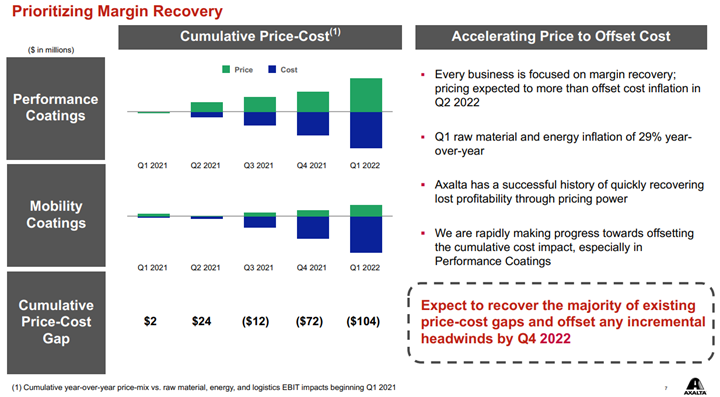

Axalta shows a helpful picture below of how pricing and costs are moving. All coatings producers are seeing the same cost inflation, some of it energy/hydrocarbon input related and some of it supply chain-related – either for inputs such as pigments or higher costs of getting products to markets. How pricing looks relative to costs is very customer dependent, as shown in the chart below. Auto OEM customers have long lead times on price adjustments and this is why Axalta is signaling the end of the year before prices will be aligned with costs. This of course assumes that costs do not rise again in 2H 2022 as they will also drive a lag in price increases and create a further gap as shown in the “Mobility” bar below. In the more consumer-facing coatings, it is easier to raise prices more quickly and Axalta and others have managed to keep pace with costs. We see the pricing versus costs issue as a much greater headwind for the specialty chemical companies than for the commodity companies and the industrial gas companies – the commodity chemical companies can raise prices more quickly and most industrial gas pricing is on a cost pass-through basis.

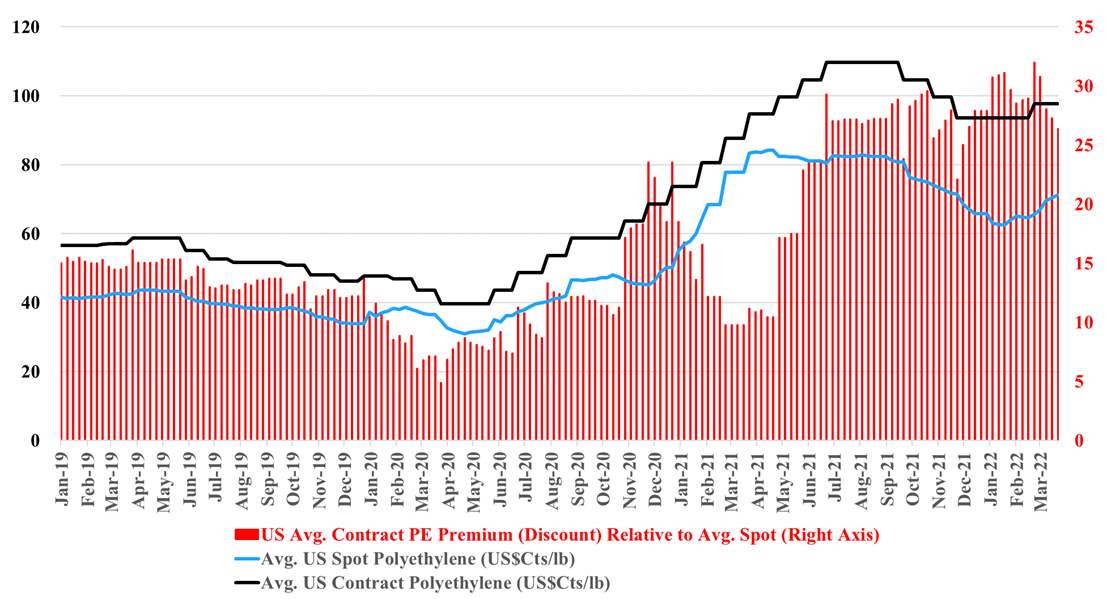

It's back to 2012/2013 for polyethylene, but with a potential twist. As we noted in today's daily report, international prices for polyethylene are being pushed up by oil prices, and even with higher prices in Asia, margins are still negative locally, which suggests that they will go higher. This margin umbrella is what generated windfall profits for US and Middle East producers in 2012, 2013, and half of 2014. The upward pressure remains high for international polyethylene prices because producers are not covering costs locally and in theory, the US should continue to benefit and we see domestic polyethylene prices rising again, both contract and spot. The risk for the US is local overcapacity of polyethylene and potential export challenges. The pricing arbitrage to export US polyethylene is huge and rising, but we are in a constrained trade world and we understand that export terminals are at capacity and warehouses are full. It is possible that the sharply lower US ethylene price is not just a function of new ethylene capacity, but also a function of integrated polyethylene producers choosing to limit production and looking for homes for the extra ethylene. If the polyethylene producers in the US try to push more volume domestically we could see local prices fall well below their export alternative – this is possible, but unlikely, in our view. Polypropylene does not have the same significant net export and the two plant closure in the US are likely enough to drive the price support that we are seeing this week.

