assuming you can find a buyer in the US willing to experiment with imported products. The other trade impact is that US retailers and manufacturers are pulling on their US suppliers to maximize supply, pushing domestic demand for polymers above trend. The lumber price moves in the US – Exhibit 1 in today's daily report – if they spur incremental home building, it will be another boost for domestic PVC demand.

We are seeing some of the same dynamics in PVC that have been prevalent in polyolefins this year with some weakness in Asia – although not as much as we are seeing for polyolefins - while markets in the US and Europe are finding enough support for prices to go back up again. As with other polymers, any possible arbitrage between Asia pricing and the West is quickly consumed by the higher container rates. PVC has seen less capacity added over the last few years compared to other polymers and while it has not seen much of a boost from the change in consumer spending patterns around packaged goods and durables (as it has more limited exposure to packaging and durables), it has benefited from strong housing demand and some initial infrastructure spending – with more to come around the globe. The blue sky scenario for PVC would be one in which some of the growing clean water issues that are emerging in many parts of the world move more to the front burner as PVC would be a major beneficiary on investments in desalination for example or simply from water infrastructure upgrades.

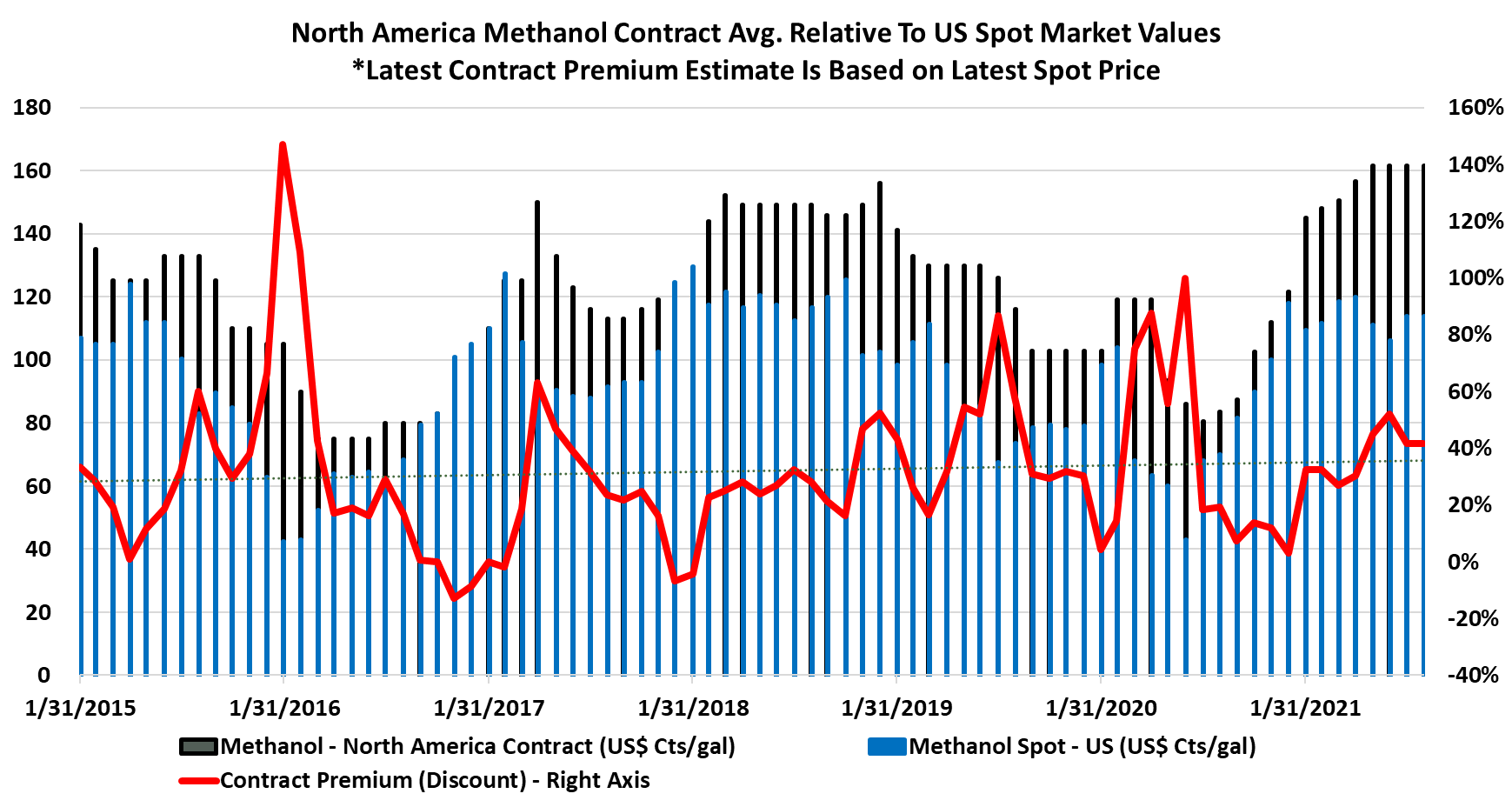

Methanol prices in the US remain very robust and quite profitable for producers, despite weakness in China. The higher natural gas price in the US (see today's daily report) provides some support for methanol pricing, but ultimately coal-based methanol in China will win out if US costs keep rising and this may curtail demand for US methanol at the margin. As with all other chemical and polymer markets today, freight costs are making it difficult to play off some of these apparent regional arbitrages and the US methanol producers would have to be somewhat reckless to upset the balance domestically and give up the margins that they have today. Domestic demand for methanol derivatives is high and the LyondellBasell accident may provide more pricing strength through the acetic acid chain. While the incident will decrease the demand for methanol, LyondellBasell should be able to manage this, and higher pricing in the acetic chain would mean that consumers would have no issue paying current prices. Higher MMA production in the US – implied in the headline below - should keep methanol demand high.

