With the rapid rise in energy prices, we are seeing price increase announcements for many intermediate chemicals, especially in regions of the world where margins were already very slim. The energy inflation issue is hard to call, with more and more commentators suggesting that it could be prolonged (which generally means it will be short), but lots of dislocations support duration. We would certainly be pushing prices today on the back of energy costs that could move higher again, and given that many chemical and polymer buyers have price protection in their contracts (for at least a month), producers could face a margin squeeze and an uphill climb to get adequate price coverage. Seasonally, demand for chemicals and polymers is at its weakest for the next couple of months, so the price hikes may be difficult. However, because of supply chain constraints, buyers may feel less confident and concede more easily. We could see a significant swing in sentiment from the chemical companies on 3Q earnings calls over the coming weeks as they talk about how good results were in 3Q but throw up all sorts of cautionary statements concerning 4Q.

Our latest Sunday Thematic report, "Damned if you Dow and Damned if you Down’t. Hard to win", centers around Dow's announced development of a new net-zero carbon emissions site in Alberta, Canada. It discusses company-specific and sector ramifications for Dow's strategic move to produce low-cost low carbon polyethylene in Canada while also expanding capacity.

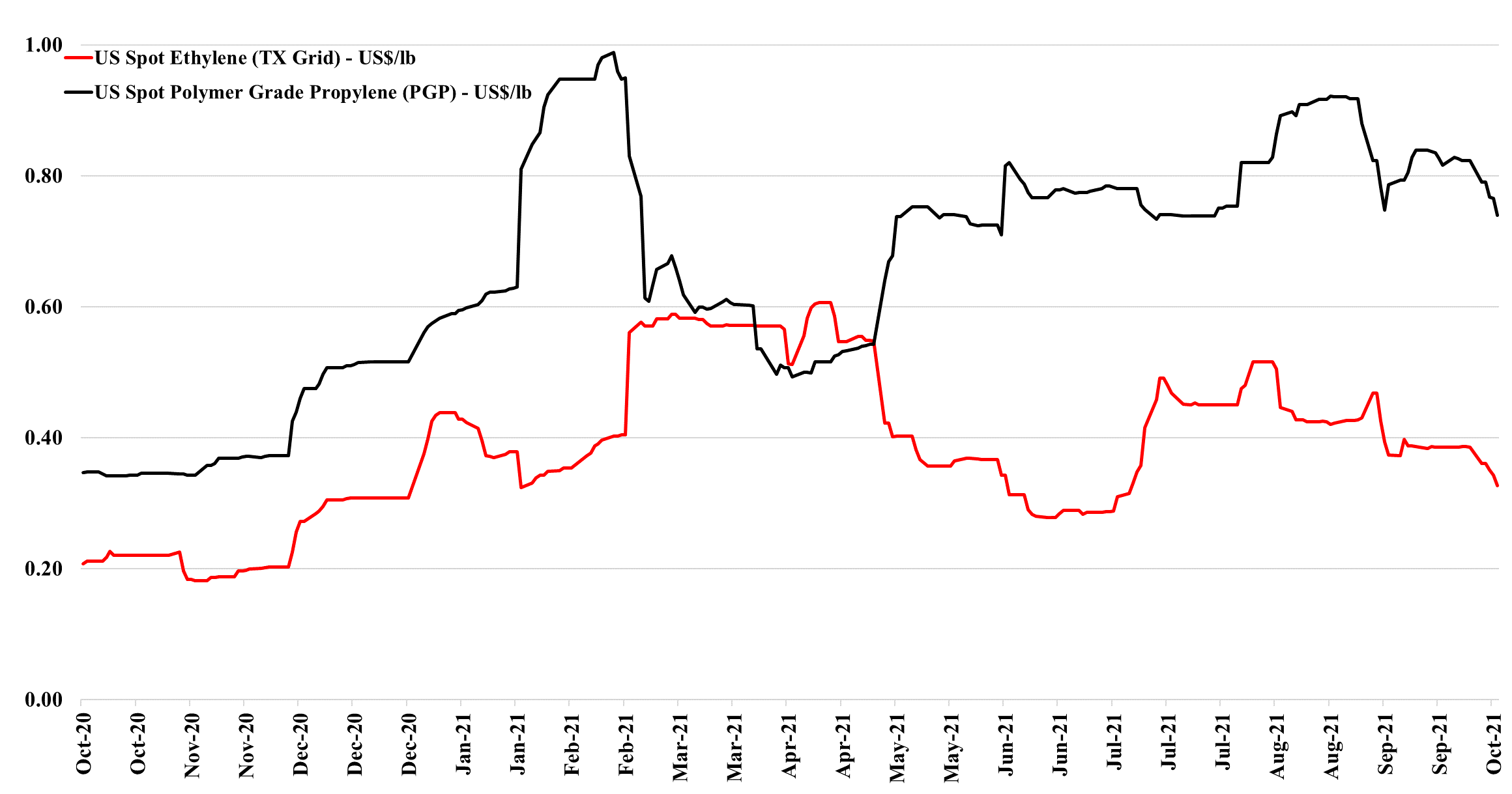

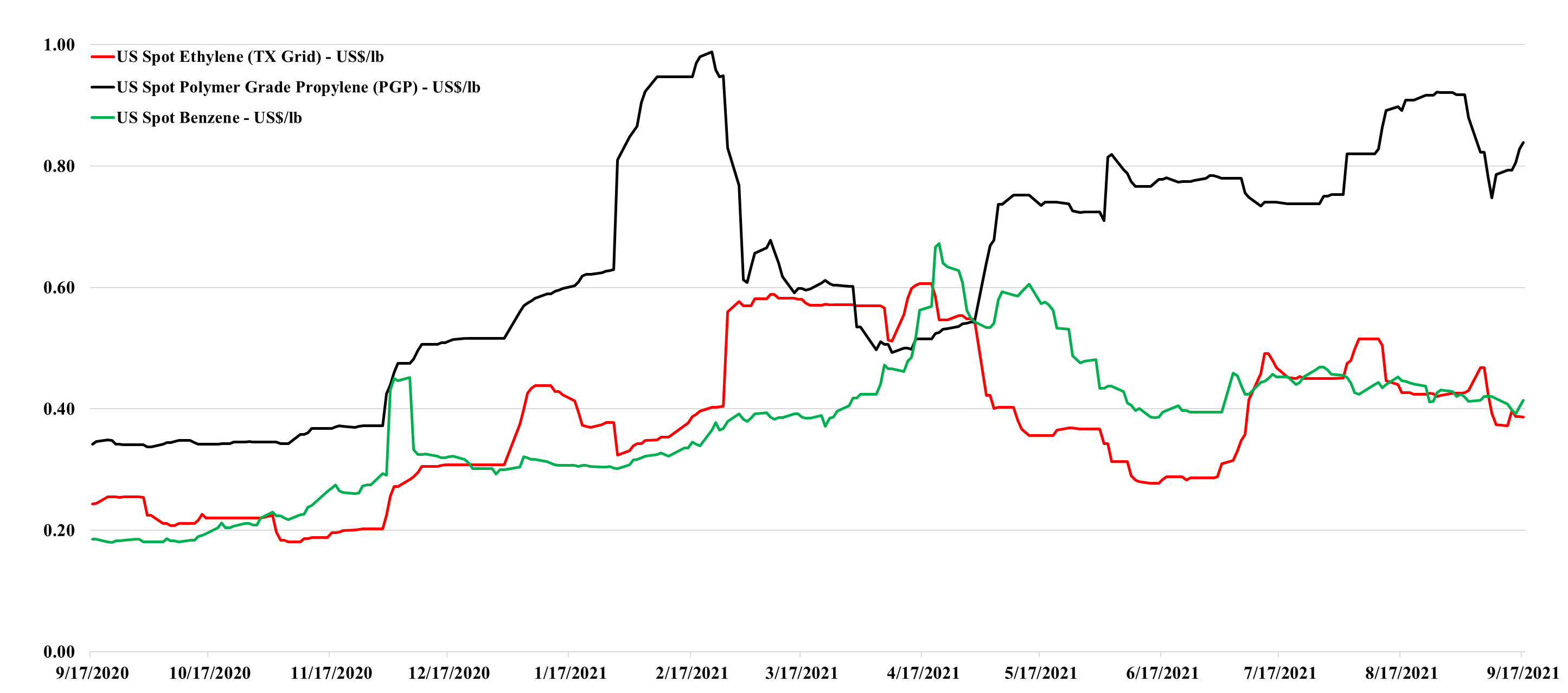

While we will talk more about the Dow project in Alberta on Sunday, one of the problems that the stock faces in the light of the announcement is largely unrelated, which is the growing expectation that margins in 2022 will be significantly lower than in 2021. This is the view coming out of the recent EPCA meeting and as the ethylene/propylene chart below shows, monomer pricing is already weakening in the US as production ramps back up following the recent storms – we note in Exhibit 1 from today's daily report the squeeze on ethylene margins as prices fall, while costs rise. But it is also worth noting that margins remain quite healthy, while well below their highs. Those companies who built new ethylene capacity in the US over the last 5 years would have had a margin similar to the current level shown in Exhibit 1 in an optimistic capital case.

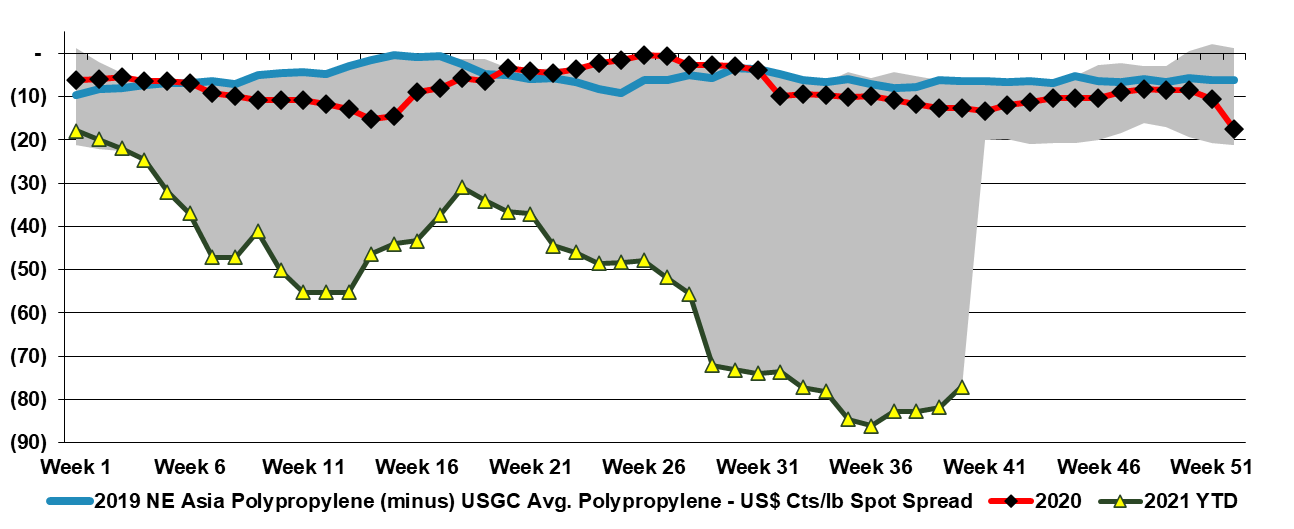

Even with the inflated container rates, the vast price difference between US and Asia polypropylene prices makes the opportunity too great to ignore. Even at their highest levels, container rates, and inland transport costs likely total no more than 35 cents per pound today, and as shown in the Exhibit below, you have plenty of room to maneuver. This is not the case with polyethylene or other polymers where the price delta between the regions, while high, does not cover the costs and the added risk of delays to sourcing. For more see today's daily.

We have discussed a theme around shortages that has been going on for months and is prevalent in many of the headlines today. It has also been a central theme of much of our energy transition work, as we think about the raw materials needed to meet the demand for solar and wind power as well as the infrastructure for hydrogen generation. The exception is lithium, where we see regular announcements around expansion projects, such as the one linked from Albemarle. The EV makers and battery storage manufacturers are doing an excellent job of encouraging investment in lithium, taking stakes in battery projects, and in some cases taking stakes in the lithium projects themselves. Offtake agreements also help projects get funding. We suspect that the offtake agreements are tactical – not aimed at buying out a source of lithium or a source of batteries but aimed at ensuring that a surplus of capacity gets built, to ensure no bottlenecks in the future.

