It is likely a difficult day for the European chemical industry as all of the fuel prices that they depend on are rising quickly, which will force many difficult decisions over the coming days. There are a couple of factors to consider – what happens to costs and margins if energy prices remain inflated, and what happens if energy availability becomes an issue and plant closures are necessary. In a world that is already reeling from inflationary pressure that we have not seen in four decades, there is at least an acceptance that prices can move higher, but the energy-dependent European industrial and materials companies will need to move prices quickly and meaningfully to absorb their higher costs. If natural gas supplies from Russia are halted, Europe is likely going to need to allocate supplies, as there is no easy fix given an LNG system that is already at capacity. Industry will likely take the hit to ensure power for heating and cooling. This will drive product shortages in Europe, especially for chemicals, which will likely make it easier to get the pricing necessary to cover costs.

Part of our confidence/concern that prices can continue to rise in the chemical space in general stems from what seems to be very strong demand – again confirmed in earnings reports overnight, as well as in the rail data from today's daily report, as well as inventory data that suggest we are below recent ratios to shipment trends. The inventory piece is the great unknown here because the supply chain shocks of the last 20 months will have reset expectations around “safe” levels of inventory and it is hard to judge whether the new “comfort” normal will be back to the trend in the chart or 50% higher! If the new comfort level is materially higher than in the past, demand growth will remain strong and price momentum could continue through 2022. Our expectations for a mega-cycle in basic chemicals and polymers – targeting late 2023 and 2024 could be dragged forward because of higher apparent demand the time to buy the equities could be now, on that basis.

