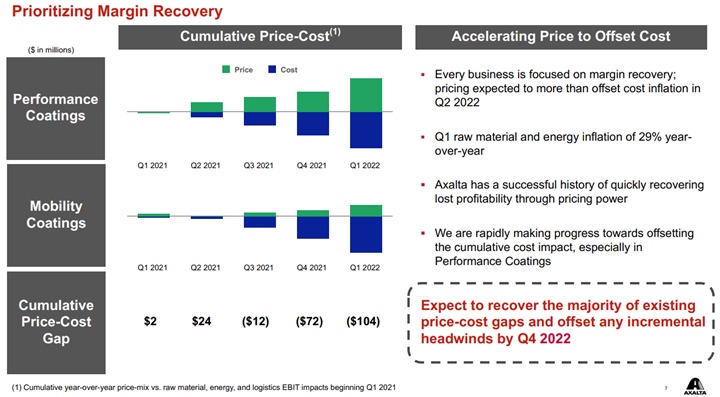

Axalta shows a helpful picture below of how pricing and costs are moving. All coatings producers are seeing the same cost inflation, some of it energy/hydrocarbon input related and some of it supply chain-related – either for inputs such as pigments or higher costs of getting products to markets. How pricing looks relative to costs is very customer dependent, as shown in the chart below. Auto OEM customers have long lead times on price adjustments and this is why Axalta is signaling the end of the year before prices will be aligned with costs. This of course assumes that costs do not rise again in 2H 2022 as they will also drive a lag in price increases and create a further gap as shown in the “Mobility” bar below. In the more consumer-facing coatings, it is easier to raise prices more quickly and Axalta and others have managed to keep pace with costs. We see the pricing versus costs issue as a much greater headwind for the specialty chemical companies than for the commodity companies and the industrial gas companies – the commodity chemical companies can raise prices more quickly and most industrial gas pricing is on a cost pass-through basis.

With the rapid jump in international natural gas and oil prices, we would see very concerted efforts to raise basic chemicals and polymer prices in Europe and Asia and will have a positive knock-on effect for the US. In our weekly catalyst report on Monday, we showed that ethylene producers outside the US were all losing money, especially in Europe and Asia. Some European demand will already be lower, because of curtailed product exports to Russia and Ukraine, but producers will want to cover costs at a very minimum and consequently, will be trying to match price increases with cost increases and if possible do a bit better than that. All of this will create a greater margin umbrella for the US, and US exporters selling directly into international markets will see export margins step up and may see incremental opportunities to export more, assuming that the freight rates are not too onerous for incremental containers.

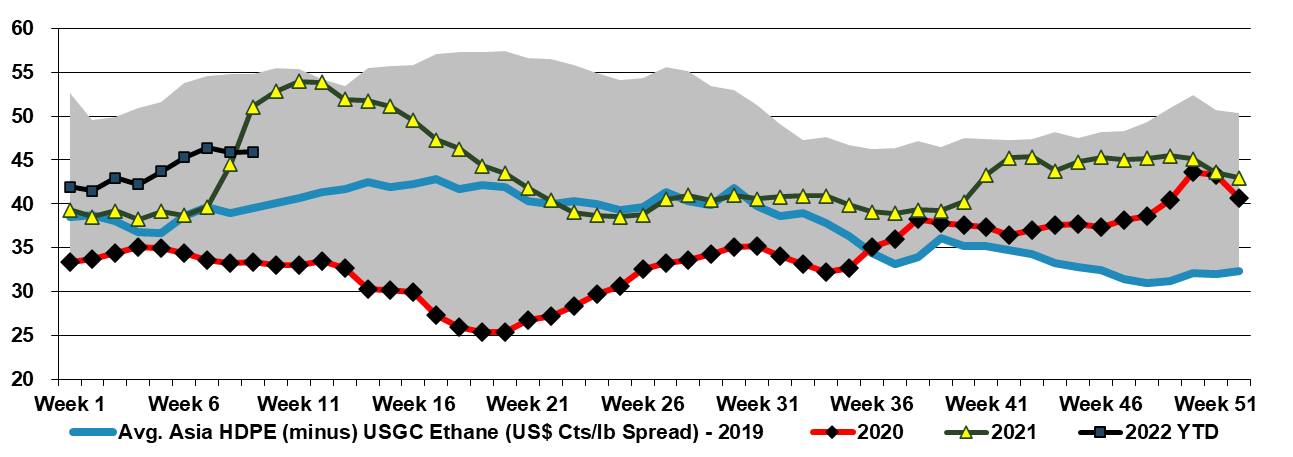

Pessimism in the Asia ethylene market is a bad sign for ethylene vs. other US monomers. Those in the US with ethylene surpluses may need to fight a bit harder to find homes for the excess product in the US. We have not focused on the cost curve for a while as markets have been tight and global costs have not been an influence in the market for some time. The US has plenty of dry powder, in that export prices can fall significantly before they approach ethane-based costs, and can fall below production costs outside the US – especially in Asia – and still generate a margin for the US sellers. But that would mean more downside for US spot pricing and it may be enough to create some surpluses and some downward pressure on US derivative pricing. The caveat, of course, is that we had the same setup last year, albeit with less new capacity in Asia, and the summer hurricane season quickly wiped away any US surplus. A better understanding of the current cost curve and relative regional pricing can be found in our Weekly from Monday.