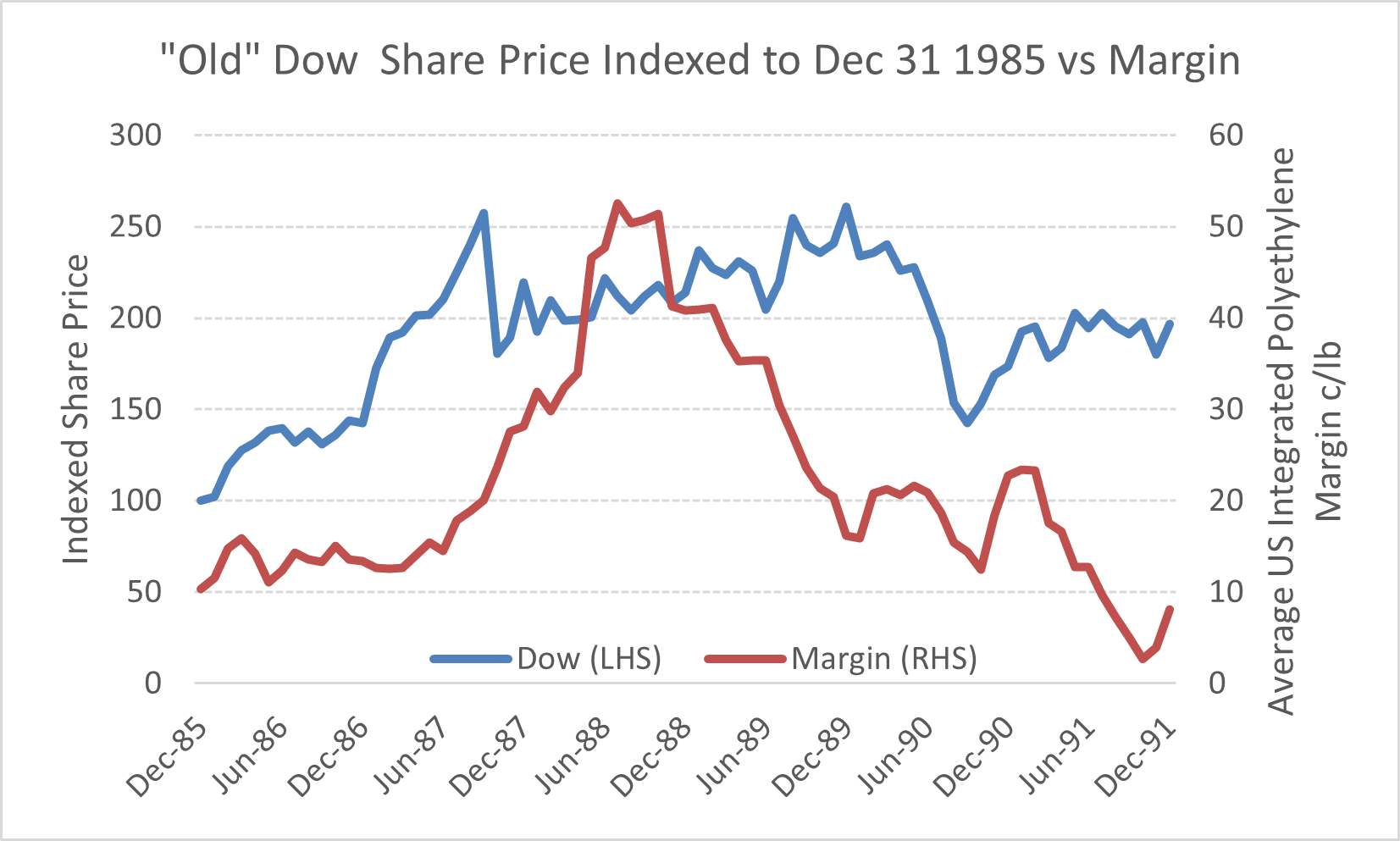

In yesterday's Sunday thematic and weekly recap report titled "Waiting For The Big One – Is A Chemical Mega-Cycle Ahead?", we referenced the global shortage of basic chemicals and polymers in the late 80's. We think this could repeat because of limited capital spending to grow basic chemical capacity due to cost and long-term demand uncertainties and this could cause a mid-decade global profit mega-cycle. Emission abatement initiatives and concerns with feedstock prices/availability will work against the justification of capacity expansions in every global region. Demand growth mitigation from plastic bans, renewables, and increased like-for-like recycling is unlikely to impact materially pre-2026/27.