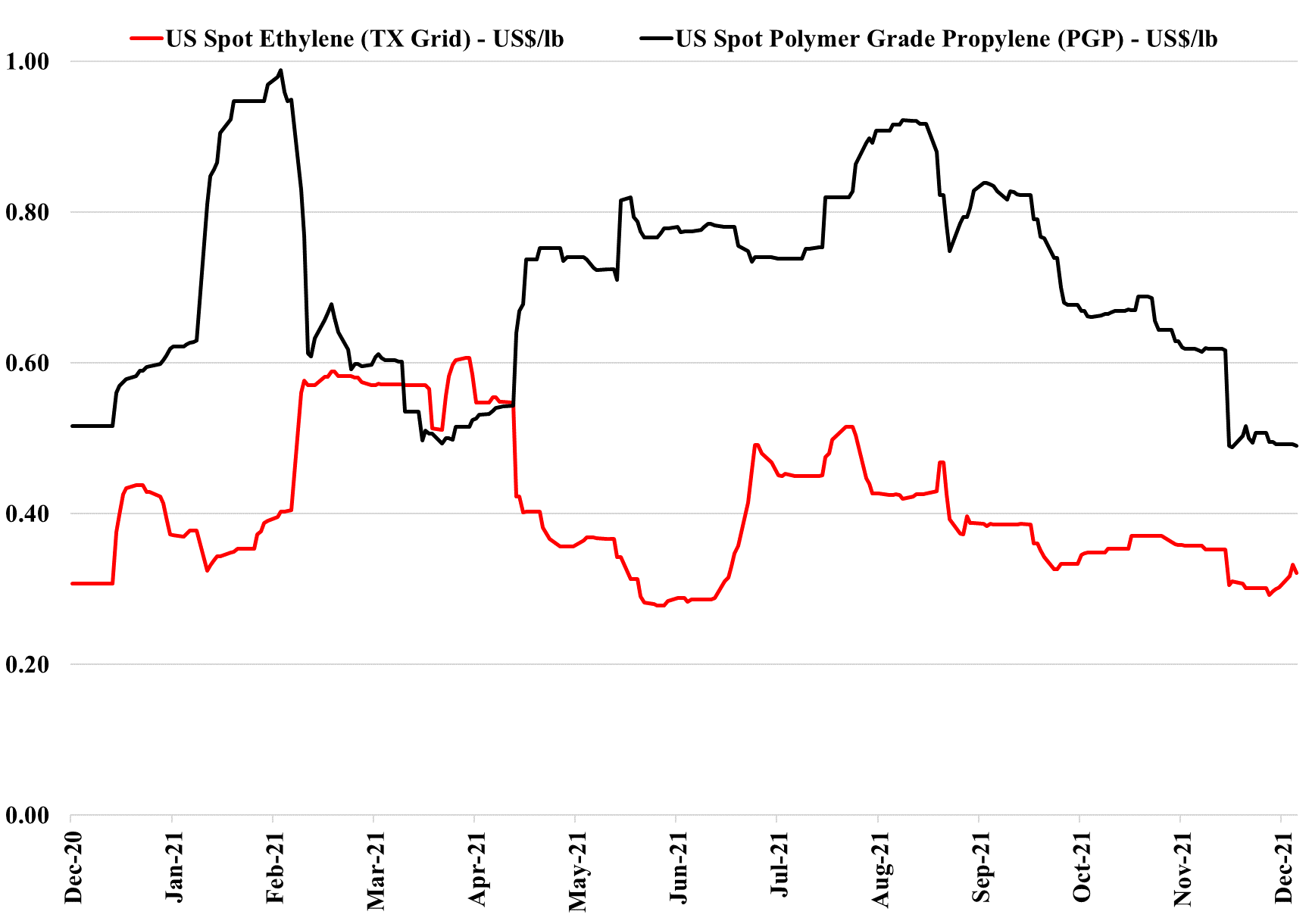

We have seen relative stability in US spot ethylene and propylene prices for several weeks now, despite some volatility in feedstock markets. Ethylene likely has significant export support in that there are complexes in Asia that are net short of ethylene and where derivative production can be increased if ethylene is available at the right price. There are also displacement opportunities if US ethylene can be delivered to importers in Asia at lower prices than local production costs. This is broadly the case today and there may even be select opportunities in Europe. In Asia it is likely easier, as the buyer would be replacing an alternate supplier. In Europe, most potential buyers would be looking at cutting back their own local production and that is a more marginal decision given the impact on unit economics of lower operating rates. US propylene demand remains high, but prices are now settling closer to PDH costs, although not close enough to encourage anyone to slow production. See more in today's daily report!