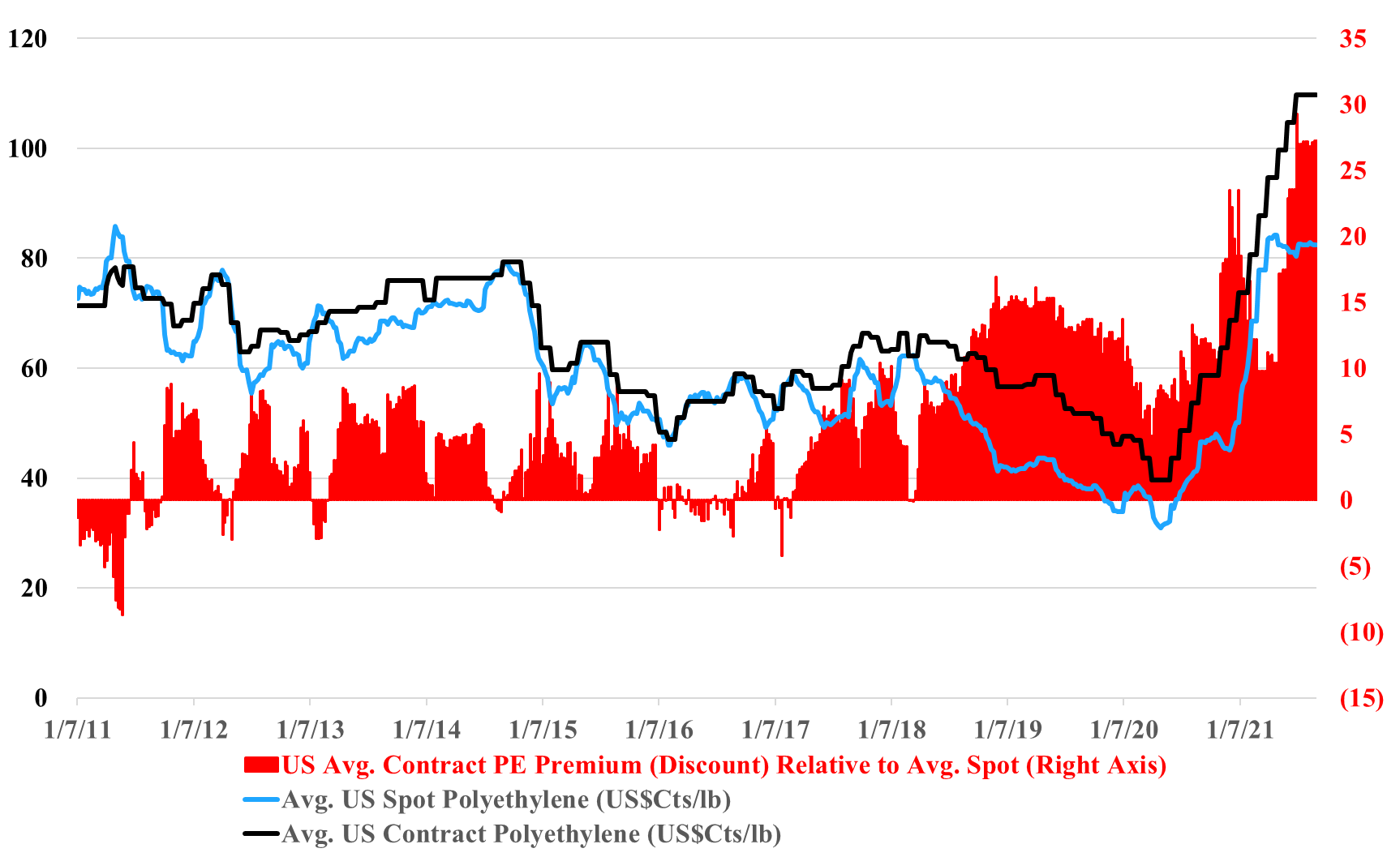

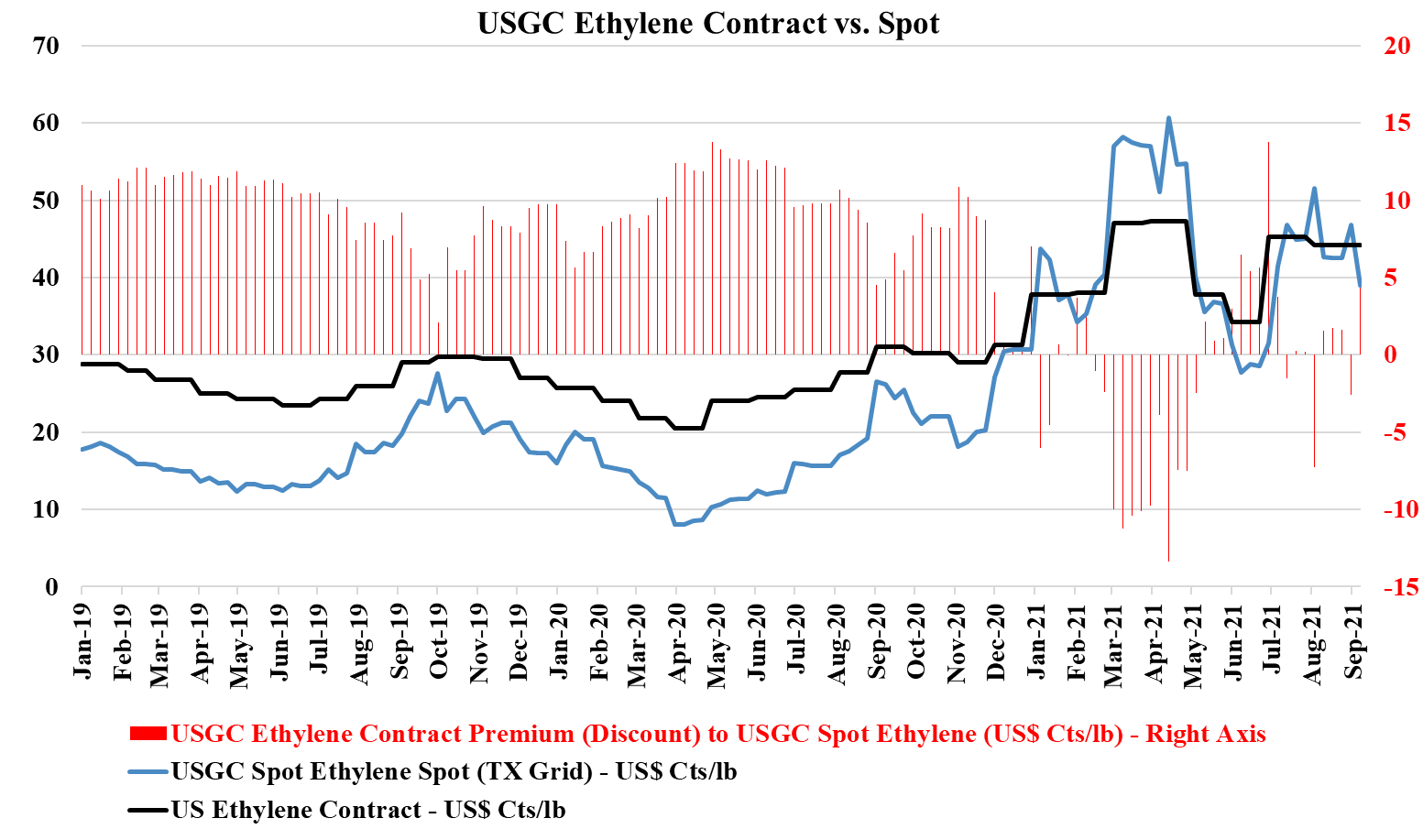

US polyethylene producers are pushing for September price increases and their arguments center around lost production, because of Ida and Nicholas, and rising costs because of the much firmer natural gas and ethane markets. Working against them are the very high margins and what appears to be a stubborn spot market, both covered in the charts below. A contract increase in September would maintain an unprecedented gap between US contract and spot pricing, and while it is likely that the spot market is very thin, it is a very strong push back against producers for a contract hike.