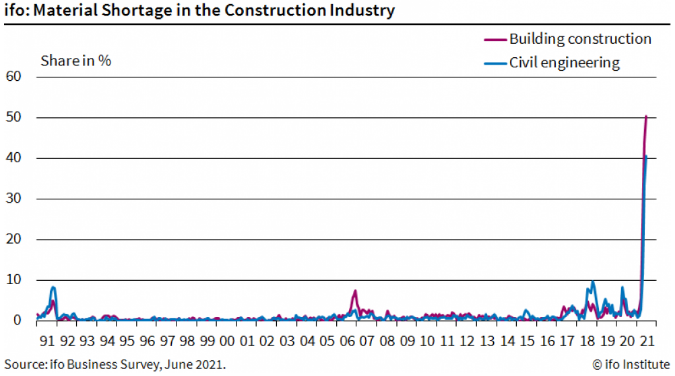

The German materials shortage chart below is certainly eye-catching. There is nothing even remotely close in 30 years of history. We see this as further confirmation that we should continue to expect high shipping rates and congested ports until surveys like this show significantly better results and it is also further supportive of inflation. While it is extremely difficult to forecast from here, we would use the pendulum or spring metaphor – the further you pull either in one direction, the further they swing or spring back. The current dislocation is so extreme that everyone in the chain is likely acting instinctively and working to find greater supply and greater supply security. At some point, both end-demand and demand to fill inventories will normalize – either back to trend or back to a higher trend, but the inventory build piece will end and we will either get a gradual retreat in the scary data – such as the spike in the chart below – or we will see an equally quick collapse, at which point pricing will likely take a hit down the chain, with basic chemicals particularly vulnerable because the world has been adding substantial new capacity over the last several years in the US and China. More investment may be needed to keep up with higher trend demand in many intermediate or end-products that consume base chemicals and this could keep pricing supported, but basic chemicals and polymers look especially vulnerable to a reversal in the supply chain build we have seen for the last 9 months. For more see today's daily report.

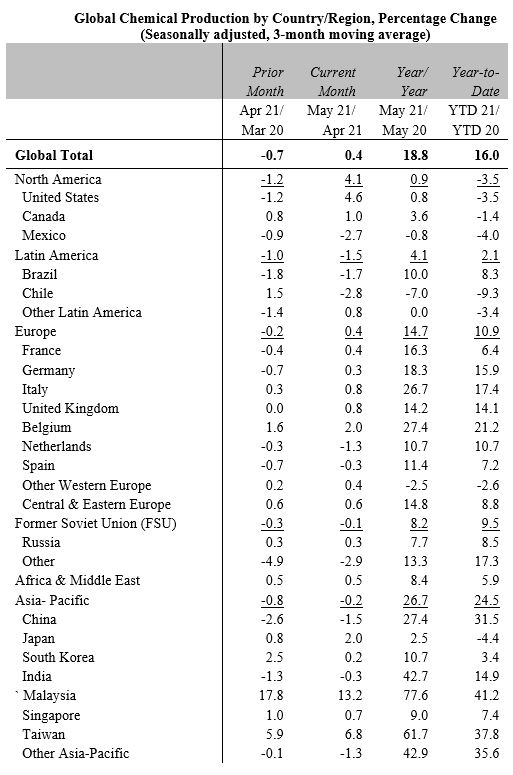

The ACC May production data shows the very strong year on year production growth globally, with the US gains more muted than the rest of the world as the COVID production impact in May of 2020 was less severe in the US than in many other parts of the world, and the China growth has been further assisted by significant capacity additions since this time last year. It is interesting to note that on a year to date basis the US is still down year-on-year, which is the lingering impact of the winter storm on production and it reflects that there is not much space capacity in the US, given both the strong demand and the export economic advantage of lower feedstock costs. Despite the collapse in prices in Asia – very well reflected in Exhibit 1 in today's daily report – the US has enough margin to continue its derivative and ethylene exports.

We think the India styrene plan is ill-advised. The styrene market has had a brief moment in the sun over the last couple of years, but we believe that it has another leg down ahead, based on the recycling complications of polystyrene versus other packaging polymers. New capacity in China and likely weaker demand in the US and Europe should push the global market into oversupply for a prolonged period (if not permanently). This is bad news for styrene (or polystyrene) producers but very good news for the non-integrated producers of styrene derivatives targeting the durables markets – such as Kraton.

See today's daily for more on this, but while the freight rate moves are more than likely going to correct to a degree at some point, their continual escalation has multiple implications for the chemical and plastic industry as they are most impactful on cheap imports from Asia targeting low-cost furniture, appliances, toys, and household goods where the base cost of the product is low and the move from $3,000 to $10,000 per container wipes out any advantage of manufacturing offshore.