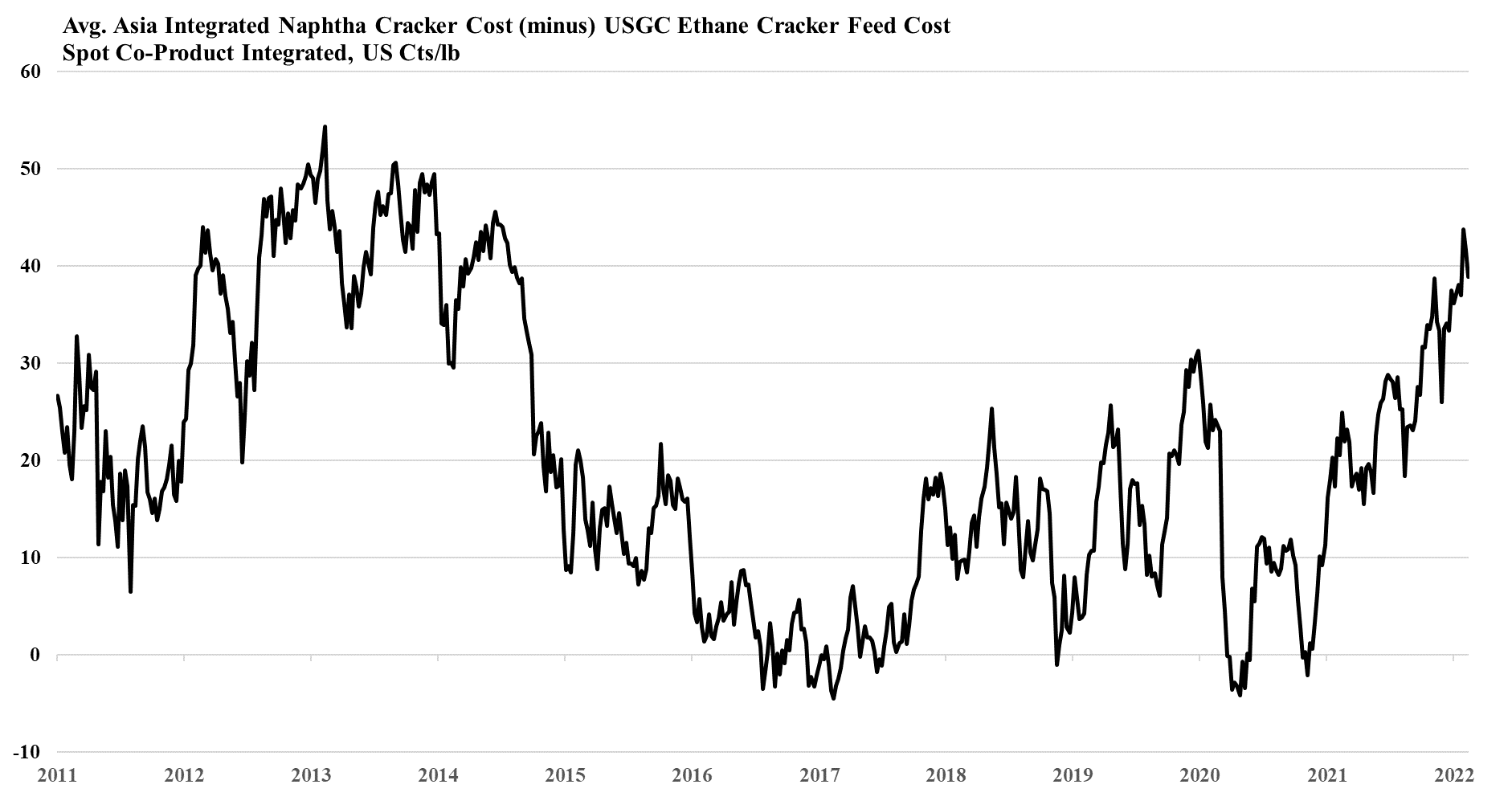

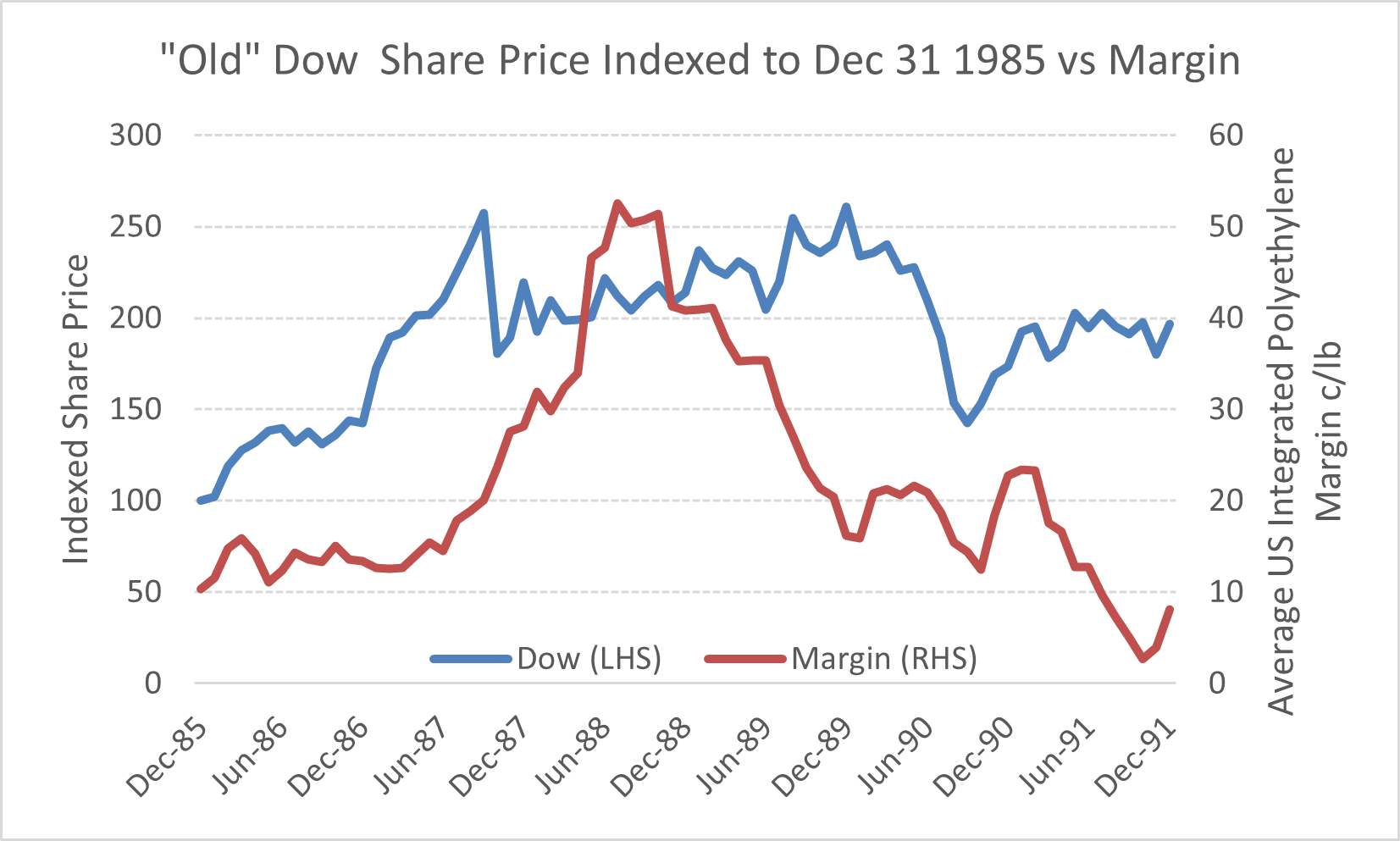

In yesterday's Sunday thematic and weekly recap report titled "Waiting For The Big One – Is A Chemical Mega-Cycle Ahead?", we referenced the global shortage of basic chemicals and polymers in the late 80's. We think this could repeat because of limited capital spending to grow basic chemical capacity due to cost and long-term demand uncertainties and this could cause a mid-decade global profit mega-cycle. Emission abatement initiatives and concerns with feedstock prices/availability will work against the justification of capacity expansions in every global region. Demand growth mitigation from plastic bans, renewables, and increased like-for-like recycling is unlikely to impact materially pre-2026/27.

Our latest Sunday Thematic report, "Damned if you Dow and Damned if you Down’t. Hard to win", centers around Dow's announced development of a new net-zero carbon emissions site in Alberta, Canada. It discusses company-specific and sector ramifications for Dow's strategic move to produce low-cost low carbon polyethylene in Canada while also expanding capacity.