We continue to see significant volatility in US product prices, and this increases uncertainty around the underlying direction of the markets for the balance of the year. The recent storms have likely created enough production interruptions to take any slack that had been developing in August out of play, and while we see that in the most recent moves for ethylene and propylene – Exhibit below - it is likely more interesting to see what happens with polymer pricing as we move through the balance of September – as this will determine profits for most. While we focus on the high prices in the US more than we do the prices in Europe, it is also worth noting that European polyolefin margins remain very high, with one local producer confirming this week that records continue to be set in terms of cash flows and unit profitability. The frustration for the US producers impacted by the storm is that while their plant closures may be contributing to the tight markets, they do not get the benefit of the higher margins on the impacted facilities. While we would expect many to produce extremely high numbers for 3Q – a handful will likely lament how much they could have made had their plants operated fully. See more in today's daily report.

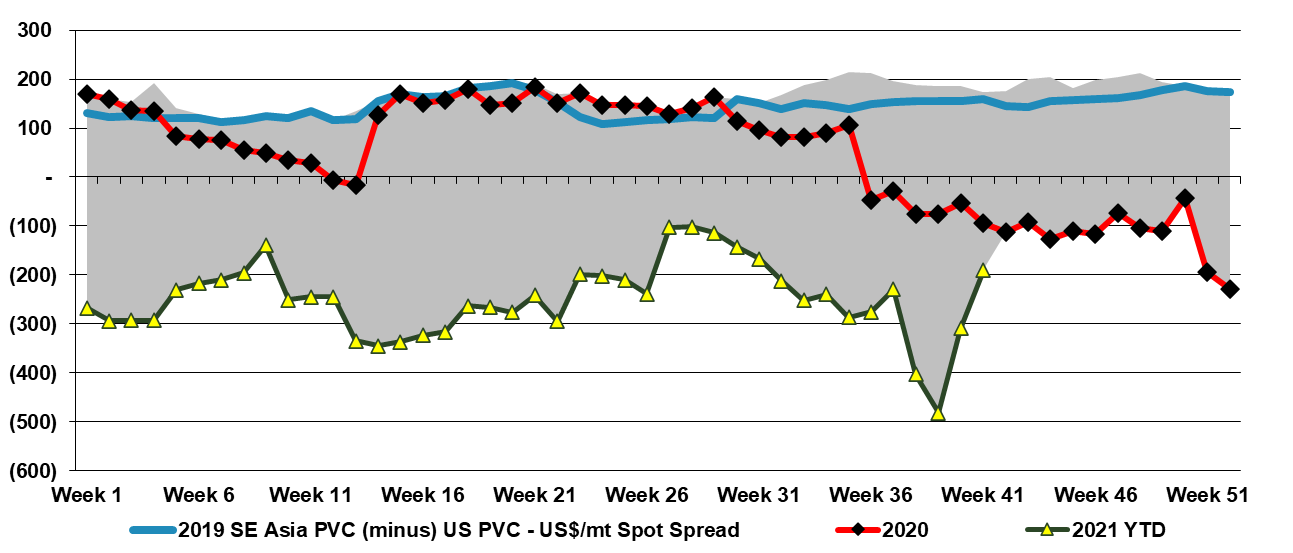

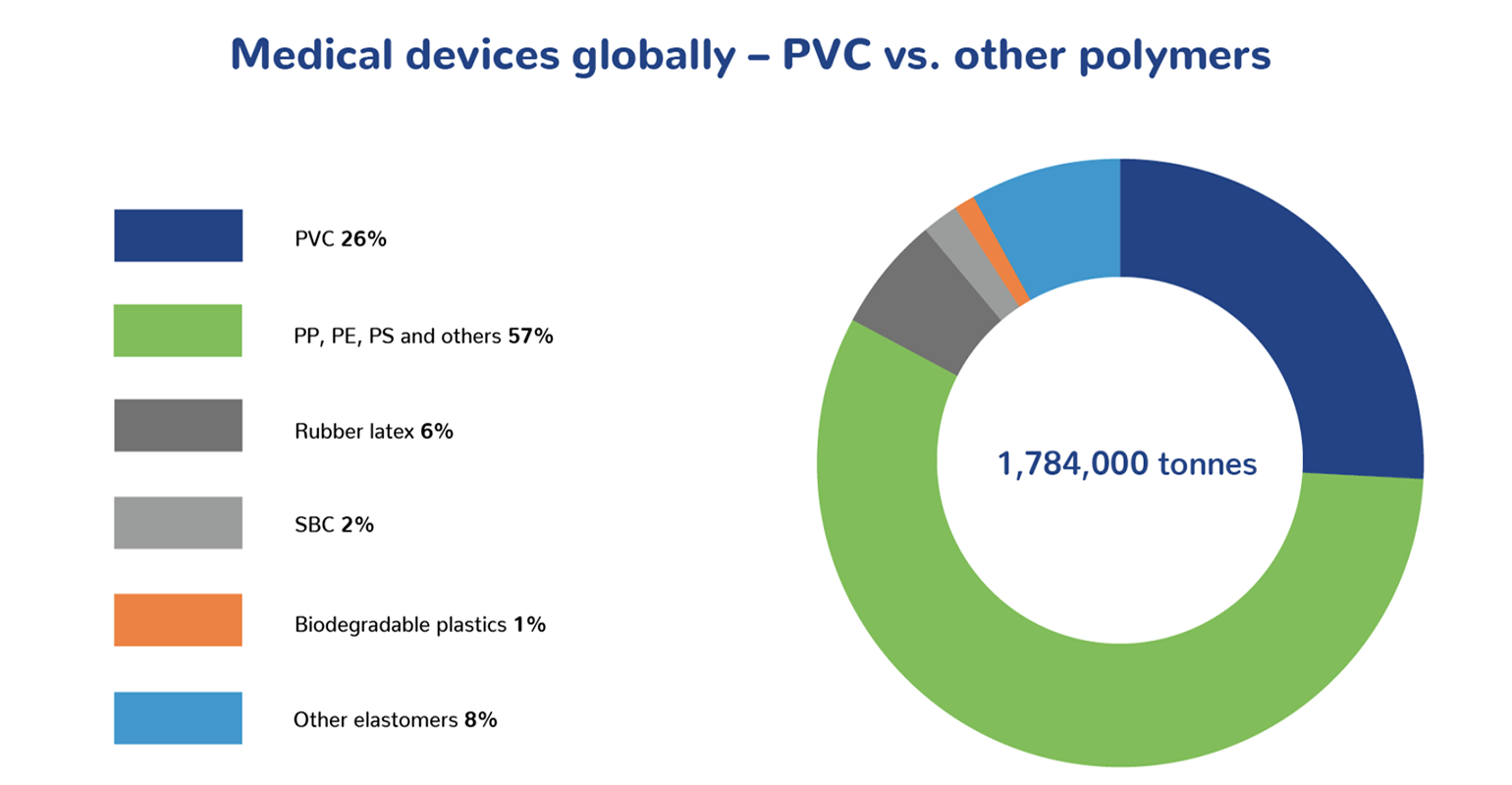

We have talked a lot over the last year about our preference for PVC as likely the better longer-term story within polymers – more stable growth – more limited global investment and less impact from the plastic waste moves, as very little PVC ends up in packaging. The exception is the medical device space, where demand for PVC in single-use applications is growing as illustrated below. While the medical device industry is setting up to use recycled PVC it is going to be hard to close the loop here as medical waste is generally quite contaminated and PVC does not do well in a conventional pyrolysis process because the chlorine molecule is a contaminant. The solution will likely be getting PVC from end-of-life consumer durables and recycling that PVC back into medical applications. Disposal of the medical waste is best done through a pyrolysis or gasification process that includes very high-temperature plasma technology. These facilities exist and operate well outside of the US, and we would expect to see broader acceptance within the US over time. See more in today's daily.

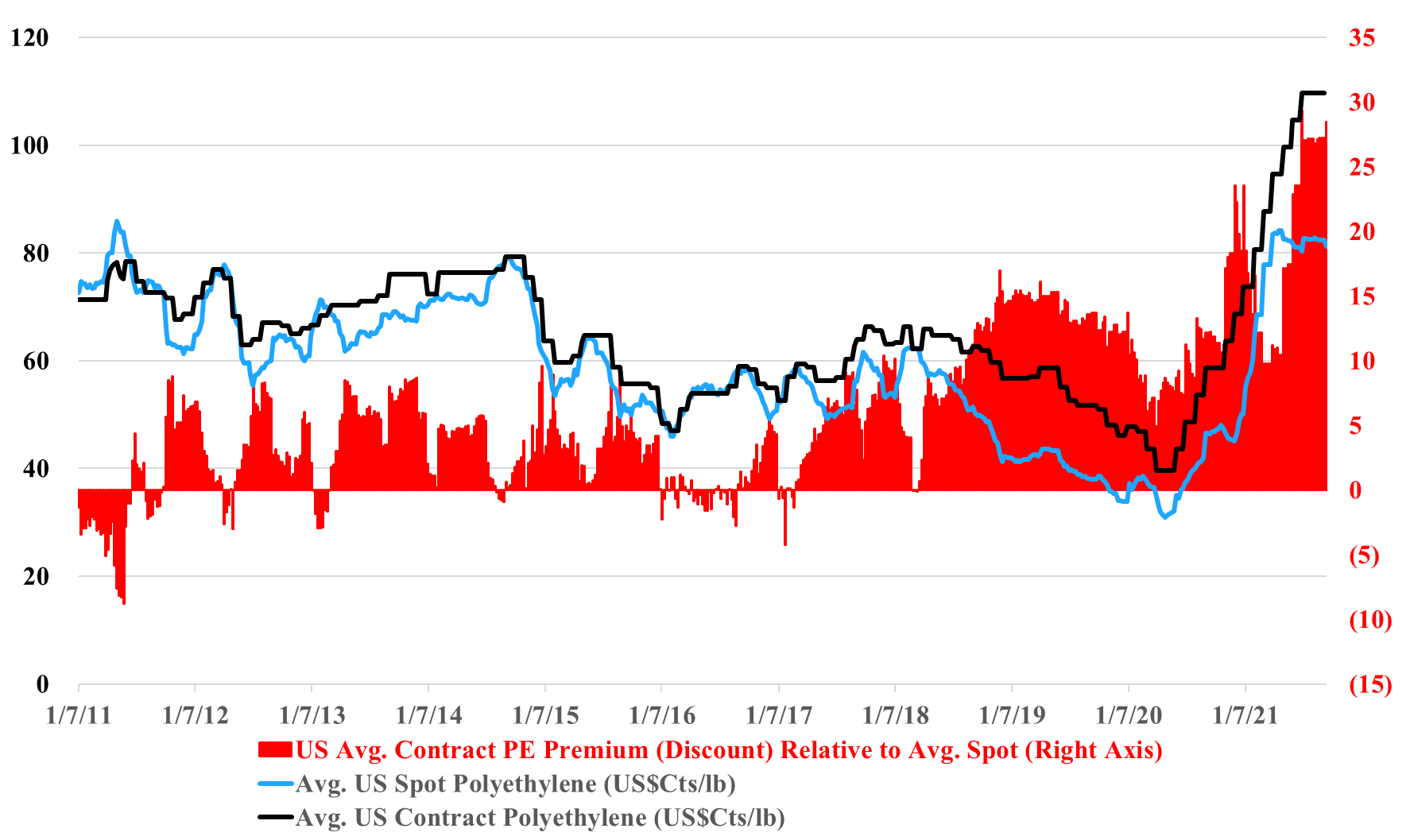

The gap between the US contract and spot price for polyethylene in the exhibit below looks wrong, and it could be wrong in absolute terms but the trend alone makes a statement. In the past, we have seen a couple of instances where reported contract settlements have drifted further from net transaction prices, either because of larger agreed discounts or because of contract formulae that reflect spot pricing to a greater degree. This tends to work for a while, but ultimately smaller buyers with more limited purchasing power become more disadvantaged and there is a breaking point at which the “contract” price is adjusted downwards by the price reporting services to better reflect what is really going on. The current market feels like the times in the past when an adjustment has been needed.

We saw the stable to downward trends in both US ethylene and propylene spot prices reverse at the end of 2020, in part because of recovering demand post the initial wave of COVID, but also because of storm-related production constraints in October and early November. The weaker spot markets for both ethylene and propylene today reflect much stronger production for propylene (all PDH capacity running) and Hurricane Ida-related upsets that have left the monomer markets less badly impacted than derivatives. Something similar happened in 2020, especially for ethylene, but the backlog of derivative demand cause a step up in ethylene consumption when everything restarted. This could happen again, and we are earlier in the Hurricane season. See today's daily report for more.